A tax is a compulsory financial charge or some other type of levy imposed on a taxpayer by a governmental organization in order to collectively fund government spending, public expenditures, or as a way to regulate and reduce negative externalities. Tax compliance refers to policy actions and individual behaviour aimed at ensuring that taxpayers are paying the right amount of tax at the right time and securing the correct tax allowances and tax relief. The first known taxation took place in Ancient Egypt around 3000–2800 BC. Taxes consist of direct or indirect taxes and may be paid in money or as its labor equivalent.

Ballot Measure 5 was a landmark piece of direct legislation in the U.S. state of Oregon in 1990. Measure 5, an amendment to the Oregon Constitution, established limits on Oregon's property taxes on real estate. Its primary champion and spokesman was Don McIntire, a politically-active Gresham health club owner who would go on to lead the Taxpayers Association of Oregon.

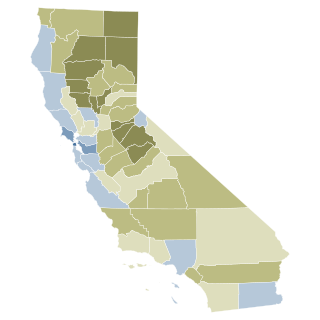

Proposition 13 is an amendment of the Constitution of California enacted during 1978, by means of the initiative process. The initiative was approved by California voters on June 6, 1978. It was upheld as constitutional by the United States Supreme Court in the case of Nordlinger v. Hahn, 505 U.S. 1 (1992). Proposition 13 is embodied in Article XIII A of the Constitution of the State of California.

Equalization payments are cash payments made in some federal systems of government from the federal government to subnational governments with the objective of offsetting differences in available revenue or in the cost of providing services. Many federations use fiscal equalisation to reduce the inequalities in the fiscal capacities of sub-national governments arising from the differences in their geography, demography, natural endowments and economies. The level of equalisation sought can vary, however.

Taxation in the United Kingdom may involve payments to at least three different levels of government: central government, devolved governments and local government. Central government revenues come primarily from income tax, National Insurance contributions, value added tax, corporation tax and fuel duty. Local government revenues come primarily from grants from central government funds, business rates in England, Council Tax and increasingly from fees and charges such as those for on-street parking. In the fiscal year 2014–15, total government revenue was forecast to be £648 billion, or 37.7 per cent of GDP, with net taxes and National Insurance contributions standing at £606 billion.

The State of New Hampshire has a republican form of government modeled after the Government of the United States, with three branches: the executive, consisting of the Governor of New Hampshire and the other elected constitutional officers; the legislative, called the New Hampshire General Court, which includes the Senate and the House of Representatives; and the judicial, consisting of the Supreme Court of New Hampshire and lower courts.

Massachusetts shares with the five other New England states a governmental structure known as the New England town. Only the southeastern third of the state has functioning county governments; in western, central, and northeastern Massachusetts, traditional county-level government was eliminated in the late 1990s. Generally speaking, there are four kinds of public school districts in Massachusetts: local schools, regional schools, vocational/technical schools, and charter schools.

The United States budget comprises the spending and revenues of the U.S. federal government. The budget is the financial representation of the priorities of the government, reflecting historical debates and competing economic philosophies. The government primarily spends on healthcare, retirement, and defense programs. The non-partisan Congressional Budget Office provides extensive analysis of the budget and its economic effects. It has reported that large budget deficits over the next 30 years are projected to drive federal debt held by the public to unprecedented levels—from 98 percent of gross domestic product (GDP) in 2020 to 195 percent by 2050.

At the 2004 and 2005 town meetings, the citizens of the ski resort community of Killington, Vermont, voted in favor of pursuing secession from Vermont and admission into the state of New Hampshire, which lies 25 miles (40 km) to the east.

The government of Vermont is a republican form of government modeled after the Government of the United States. The Constitution of Vermont is the supreme law of the state, followed by the Vermont Statutes. This is roughly analogous to the Federal United States Constitution, United States Code and Code of Federal Regulations respectively. Provision is made for the following frame of government under the Constitution of the State of Vermont: the executive branch, the legislative branch, and the judicial branch. All members of the executive and legislative branch serve two-year terms including the governor and senators. There are no term limits for any office.

