Related Research Articles

The United States of America has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2020, taxes collected by federal, state, and local governments amounted to 25.5% of GDP, below the OECD average of 33.5% of GDP. The United States had the seventh-lowest tax revenue-to-GDP ratio among OECD countries in 2020, with a higher ratio than Mexico, Colombia, Chile, Ireland, Costa Rica, and Turkey.

A trust is a legal relationship in which the holder of a right gives it to another person or entity who must keep and use it solely for another's benefit. In the Anglo-American common law, the party who entrusts the right is known as the "settlor", the party to whom the right is entrusted is known as the "trustee", the party for whose benefit the property is entrusted is known as the "beneficiary", and the entrusted property itself is known as the "corpus" or "trust property". A testamentary trust is created by a will and arises after the death of the settlor. An inter vivos trust is created during the settlor's lifetime by a trust instrument. A trust may be revocable or irrevocable; an irrevocable trust can be "broken" (revoked) only by a judicial proceeding.

The Sixteenth Amendment to the United States Constitution allows Congress to levy an income tax without apportioning it among the states on the basis of population. It was passed by Congress in 1909 in response to the 1895 Supreme Court case of Pollock v. Farmers' Loan & Trust Co. The Sixteenth Amendment was ratified by the requisite number of states on February 3, 1913, and effectively overruled the Supreme Court's ruling in Pollock.

A charitable trust is an irrevocable trust established for charitable purposes and, in some jurisdictions, a more specific term than "charitable organization". A charitable trust enjoys a varying degree of tax benefits in most countries. It also generates good will. Some important terminology in charitable trusts is the term "corpus", which refers to the assets with which the trust is funded, and the term "donor", which is the person donating assets to a charity.

In the law of the United States, an insular area is a U.S.-associated jurisdiction that is not part of the 50 states or the District of Columbia. This includes fourteen U.S. territories administered under U.S. sovereignty, as well as three sovereign states each with a Compact of Free Association with the United States. The term also may be used to refer to the previous status of the Philippine Islands and the Trust Territory of the Pacific Islands when it existed.

Excise tax in the United States is an indirect tax on listed items. Excise taxes can be and are made by federal, state and local governments and are not uniform throughout the United States. Certain goods, such as gasoline, diesel fuel, alcohol, and tobacco products, are taxed by multiple governments simultaneously. Some excise taxes are collected from the producer or retailer and not paid directly by the consumer, and as such often remain "hidden" in the price of a product or service, rather than being listed separately.

A 529 plan, also called a Qualified Tuition Program, is a tax-advantaged investment vehicle in the United States designed to encourage saving for the future higher education expenses of a designated beneficiary. In 2017, K–12 public, private, and religious school tuition were included as qualified expenses for 529 plans along with post-secondary education costs after passage of the Tax Cuts and Jobs Act.

The Uniform Law Commission (ULC), also called the National Conference of Commissioners on Uniform State Laws, is a non-profit, American unincorporated association. Established in 1892, the ULC aims to provide U.S. states with well-researched and drafted model acts to bring clarity and stability to critical areas of statutory law across jurisdictions. The ULC promotes enactment of uniform acts in areas of state law where uniformity is desirable and practical. The ULC headquarters are in Chicago, Illinois.

In addition to federal income tax collected by the United States, most individual U.S. states collect a state income tax. Some local governments also impose an income tax, often based on state income tax calculations. Forty-two states and many localities in the United States impose an income tax on individuals. Eight states impose no state income tax, and a ninth, New Hampshire, imposes an individual income tax on dividends and interest income but not other forms of income. Forty-seven states and many localities impose a tax on the income of corporations.

The Uniform Prudent Investor Act(UPIA), which was adopted in 1992 by the American Law Institute's Third Restatement of the Law of Trusts ("Restatement of Trust 3d"), reflects a "modern portfolio theory" and "total return" approach to the exercise of fiduciary investment discretion.

