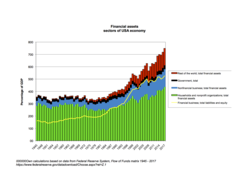

Net financial assets of sectors of US economy, 1945-2017Liabilities of sectors of US economy, 1945-2017, based on flow of funds statistics of the Federal Reserve System.Financial assets of sectors of US economy, 1945-2017, based on flow of funds statistics of the Federal Reserve System.

An asset in economic theory is a durable good which can only be partially consumed (like a portable music player) or input as a factor of production (like a cement mixer) which can only be partially used up in production. The necessary quality for an asset is that value remains after the period of analysis so it can be used as a store of value. As such, financial instruments like corporate bonds and common stocks are assets because they store value for the next period. If the good or factor is used up before the next period, there would be nothing upon which to place a value.

As a result of this definition, assets only have positive future prices. This is analogous to the distinction between consumer durables and non-durables. Durables last more than one year. A classic durable is an automobile. A classic non-durable is an apple, which is eaten and lasts less than one year. Assets are that category of output which economic theory places prices upon. In a simple Walrasian equilibrium model, there is but a single period and all items have prices. In a multi-period equilibrium model, while all items have prices in the current period. Only assets can survive into the next period and thus only assets can store value and as a result, only assets have a price today for delivery tomorrow. Items which depreciate 100% by tomorrow have no price for delivery tomorrow because by tomorrow it ceases to exist.

The subfield of asset pricing (or valuation) is the financial evaluation of the value of such assets; the primary method used by today's financial analysts is the discounted cash flow method. With this method, an asset's future cash flows are either assumed to be known with certainty (as in a treasury bond which is risk free) or estimated. These future cash flows are discounting used present values.

The Flow of Funds tables from the Federal Reserve System provide data about assets, which are tangible assets and financial assets, and liabilities. The difference, assets minus liabilities, is net worth.

In economics and finance, arbitrage is the practice of taking advantage of a difference in prices in two or more markets – striking a combination of matching deals to capitalize on the difference, the profit being the difference between the market prices at which the unit is traded. When used by academics, an arbitrage is a transaction that involves no negative cash flow at any probabilistic or temporal state and a positive cash flow in at least one state; in simple terms, it is the possibility of a risk-free profit after transaction costs. For example, an arbitrage opportunity is present when there is the possibility to instantaneously buy something for a low price and sell it for a higher price.

The discounted cash flow (DCF) analysis, in financial analysis, is a method used to value a security, project, company, or asset, that incorporates the time value of money. Discounted cash flow analysis is widely used in investment finance, real estate development, corporate financial management, and patent valuation. Used in industry as early as the 1700s or 1800s, it was widely discussed in financial economics in the 1960s, and U.S. courts began employing the concept in the 1980s and 1990s.

Fundamental analysis, in accounting and finance, is the analysis of a business's financial statements ; health; competitors and markets. It also considers the overall state of the economy and factors including interest rates, production, earnings, employment, GDP, housing, manufacturing and management. There are two basic approaches that can be used: bottom up analysis and top down analysis. These terms are used to distinguish such analysis from other types of investment analysis, such as quantitative and technical.

In finance, discounting is a mechanism in which a debtor obtains the right to delay payments to a creditor, for a defined period of time, in exchange for a charge or fee. Essentially, the party that owes money in the present purchases the right to delay the payment until some future date. This transaction is based on the fact that most people prefer current interest to delayed interest because of mortality effects, impatience effects, and salience effects. The discount, or charge, is the difference between the original amount owed in the present and the amount that has to be paid in the future to settle the debt.

The net present value (NPV) or net present worth (NPW) is a way of measuring the value of an asset that has cashflow by adding up the present value of all the future cash flows that asset will generate. The present value of a cash flow depends on the interval of time between now and the cash flow because of the Time value of money. It provides a method for evaluating and comparing capital projects or financial products with cash flows spread over time, as in loans, investments, payouts from insurance contracts plus many other applications.

Financial economics is the branch of economics characterized by a "concentration on monetary activities", in which "money of one type or another is likely to appear on both sides of a trade". Its concern is thus the interrelation of financial variables, such as share prices, interest rates and exchange rates, as opposed to those concerning the real economy. It has two main areas of focus: asset pricing and corporate finance; the first being the perspective of providers of capital, i.e. investors, and the second of users of capital. It thus provides the theoretical underpinning for much of finance.

