In budgeting, and management accounting in general, a variance is the difference between a budgeted, planned, or standard cost and the actual amount incurred/sold. Variances can be computed for both costs and revenues.

The concept of variance is intrinsically connected with planned and actual results and effects of the difference between those two on the performance of the entity or company.

Types of variances

Variances can be divided according to their effect or nature of the underlying amounts.

When effect of variance is concerned, there are two types of variances:

When actual results are better than expected results given variance is described as favorable variance. In common use favorable variance is denoted by the letter F - usually in parentheses (F).

When actual results are worse than expected results given variance is described as adverse variance, or unfavourable variance. In common use adverse variance is denoted by the letter U or the letter A - usually in parentheses (A).

The second typology (according to the nature of the underlying amount) is determined by the needs of users of the variance information and may include e.g.:

Variance analysis, in budgeting or management accounting in general, is a tool of budgetary control and performance evaluation, assessing any variances between the budgeted, planned, or standard amount, and the actual amount realized. Variance analysis can be carried out for both costs and revenues.

Variance analysis is usually associated with explaining the difference (or variance) between actual costs and the standard costs allowed for the good output. For example, the difference in materials costs can be divided into a materials price variance and a materials usage variance. The difference between the actual direct labor costs and the standard direct labor costs can be divided into a rate variance and an efficiency variance. The difference in manufacturing overhead can be divided into spending, efficiency, and volume variances. Mix and yield variances can also be calculated.

Variance analysis helps management to understand the present costs and then to control future costs. Variance calculation should always be calculated by taking the planned or budgeted amount and subtracting the actual/forecasted value. Thus a positive number is favorable and a negative number is unfavorable.

Earned Value Management (EVM), earned value project management, or earned value performance management (EVPM) is a project management technique for measuring project performance and progress in an objective manner.

Cost accounting is defined by the Institute of Management Accountants as "a systematic set of procedures for recording and reporting measurements of the cost of manufacturing goods and performing services in the aggregate and in detail. It includes methods for recognizing, classifying, allocating, aggregating and reporting such costs and comparing them with standard costs". Often considered a subset of managerial accounting, its end goal is to advise the management on how to optimize business practices and processes based on cost efficiency and capability. Cost accounting provides the detailed cost information that management needs to control current operations and plan for the future.

In management accounting or managerial accounting, managers use accounting information in decision-making and to assist in the management and performance of their control functions.

Environmental full-cost accounting (EFCA) is a method of cost accounting that traces direct costs and allocates indirect costs by collecting and presenting information about the possible environmental, social and economical costs and benefits or advantages – in short, about the "triple bottom line" – for each proposed alternative. It is also known as true-cost accounting (TCA), but, as definitions for "true" and "full" are inherently subjective, experts consider both terms problematic.

Market risk is the risk of losses in positions arising from movements in market variables like prices and volatility. There is no unique classification as each classification may refer to different aspects of market risk. Nevertheless, the most commonly used types of market risk are:

A performance indicator or key performance indicator (KPI) is a type of performance measurement. KPIs evaluate the success of an organization or of a particular activity in which it engages. KPIs provide a focus for strategic and operational improvement, create an analytical basis for decision making and help focus attention on what matters most.

In variance analysis (accounting) direct material total variance is the difference between the actual cost of actual number of units produced and its budgeted cost in terms of material. Direct material total variance can be divided into two components:

Direct labour cost variance is the difference between the standard cost for actual production and the actual cost in production.

Energy monitoring and targeting (M&T) is an energy efficiency technique based on the standard management axiom stating that “you cannot manage what you cannot measure”. M&T techniques provide energy managers with feedback on operating practices, results of energy management projects, and guidance on the level of energy use that is expected in a certain period. Importantly, they also give early warning of unexpected excess consumption caused by equipment malfunctions, operator error, unwanted user behaviours, lack of effective maintenance and the like.

Financial Management for IT Services is a Service Strategy element of the ITIL best practice framework. The aim of this ITIL process area is to give accurate and cost effective stewardship of IT assets and resources used in providing IT Services. It is used to plan, control and recover costs expended in providing the IT Services negotiated and agreed to in a service-level agreement (SLA).

A cost estimate is the approximation of the cost of a program, project, or operation. The cost estimate is the product of the cost estimating process. The cost estimate has a single total value and may have identifiable component values.

Project workforce management is the practice of combining the coordination of all logistic elements of a project through a single software application. This includes planning and tracking of schedules and mileposts, cost and revenue, resource allocation, as well as overall management of these project elements. Efficiency is improved by eliminating manual processes, like spreadsheet tracking to monitor project progress. It also allows for at-a-glance status updates and ideally integrates with existing legacy applications in order to unify ongoing projects, enterprise resource planning (ERP) and broader organizational goals. There are a lot of logistic elements in a project. Different team members are responsible for managing each element and often, the organisation may have a mechanism to manage some logistic areas as well.

In business, overhead or overhead expense refers to an ongoing expense of operating a business. Overheads are the expenditure which cannot be conveniently traced to or identified with any particular revenue unit, unlike operating expenses such as raw material and labor. Therefore, overheads cannot be immediately associated with the products or services being offered, thus do not directly generate profits. However, overheads are still vital to business operations as they provide critical support for the business to carry out profit making activities. For example, overhead costs such as the rent for a factory allows workers to manufacture products which can then be sold for a profit. Such expenses are incurred for output generally and not for particular work order; e.g., wages paid to watch and ward staff, heating and lighting expenses of factory, etc. Overheads are also a very important cost element along with direct materials and direct labor.

Control is a function of management that helps to check errors and take corrective actions. This is done to minimize deviation from standards and ensure that the stated goals of the organization are achieved in a desired manner.

Job costing is accounting which tracks the costs and revenues by "job" and enables standardized reporting of profitability by job. For an accounting system to support job costing, it must allow job numbers to be assigned to individual items of expenses and revenues. A job can be defined to be a specific project done for one customer, or a single unit of product manufactured, or a batch of units of the same type that are produced together.

Price variance (Vmp) is a term used in cost accounting which denotes the difference between the expected cost of an item and the actual cost at the time of purchase. The price of an item is often affected by the quantity of items ordered, and this is taken into consideration. A price variance means that actual costs may exceed the budgeted cost, which is generally not desirable. This is important when companies are deciding what quantities of an item to purchase.

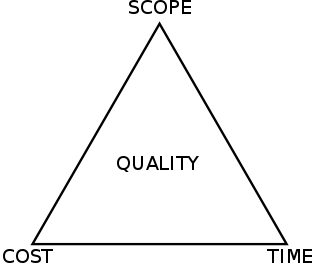

The project management triangle is a model of the constraints of project management. While its origins are unclear, it has been used since at least the 1950s. It contends that:

The quality of work is constrained by the project's budget, deadlines and scope (features).

The project manager can trade between constraints.

Changes in one constraint necessitate changes in others to compensate or quality will suffer.

Management by exception (MBE) is a style of business management that focuses on identifying and handling cases that deviate from the norm, recommended as best practice by the project management method.

The profit model is the linear, deterministic algebraic model used implicitly by most cost accountants. Starting with, profit equals sales minus costs, it provides a structure for modeling cost elements such as materials, losses, multi-products, learning, depreciation etc. It provides a mutable conceptual base for spreadsheet modelers. This enables them to run deterministic simulations or 'what if' modelling to see the impact of price, cost or quantity changes on profitability.

Standard cost accounting is a traditional cost accounting method introduced in the 1920s, as an alternative for the traditional cost accounting method based on historical costs.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.