Related Research Articles

In finance, a bond is a type of security under which the issuer (debtor) owes the holder (creditor) a debt, and is obliged – depending on the terms – to provide cash flow to the creditor The timing and the amount of cash flow provided varies, depending on the economic value that is emphasized upon, thus giving rise to different types of bonds. The interest is usually payable at fixed intervals: semiannual, annual, and less often at other periods. Thus, a bond is a form of loan or IOU. Bonds provide the borrower with external funds to finance long-term investments or, in the case of government bonds, to finance current expenditure.

A government bond or sovereign bond is a form of bond issued by a government to support public spending. It generally includes a commitment to pay periodic interest, called coupon payments, and to repay the face value on the maturity date.

In finance, a convertible bond, convertible note, or convertible debt is a type of bond that the holder can convert into a specified number of shares of common stock in the issuing company or cash of equal value. It is a hybrid security with debt- and equity-like features. It originated in the mid-19th century, and was used by early speculators such as Jacob Little and Daniel Drew to counter market cornering.

In finance, a holdout problem occurs when a bond issuer is in default or nears default, and launches an exchange offer in an attempt to restructure debt held by existing bond holders. Such exchange offers typically require the consent of holders of some minimum portion of the total outstanding debt, often in excess of 90%, because, unless the terms of the bond provide otherwise, non-consenting bondholders will retain their legal right to demand repayment of their bonds at par. Bondholders who withhold their consent and retain their right to seek the full repayment of original bonds, may disrupt the restructuring process, creating a situation known as the holdout problem.

A collateralized mortgage obligation (CMO) is a type of complex debt security that repackages and directs the payments of principal and interest from a collateral pool to different types and maturities of securities, thereby meeting investor needs.

Cleary Gottlieb Steen & Hamilton LLP, formerly Cleary, Gottlieb, Friendly & Cox and Cleary, Gottlieb, Friendly, Steen & Hamilton, is an American multinational law firm headquartered at One Liberty Plaza in New York City. Known as a white shoe law firm, Cleary employs over 1,200 lawyers worldwide.

In corporate finance, distressed securities are securities over companies or government entities that are experiencing financial or operational distress, default, or are under bankruptcy. As far as debt securities, this is called distressed debt. Purchasing or holding such distressed-debt creates significant risk due to the possibility that bankruptcy may render such securities worthless.

A vulture fund is a hedge fund or private-equity fund that invests in debt considered to be very weak or in default, known as distressed debt. Investors in the fund profit by buying debt at a discounted price on a secondary market and then using numerous methods to sell the debt for more than the purchasing price. Debtors include companies, countries, and individuals.

The Argentine debt restructuring is a process of debt restructuring by Argentina that began on January 14, 2005, and allowed it to resume payment on 76% of the US$82 billion in sovereign bonds that defaulted in 2001 at the depth of the worst economic crisis in the nation's history. A second debt restructuring in 2010 brought the percentage of bonds under some form of repayment to 93%, though ongoing disputes with holdouts remained. Bondholders who participated in the restructuring settled for repayments of around 30% of face value and deferred payment terms, as well as warrants that paid investors based on annual economic growth as part of the same offer, and began to be paid punctually; the value of their nearly worthless bonds also began to rise. The remaining 7% of bondholders were later repaid 25% less than they were demanding, after centre-right and US-aligned leader Mauricio Macri came to power in 2015.

David Martínez Guzmán is a Mexican investor who is the founder and managing partner of Fintech Advisory. This firm specializes in corporate and sovereign debt. Fintech Advisory has offices in London and New York City, and he currently divides his time between those two cities.

A sovereign default is the failure or refusal of the government of a sovereign state to pay back its debt in full when due. Cessation of due payments may either be accompanied by that government's formal declaration that it will not pay its debts (repudiation), or it may be unannounced. A credit rating agency will take into account in its gradings capital, interest, extraneous and procedural defaults, and failures to abide by the terms of bonds or other debt instruments.

In finance, a GDP-linked bond is a debt security or derivative security in which the authorized issuer promises to pay a return, in addition to amortization, that varies with the behavior of Gross Domestic Product (GDP). This type of security can be thought as a “stock on a country” in the sense that it has “equity-like” features. It pays more/less when the performance of the country is better/worse than expected. Nevertheless, it is substantially different from a stock because there are no ownership-rights over the country.