Factoring is a financial transaction and a type of debtor finance in which a business sells its accounts receivable to a third party at a discount. A business will sometimes factor its receivable assets to meet its present and immediate cash needs. Forfaiting is a factoring arrangement used in international trade finance by exporters who wish to sell their receivables to a forfaiter. Factoring is commonly referred to as accounts receivable factoring, invoice factoring, and sometimes accounts receivable financing. Accounts receivable financing is a term more accurately used to describe a form of asset based lending against accounts receivable. The Commercial Finance Association is the leading trade association of the asset-based lending and factoring industries.

In finance, valuation is the process of determining the value of a (potential) investment, asset, or security. Generally, there are three approaches taken, namely discounted cashflow valuation, relative valuation, and contingent claim valuation.

In financial accounting, a cash flow statement, also known as statement of cash flows, is a financial statement that shows how changes in balance sheet accounts and income affect cash and cash equivalents, and breaks the analysis down to operating, investing and financing activities. Essentially, the cash flow statement is concerned with the flow of cash in and out of the business. As an analytical tool, the statement of cash flows is useful in determining the short-term viability of a company, particularly its ability to pay bills. International Accounting Standard 7 is the International Accounting Standard that deals with cash flow statements.

In accounting, fair value is a rational and unbiased estimate of the potential market price of a good, service, or asset. The derivation takes into account such objective factors as the costs associated with production or replacement, market conditions and matters of supply and demand. Subjective factors may also be considered such as the risk characteristics, the cost of and return on capital, and individually perceived utility.

Stock valuation is the method of calculating theoretical values of companies and their stocks. The main use of these methods is to predict future market prices, or more generally, potential market prices, and thus to profit from price movement – stocks that are judged undervalued are bought, while stocks that are judged overvalued are sold, in the expectation that undervalued stocks will overall rise in value, while overvalued stocks will generally decrease in value. A target price is a price at which an analyst believes a stock to be fairly valued relative to its projected and historical earnings.

Rational pricing is the assumption in financial economics that asset prices – and hence asset pricing models – will reflect the arbitrage-free price of the asset as any deviation from this price will be "arbitraged away". This assumption is useful in pricing fixed income securities, particularly bonds, and is fundamental to the pricing of derivative instruments.

Enterprise value (EV), total enterprise value (TEV), or firm value (FV) is an economic measure reflecting the market value of a business. It is a sum of claims by all claimants: creditors and shareholders. Enterprise value is one of the fundamental metrics used in business valuation, financial analysis, accounting, portfolio analysis, and risk analysis.

Liquidity risk is a financial risk that for a certain period of time a given financial asset, security or commodity cannot be traded quickly enough in the market without impacting the market price.

Business valuation is a process and a set of procedures used to estimate the economic value of an owner's interest in a business. Here various valuation techniques are used by financial market participants to determine the price they are willing to pay or receive to effect a sale of the business. In addition to estimating the selling price of a business, the same valuation tools are often used by business appraisers to resolve disputes related to estate and gift taxation, divorce litigation, allocate business purchase price among business assets, establish a formula for estimating the value of partners' ownership interest for buy-sell agreements, and many other business and legal purposes such as in shareholders deadlock, divorce litigation and estate contest.

A housing bubble is one of several types of asset price bubbles which periodically occur in the market. The basic concept of a housing bubble is the same as for other asset bubbles, consisting of two main phases. First there is a period where house prices increase dramatically, driven more and more by speculation. In the second phase, house prices fall dramatically. Housing bubbles tend to be among the asset bubbles with the largest effect on the real economy, because they are credit-fueled, because a large number of households participate and not just investors, and because the wealth effect from housing tends to be larger than for other types of financial assets.

The revenue recognition principle is a cornerstone of accrual accounting together with the matching principle. They both determine the accounting period in which revenues and expenses are recognized. According to the principle, revenues are recognized when they are realized or realizable, and are earned, no matter when cash is received. In cash accounting—in contrast—revenues are recognized when cash is received no matter when goods or services are sold.

Valuation using discounted cash flows is a method of estimating the current value of a company based on projected future cash flows adjusted for the time value of money. The cash flows are made up of those within the “explicit” forecast period, together with a continuing or terminal value that represents the cash flow stream after the forecast period. In several contexts, DCF valuation is referred to as the "income approach".

In economics, valuation using multiples, or "relative valuation", is a process that consists of:

The following outline is provided as an overview of and topical guide to finance:

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.