Passive management is an investing strategy that tracks a market-weighted index or portfolio. Passive management is most common on the equity market, where index funds track a stock market index, but it is becoming more common in other investment types, including bonds, commodities and hedge funds.

An index fund is a mutual fund or exchange-traded fund (ETF) designed to follow certain preset rules so that the fund can track a specified basket of underlying investments. While index providers often emphasize that they are for-profit organizations, index providers have the ability to act as "reluctant regulators" when determining which companies are suitable for an index. Those rules may include tracking prominent indexes like the S&P 500 or the Dow Jones Industrial Average or implementation rules, such as tax-management, tracking error minimization, large block trading or patient/flexible trading strategies that allow for greater tracking error but lower market impact costs. Index funds may also have rules that screen for social and sustainable criteria.

In finance, the capital asset pricing model (CAPM) is a model used to determine a theoretically appropriate required rate of return of an asset, to make decisions about adding assets to a well-diversified portfolio.

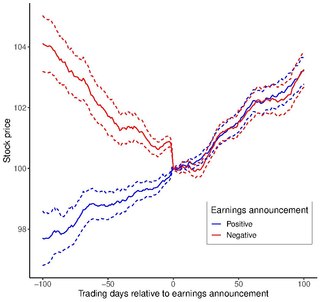

The efficient-market hypothesis (EMH) is a hypothesis in financial economics that states that asset prices reflect all available information. A direct implication is that it is impossible to "beat the market" consistently on a risk-adjusted basis since market prices should only react to new information.

For an individual, a risk premium is the minimum amount of money by which the expected return on a risky asset must exceed the known return on a risk-free asset in order to induce an individual to hold the risky asset rather than the risk-free asset. It is positive if the person is risk averse. Thus it is the minimum willingness to accept compensation for the risk.

In financial markets, stock valuation is the method of calculating theoretical values of companies and their stocks. The main use of these methods is to predict future market prices, or more generally, potential market prices, and thus to profit from price movement – stocks that are judged undervalued are bought, while stocks that are judged overvalued are sold, in the expectation that undervalued stocks will overall rise in value, while overvalued stocks will generally decrease in value.

Value investing is an investment paradigm that involves buying securities that appear underpriced by some form of fundamental analysis. The various forms of value investing derive from the investment philosophy first taught by Benjamin Graham and David Dodd at Columbia Business School in 1928, and subsequently developed in their 1934 text Security Analysis.

In finance, Jensen's alpha is used to determine the abnormal return of a security or portfolio of securities over the theoretical expected return. It is a version of the standard alpha based on a theoretical performance instead of a market index.

Contrarian Investing is an investment strategy that is characterized by purchasing and selling in contrast to the prevailing sentiment of the time.

Active management refers to a portfolio management strategy where the manager makes specific investments with the goal of outperforming an investment benchmark index or target return. In passive management, investors expect a return that closely replicates the investment weighting and returns of a benchmark index and will often invest in an index fund.

A market anomaly in a financial market is predictability that seems to be inconsistent with theories of asset prices. Standard theories include the capital asset pricing model and the Fama-French Three Factor Model, but a lack of agreement among academics about the proper theory leads many to refer to anomalies without a reference to a benchmark theory. Indeed, many academics simply refer to anomalies as "return predictors", avoiding the problem of defining a benchmark theory.

Business valuation is a process and a set of procedures used to estimate the economic value of an owner's interest in a business. Valuation is used by financial market participants to determine the price they are willing to pay or receive to effect a sale of a business. In addition to estimating the selling price of a business, the same valuation tools are often used by business appraisers to resolve disputes related to estate and gift taxation, divorce litigation, allocate business purchase price among business assets, establish a formula for estimating the value of partners' ownership interest for buy-sell agreements, and many other business and legal purposes such as in shareholders deadlock, divorce litigation and estate contest. In some cases, the court would appoint a forensic accountant as the joint expert doing the business valuation. In these cases, attorneys should always be prepared to have their expert’s report withstand the scrutiny of cross-examination and criticism.

Fundamentally based indexes are indices in which stocks are weighted by one of many economic fundamental factors, especially accounting figures which are commonly used when performing corporate valuation, or by a composite of several fundamental factors. A potential benefit with composite fundamental indices is that they might average out specific sector biases which may be the case when only using one fundamental factor. A key belief behind the fundamental index methodology is that underlying corporate accounting/valuation figures are more accurate estimators of a company's intrinsic value, rather than the listed market value of the company, i.e. that one should buy and sell companies in line with their accounting figures rather than according to their current market prices. In this sense fundamental indexing is linked to so-called fundamental analysis.

In asset pricing and portfolio management the Fama–French three-factor model is a model designed by Eugene Fama and Kenneth French to describe stock returns. Fama and French were professors at the University of Chicago Booth School of Business, where Fama still resides. In 2013, Fama shared the Nobel Memorial Prize in Economic Sciences. The three factors are (1) market risk, (2) the outperformance of small versus big companies, and (3) the outperformance of high book/market versus small book/market companies. However, the size and book/market ratio themselves are not in the model. For this reason, there is academic debate about the meaning of the last two factors.

Clifford Scott Asness is an American billionaire hedge fund manager and the co-founder of AQR Capital Management.

The price-to-book ratio, or P/B ratio, is a financial ratio used to compare a company's current market value to its book value. The calculation can be performed in two ways, but the result should be the same. In the first way, the company's market capitalization can be divided by the company's total book value from its balance sheet. The second way, using per-share values, is to divide the company's current share price by the book value per share. It is also known as the market-to-book ratio and the price-to-equity ratio, and its inverse is called the book-to-market ratio.

The low-volatility anomaly is the observation that low-volatility stocks have higher returns than high-volatility stocks in most markets studied. This is an example of a stock market anomaly since it contradicts the central prediction of many financial theories that taking higher risk must be compensated with higher returns.

In portfolio management, the Carhart four-factor model is an extra factor addition in the Fama–French three-factor model, including a momentum factor for asset pricing of stocks, proposed by Mark Carhart. It is also known in the industry as the Monthly Momentum Factor(MOM). Momentum is the speed or velocity of price changes in a stock, security, or tradable instrument.

Factor investing is an investment approach that involves targeting quantifiable firm characteristics or “factors” that can explain differences in stock returns. Over the last fifty years, academic research has identified hundreds of factors that impact stock returns. Security characteristics that may be included in a factor-based approach includes size, value, momentum, asset growth, profitability, leverage, term and carry.

Low-volatility investing is an investment style that buys stocks or securities with low volatility and avoids those with high volatility. This investment style exploits the low-volatility anomaly. According to financial theory risk and return should be positively related, however in practice this is not true. Low-volatility investors aim to achieve market-like returns, but with lower risk. This investment style is also referred to as minimum volatility, minimum variance, managed volatility, smart beta, defensive and conservative investing.