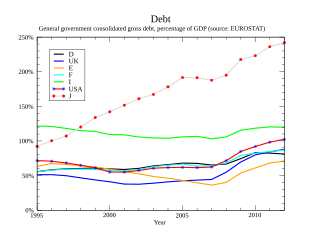

Debt crisis is a situation in which a government loses the ability of paying back its governmental debt. When the expenditures of a government are more than its tax revenues for a prolonged period, the government may enter into a debt crisis. Various forms of governments finance their expenditures primarily by raising money through taxation. When tax revenues are insufficient, the government can make up the difference by issuing debt.

In the context of sovereign debt crisis, private sector involvement (PSI) refers, broadly speaking, to the forced contribution of private sector creditors to a financial crisis resolution process, and, specifically, to the private sector incurring outright reductions ("haircuts") on the value of its debt holdings.

The Puerto Rican government-debt crisis was a financial crisis affecting the government of Puerto Rico. The crisis began in 2014 when three major credit agencies downgraded several bond issues by Puerto Rico to "junk status" after the government was unable to demonstrate that it could pay its debt. The downgrades, in turn, prevented the government from selling more bonds in the open market. Unable to obtain the funding to cover its budget imbalance, the government began using its savings to pay its debt while warning that those savings would eventually be exhausted. To prevent such a scenario, the United States Congress enacted a law known as PROMESA, which appointed an oversight board with ultimate control over the Commonwealth's budget. As the PROMESA board began to exert that control, the Puerto Rican government sought to increase revenues and reduce its expenses by increasing taxes while curtailing public services and reducing government pensions. These measures provoked social distrust and unrest, further compounding the crisis. In August 2018, a debt investigation report of the Financial Oversight and management board for Puerto Rico reported the Commonwealth had $74 billion in bond debt and $49 billion in unfunded pension liabilities as of May 2017. Puerto Rico officially exited bankruptcy on March 15, 2022.

Kenneth Bryan Dart is a Cayman Islands-based billionaire businessman. His family founded Dart Container, a food and beverage packaging company and the owner of the Solo Cup Company. Dart owns real estate development and investment companies in the U.S. and Cayman Islands and developed the town of Camana Bay. He maintains a low profile and is known for his focus on privacy. He is also a citizen of Belize and Ireland.

The Second Economic Adjustment Programme for Greece, usually referred to as the second bailout package or the second memorandum, is a memorandum of understanding on financial assistance to the Hellenic Republic in order to cope with the Greek government-debt crisis.

Beginning in 1969, the government of Peru issued sovereign bonds as compensation for land expropriation during the Peruvian land reform under General Juan Velasco Alvarado. The government's aim was to redistribute land and reform the country's agrarian infrastructure. Payments on these bonds halted in 1992 due to periods of hyperinflation. The agrarian bonds have been recognized as outstanding sovereign debt obligations by Peru's highest courts, who have stated that these bonds should be repaid. However, today the debt remains unpaid, and the government of Peru has yet to clarify means and ultimate value of compensation to current bondholders.

Greylock Capital Management, LLC is a U.S. Securities and Exchange Commission registered alternative investment adviser that invests globally in high yield, undervalued, and distressed assets worldwide, particularly in emerging and frontier markets. The firm was founded in 2004 by Hans Humes from a portfolio of emerging market assets managed by Humes while at Van Eck Global. AJ Mediratta joined the firm in 2008 from Bear Stearns and serves as its president.

State defaults in the United States are instances of states within the United States defaulting on their debt. The last instance of such a default took place during the Great Depression, in 1933, when the state of Arkansas defaulted on its highway bonds, which had long-lasting consequences for the state. Current U.S. bankruptcy law, an area governed by federal law, does not allow a state to file for bankruptcy under the Bankruptcy Code. Certain politicians and scholars have argued that the law should be amended to allow states to file for bankruptcy.

References

- 1 2 WSJ.com: "2nd UPDATE: Greece To Introduce Retroactive Collective Action Clauses-Source" 9 Jan 2012

- 1 2 3 4 5 bloomberg.com: "Greece Pushes Bondholders Into Record Debt Swap" 9 Mar 2012

- ↑ Collective Action Clauses: No Panacea for Sovereign Debt Restructurings

- ↑ Collective Action Clauses in Euro area Archived 2014-08-11 at the Wayback Machine