The Connecticut Supreme Court issued its ruling in Horton v. Meskill on April 19, 1977. It held that the right to education in Connecticut is so basic and fundamental that any intrusion on the right must be strictly scrutinized. The Court said that public school students are entitled to equal enjoyment of the right to education, and a system of school financing that relied on local property tax revenues without regard to disparities in town wealth and that lacked significant equalizing state support was unconstitutional. It could not pass the test of strict judicial scrutiny. The Court also held that the creation of a constitutional system for education financing is a job for the legislature and not the courts.

Transfer payments are a collection of payments made by the Government of Canada to Canadian provinces and territories under the Federal–Provincial Arrangements Act. Chief among these are the Canada Social Transfer, the Canada Health Transfer and equalization payments. The last of these can be spent however the receiving provinces see fit, while the first two are intended to support social and health services respectively.

The North Country Supervisory Union is a school district responsible for the education of students in the Vermont towns of the city of Newport, Newport Town, Derby, Charleston, Jay, Troy, North Troy, Coventry, Brighton, Holland, Morgan, Westfield, and Lowell. It is administered by a school board.

The New York State School Tax Relief Program, or New York State Real Property Tax Law §425, is a school tax rebate program offered in New York State aimed at reducing school district property taxes on the primary residences of New York residents. In New York City, the STAR Program is a tax exemption for those who applied before Fiscal Year 2015-2016 and a tax credit there after for new applicants. The program, which acts similarly to homestead exemptions in other states, was enacted on August 7, 1997, a product of the annual budget of then-Governor George Pataki.

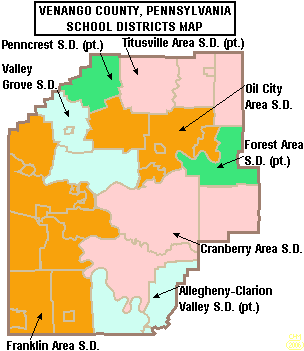

The Cranberry Area School District is a small, rural, public school district which serves the residents of Cranberry Township, Pinegrove Township and Rockland Township in Venango County, Pennsylvania. Cranberry Area School District encompasses approximately 155 square miles (400 km2). According to 2000 federal census data, it serves a resident population of 9,698. In 2009, the per capita income of district residents was $16,307, while the median family income was $39,203 a year. In the Commonwealth, the median family income was $49,501 and the United States median family income was $49,445, in 2010. Per school district officials, in school year 2007-08 the Cranberry Area School District provided basic educational services to 1271 pupils through the employment of 115 teachers, 77 full-time and part-time support personnel, and 7 administrators. In 2006, the 1,308 student population was 98% white, 1% black, 1% Asian, Native American <0.1% and <0.2% Hispanic. The Cranberry Area School District received more than $9 million in state funding, for school year 2007-08.

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property, multiplied by an assessment ratio, multiplied by a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other types of taxes. The property tax typically produces the required revenue for municipalities' tax levies. One disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

In Louisiana, the Minimum Foundation Program is the formula that determines the cost to educate students at public elementary and secondary schools and defines state and local funding contributions to each district. Education officials often use the term "MFP" to refer specifically to the portion the state pays per student to each school district.

Public schools in the United States of America provide basic education from kindergarten until the twelfth grade. This is provided free of charge for the students and parents, but is paid for by taxes on property owners as well as general taxes collected by the federal government. This education is mandated by the states. With the completion of this basic schooling, one obtains a high school diploma as certification of basic skills for employers.

Bois Blanc Pines School District is a public school district located in Bois Blanc Township in the U.S. state of Michigan. The district had an enrollment of four students for the 2021–22 school year. It ranks as the smallest district in the state in terms of enrollment and among the smallest in the nation. The district contains one school, Pines School Elementary, which is a one-room schoolhouse that provides K–8 primary education. It is one of the last functioning one-room schoolhouses in the state of Michigan.

California Proposition 15 was a failed citizen-initiated proposition on the November 3, 2020, ballot. It would have provided $6.5 billion to $11.5 billion in new funding for public schools, community colleges, and local government services by creating a "split roll" system that increased taxes on large commercial properties by assessing them at market value, without changing property taxes for small business owners or residential properties for homeowners or renters. The measure failed by a small margin of about four percentage points.