Supplemental needs trust is a US-specific term for a type of special needs trust. Supplemental needs trusts are compliant with provisions of US state and federal law and are designed to provide benefits to, and protect the assets of, individuals with physical, psychiatric, or intellectual disabilities, and still allow such persons to be qualified for and receive governmental health care benefits, especially long-term nursing care benefits, under the Medicaid welfare program.

The U.S. generation-skipping transfer tax imposes a tax on both outright gifts and transfers in trust to or for the benefit of unrelated persons who are more than 37.5 years younger than the donor or to related persons more than one generation younger than the donor, such as grandchildren. These people are known as "skip persons." In most cases where a trust is involved, the GST tax will be imposed only if the transfer avoids incurring a gift or estate tax at each generation level.

United States trust law is the body of law regulating the legal instrument for holding wealth known as a trust.

The Uniform Probate Code is a uniform act drafted by National Conference of Commissioners on Uniform State Laws (NCCUSL) governing inheritance and the decedents' estates in the United States. The primary purposes of the act were to streamline the probate process and to standardize and modernize the various state laws governing wills, trusts, and intestacy.

A model act, also called a model law or a piece of model legislation, is a suggested example for a law, drafted centrally to be disseminated and suggested for enactment in multiple independent legislatures. The motivation classically has been the hope of fostering more legal uniformity among jurisdictions, and better practice in legislative wording, than would otherwise occur; another motivation sometimes has been lobbying disguised under such ideals. Model laws can be intended to be enacted verbatim, to be enacted after minor modification, or to serve more as general guides for the legislatures.

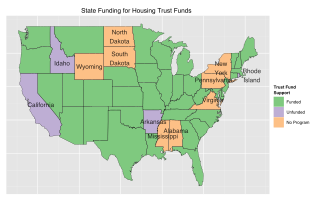

Housing trust funds are established sources of funding for affordable housing construction and other related purposes created by governments in the United States (U.S.). Housing Trust Funds (HTF) began as a way of funding affordable housing in the late 1970s. Since then, elected government officials from all levels of government in the U.S. have established housing trust funds to support the construction, acquisition, and preservation of affordable housing and related services to meet the housing needs of low-income households. Ideally, HTFs are funded through dedicated revenues like real estate transfer taxes or document recording fees to ensure a steady stream of funding rather than being dependent on regular budget processes. As of 2016, 400 state, local and county trust funds existed across the U.S.

The Nonadmitted and Reinsurance Reform Act of 2010 is a United States law regulating the sale of insurance in states where the insurer is usually not authorized to sell insurance. It prevents states other than the home state of a U.S. insurance company from imposing regulations or taxes on the sale of nonadmitted insurance.

The Uniform Power of Attorney Act (2006) (UPOAA) was a law proposed by the National Conference of Commissioners on Uniform State Laws (ULC) to create a uniform framework for power of attorney provisions throughout the United States.

The Uniform Fiduciary Income and Principal Act (UFIPA) is one of the uniform acts that have been proposed in an attempt to harmonize the law in all fifty U.S. states. UFIPA was finalized and adopted by the Uniform Law Commission (ULC) in 2018.

In the United States, those seeking to become lawyers must normally pass a bar examination before they can be admitted to the bar and become licensed to practice law. Bar exams are administered by states or territories, generally by agencies under the authority of state supreme courts. Almost all states use some examination components created by the National Conference of Bar Examiners (NCBE). Forty-one jurisdictions have adopted the Uniform Bar Examination (UBE), which is composed entirely of NCBE-created components.

References

- 1 2 Christopher Cline, Speed Walking Through the Uniform Principal and Income Act (2019), retrieved at https://s3-us-west-2.amazonaws.com/oregonstatebar/Seminars/2019/AEP19-2.pdf

- ↑ "UNIFORM PRINCIPAL AND INCOME ACT" (PDF). Michigan Compiled Laws. 1 (4): 4.

| | This economics-related article is a stub. You can help Wikipedia by expanding it. |