Related Research Articles

Insurance is a means of protection from financial loss. It is a form of risk management, primarily used to hedge against the risk of a contingent or uncertain loss.

Financial economics is the branch of economics characterized by a "concentration on monetary activities", in which "money of one type or another is likely to appear on both sides of a trade". Its concern is thus the interrelation of financial variables, such as prices, interest rates and shares, as opposed to those concerning the real economy. It has two main areas of focus: asset pricing and corporate finance; the first being the perspective of providers of capital, i.e. investors, and the second of users of capital.

The Black–Scholes or Black–Scholes–Merton model is a mathematical model for the dynamics of a financial market containing derivative investment instruments. From the partial differential equation in the model, known as the Black–Scholes equation, one can deduce the Black–Scholes formula, which gives a theoretical estimate of the price of European-style options and shows that the option has a unique price regardless of the risk of the security and its expected return. The formula led to a boom in options trading and provided mathematical legitimacy to the activities of the Chicago Board Options Exchange and other options markets around the world. It is widely used, although often with adjustments and corrections, by options market participants.

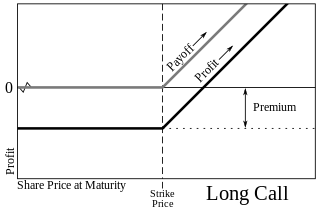

A call option, often simply labeled a "call", is a financial contract between two parties, the buyer and the seller of this type of option. The buyer of the call option has the right, but not the obligation, to buy an agreed quantity of a particular commodity or financial instrument from the seller of the option at a certain time for a certain price. The seller is obligated to sell the commodity or financial instrument to the buyer if the buyer so decides. The buyer pays a fee for this right. The term "call" comes from the fact that the owner has the right to "call the stock away" from the seller.

In finance, a put or put option is a stock market device which gives the owner the right, but not the obligation, to sell an asset, at a specified price, by a predetermined date to a given party. The purchase of a put option is interpreted as a negative sentiment about the future value of the underlying stock. The term "put" comes from the fact that the owner has the right to "put up for sale" the stock or index.

Real options valuation, also often termed real options analysis, applies option valuation techniques to capital budgeting decisions. A real option itself, is the right—but not the obligation—to undertake certain business initiatives, such as deferring, abandoning, expanding, staging, or contracting a capital investment project. For example, the opportunity to invest in the expansion of a firm's factory, or alternatively to sell the factory, is a real call or put option, respectively.

An interest rate cap is a type of interest rate derivative in which the buyer receives payments at the end of each period in which the interest rate exceeds the agreed strike price. An example of a cap would be an agreement to receive a payment for each month the LIBOR rate exceeds 2.5%.

A hedge is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. A hedge can be constructed from many types of financial instruments, including stocks, exchange-traded funds, insurance, forward contracts, swaps, options, gambles, many types of over-the-counter and derivative products, and futures contracts.

In finance, a convertible bond or convertible note or convertible debt is a type of bond that the holder can convert into a specified number of shares of common stock in the issuing company or cash of equal value. It is a hybrid security with debt- and equity-like features. It originated in the mid-19th century, and was used by early speculators such as Jacob Little and Daniel Drew to counter market cornering.

In finance, the yield curve is a curve showing several yields or interest rates across different contract lengths for a similar debt contract. The curve shows the relation between the interest rate and the time to maturity, known as the "term", of the debt for a given borrower in a given currency. For example, the U.S. dollar interest rates paid on U.S. Treasury securities for various maturities are closely watched by many traders, and are commonly plotted on a graph such as the one on the right which is informally called "the yield curve". More formal mathematical descriptions of this relation are often called the term structure of interest rates.

Volatility risk is the risk of a change of price of a portfolio as a result of changes in the volatility of a risk factor. It usually applies to portfolios of derivatives instruments, where the volatility of its under lyings is a major influencer of prices.

In finance, the beta of an investment indicates whether the investment is more or less volatile than the market as a whole.

A variance swap is an over-the-counter financial derivative that allows one to speculate on or hedge risks associated with the magnitude of movement, i.e. volatility, of some underlying product, like an exchange rate, interest rate, or stock index.

In finance, the yield spread or credit spread is the difference between the quoted rates of return on two different investments, usually of different credit qualities but similar maturities. It is often an indication of the risk premium for one investment product over another. The phrase is a compound of yield and spread.

Financial risk is any of various types of risk associated with financing, including financial transactions that include company loans in risk of default. Often it is understood to include only downside risk, meaning the potential for financial loss and uncertainty about its extent.

The CBOE Volatility Index, known by its ticker symbol VIX, is a popular measure of the stock market's expectation of volatility implied by S&P 500 index options. It is calculated and disseminated on a real-time basis by the Chicago Board Options Exchange (CBOE), and is commonly referred to as the fear index or the fear gauge.

In finance, a price (premium) is paid or received for purchasing or selling options. This price can be split into two components.

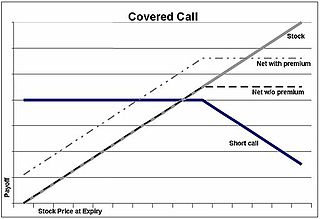

A covered call is a financial market transaction in which the seller of call options owns the corresponding amount of the underlying instrument, such as shares of a stock or other securities. If a trader buys the underlying instrument at the same time the trader sells the call, the strategy is often called a "buy-write" strategy. In equilibrium, the strategy has the same payoffs as writing a put option.

In finance, an option is a contract which gives the buyer the right, but not the obligation, to buy or sell an underlying asset or instrument at a specified strike price prior to or on a specified date, depending on the form of the option. The strike price may be set by reference to the spot price of the underlying security or commodity on the day an option is taken out, or it may be fixed at a discount or at a premium. The seller has the corresponding obligation to fulfill the transaction – to sell or buy – if the buyer (owner) "exercises" the option. An option that conveys to the owner the right to buy at a specific price is referred to as a call; an option that conveys the right of the owner to sell at a specific price is referred to as a put. Both are commonly traded, but the call option is more frequently discussed.

Variance risk premium is a phenomenon on the variance swap market, of the variance swap strike being greater than the realized variance on average. For most trades, the buyer of variance ends up with a loss on the trade, while the seller profits. The amount that the buyer of variance typically loses in entering into the variance swap, is known as the variance risk premium. The variance risk premium can be naively justified by taking into account the large negative convexity of a short variance position; variance during rare times of crisis can be 50-100 times that of normal market conditions.

References

- ↑ Stochastic volatility and the pricing of financial derivatives by Antoine Petrus Cornelius van der Ploeg 2006, University of Amsterdam ISBN 90-5170-577-8 page 256