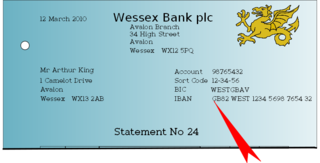

The International Bank Account Number (IBAN) is an internationally agreed upon system of identifying bank accounts across national borders to facilitate the communication and processing of cross border transactions with a reduced risk of transcription errors. An IBAN uniquely identifies the account of a customer at a financial institution. It was originally adopted by the European Committee for Banking Standards (ECBS) and since 1997 as the international standard ISO 13616 under the International Organization for Standardization (ISO). The current version is ISO 13616:2020, which indicates the Society for Worldwide Interbank Financial Telecommunication (SWIFT) as the formal registrar. Initially developed to facilitate payments within the European Union, it has been implemented by most European countries and numerous countries in other parts of the world, mainly in the Middle East and the Caribbean. By July 2024, 88 countries were using the IBAN numbering system.

Friendly fraud, also known as chargeback fraud occurs when a consumer makes an online shopping purchase with their own credit card, and then requests a chargeback from the issuing bank after receiving the purchased goods or services. Once approved, the chargeback cancels the financial transaction, and the consumer receives a refund of the money they spent. Dependent on the payment method used, the merchant can be accountable when a chargeback occurs.

A payment service provider (PSP) is a third-party company that allows businesses to accept electronic payments, such as credit card and debit card payments. PSPs act as intermediaries between those who make payments, i.e. consumers, and those who accept them, i.e. retailers.

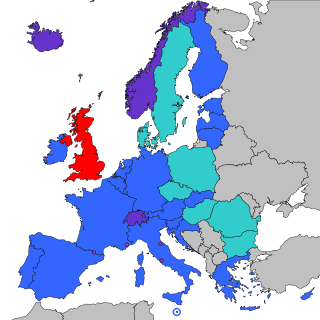

The Single Euro Payments Area (SEPA) is a payment integration initiative of the European Union for simplification of bank transfers denominated in euros. As of 2020, there were 36 members in SEPA, consisting of the 27 member states of the European Union, the four member states of the European Free Trade Association, and the United Kingdom. Some microstates participate in the technical schemes: Andorra, Monaco, San Marino, and Vatican City.

UN/CEFACT TBG5 is the entity responsible for financial services under the United Nations Centre for Trade facilitation and Electronic Business, (UN/CEFACT) under the United Nations Economic Commission for Europe (UNECE).

The Revised Payment Services Directive (PSD2, Directive (EU) 2015/2366, which replaced the Payment Services Directive (PSD), Directive 2007/64/EC) is an EU Directive, administered by the European Commission (Directorate General Internal Market) to regulate payment services and payment service providers throughout the European Union (EU) and European Economic Area (EEA). The PSD's purpose was to increase pan-European competition and participation in the payments industry also from non-banks, and to provide for a level playing field by harmonizing consumer protection and the rights and obligations of payment providers and users. The key objectives of the PSD2 directive are creating a more integrated European payments market, making payments more secure and protecting consumers.

Design for All in the context of information and communications technology (ICT) is the conscious and systematic effort to proactively apply principles, methods and tools to promote universal design in computer-related technologies, including Internet-based technologies, thus avoiding the need for a posteriori adaptations, or specialised design.

Natech is a global technology company specializing in software and services for the financial sector.

The International Association of Deposit Insurers (IADI) was formed on 6 May 2002 with the purpose of sharing deposit insurance expertise with the world and contributing to the stability of financial systems as the standard setter for deposit insurance with a global and expanding membership.

Money Dashboard is a free online personal financial management service in the United Kingdom. It provides users with the ability to view all of their online financial accounts in one place and categorises and analyses all of their transactions so they can understand how they use money. The app aims to help consumers make better financial decisions and budget for the future.

Strong customer authentication (SCA) is a requirement of the EU Revised Directive on Payment Services (PSD2) on payment service providers within the European Economic Area. The requirement ensures that electronic payments are performed with multi-factor authentication, to increase the security of electronic payments. Physical card transactions already commonly have what could be termed strong customer authentication in the EU, but this has not generally been true for Internet transactions across the EU prior to the implementation of the requirement, and many contactless card payments do not use a second authentication factor.

In financial services, open banking allows for financial data to be shared between banks and third-party service providers through the use of application programming interfaces (APIs). Traditionally, banks have kept customer financial data within their own closed systems. Open banking allows customers to share their financial information securely and electronically with other banks or other authorized financial organizations such as payment providers, lenders and insurance companies.

EBA Clearing is a provider of pan-European payment infrastructure wholly owned by shareholders that consist of major European banks.

Banking as a service (BaaS) is the provision of banking products to non-bank third parties through APIs.

Settle Group is a Norwegian, VC-backed financial technology company. Its PSD2 compliant technology platform enables banks to issue white label mobile payments products to their private and merchant customers.

Yakiv Vasyliovych Smolii is a Ukrainian economist and banker and former chairman of the National Bank of Ukraine. He was acting governor of the National Bank from 11 May 2017 until the Ukrainian parliament elected him governor on 15 March 2018. Smolii was dismissed by the parliament on 3 July 2020 after he had tendered his resignation, he claimed he had done this as a result of long-standing political pressure.

The development of neobanks in Europe is a trend in the European financial landscape beginning in the 2010s. Neobanks are a type of digital-only bank that offer financial services primarily through mobile and web applications, with little or no reliance on physical branches. The trend was driven by advancements in technology, changing consumer preferences, and supportive regulatory frameworks. Neobanks provide a range of services, including personal accounts, loans, and payment services, with a focus on user-friendly interfaces, low fees, and innovative features. In 2022, the European neobank market has generated over 570B transactions.

The Central Electronic System of Payments (CESOP) regime is an automatic exchange of information regime being introduced in the European Union from 1 January 2024. The rules were introduced by Council Directive 2020/284, amending the EU's Value-added tax Directive.

Open finance is a concept and practice within the financial services industry that involves the secure sharing of financial data with third-party service providers through Application Programming Interfaces (APIs). Building upon the principles of open banking, which focuses primarily on banking data, open finance aims to give consumers and businesses greater control over their financial data, enabling them to access a wider range of financial products and services. This includes sharing data beyond traditional banking, encompassing areas like investments, pensions, mortgages, and insurance.

The STET-CORE system is a French interbank automated clearing house that has been designated as a Systemically Important Payment System at the European level. STET, the name of the operating company, refers to Systèmes Technologiques d'Echange et de Traitement, and CORE, the name of the infrastructure itself, refers to COmpensation REtail.