The Austrian school is a heterodox school of economic thought that advocates strict adherence to methodological individualism, the concept that social phenomena result primarily from the motivations and actions of individuals along with their self interest. Austrian-school theorists hold that economic theory should be exclusively derived from basic principles of human action.

Keynesian economics are the various macroeconomic theories and models of how aggregate demand strongly influences economic output and inflation. In the Keynesian view, aggregate demand does not necessarily equal the productive capacity of the economy. It is influenced by a host of factors that sometimes behave erratically and impact production, employment, and inflation.

Neoclassical economics is an approach to economics in which the production, consumption, and valuation (pricing) of goods and services are observed as driven by the supply and demand model. According to this line of thought, the value of a good or service is determined through a hypothetical maximization of utility by income-constrained individuals and of profits by firms facing production costs and employing available information and factors of production. This approach has often been justified by appealing to rational choice theory.

Classical economics, classical political economy, or Smithian economics is a school of thought in political economy that flourished, primarily in Britain, in the late 18th and early-to-mid-19th century. Its main thinkers are held to be Adam Smith, Jean-Baptiste Say, David Ricardo, Thomas Robert Malthus, and John Stuart Mill. These economists produced a theory of market economies as largely self-regulating systems, governed by natural laws of production and exchange.

Steve Keen is an Australian economist and author. He considers himself a post-Keynesian, criticising neoclassical economics as inconsistent, unscientific, and empirically unsupported.

Market fundamentalism, also known as free-market fundamentalism, is a term applied to a strong belief in the ability of unregulated laissez-faire or free-market capitalist policies to solve most economic and social problems. It is often used as pejorative by critics of said beliefs.

Heterodox economics is a broad, relative term referring to schools of economic thought which are not commonly perceived as belonging to mainstream economics. There is no absolute definition of what constitutes heterodox economic thought, as it is defined in constrast to the most prominent, influential or popular schools of thought in a given time and place.

The Austrian business cycle theory (ABCT) is an economic theory developed by the Austrian School of economics seeking to explain how business cycles occur. The theory views business cycles as the consequence of excessive growth in bank credit due to artificially low interest rates set by a central bank or fractional reserve banks. The Austrian business cycle theory originated in the work of Austrian School economists Ludwig von Mises and Friedrich Hayek. Hayek won the Nobel Prize in Economics in 1974 in part for his work on this theory.

In economics, economic value is a measure of the benefit provided by a good or service to an economic agent, and value for money represents an assessment of whether financial or other resources are being used effectively in order to secure such benefit. Economic value is generally measured through units of currency, and the interpretation is therefore "what is the maximum amount of money a person is willing and able to pay for a good or service?” Value for money is often expressed in comparative terms, such as "better", or "best value for money", but may also be expressed in absolute terms, such as where a deal does, or does not, offer value for money.

The law of supply is a fundamental principle of economic theory which states that, keeping other factors constant, an increase in sales price results in an increase in quantity supplied. In other words, there is a direct relationship between price and quantity: quantities respond in the same direction as price changes. This means that producers and manufacturers are willing to offer more of a product for sale on the market at higher prices, as increasing production is a way of increasing profits.

George Lennox Sharman Shackle was an English economist. He made a practical attempt to challenge classical rational choice theory and has been characterised as a "post-Keynesian", though he is influenced as well by Austrian economics. Much of his work is associated with the Dempster–Shafer theory of evidence.

Mainstream economics is the body of knowledge, theories, and models of economics, as taught by universities worldwide, that are generally accepted by economists as a basis for discussion. Also known as orthodox economics, it can be contrasted to heterodox economics, which encompasses various schools or approaches that are only accepted by a small minority of economists.

Herbert Joseph Davenport was an American economist and critic of the Austrian School, educator and author.

In the history of economic thought, a school of economic thought is a group of economic thinkers who share or shared a mutual perspective on the way economies function. While economists do not always fit within particular schools, particularly in the modern era, classifying economists into schools of thought is common. Economic thought may be roughly divided into three phases: premodern, early modern and modern. Systematic economic theory has been developed primarily since the beginning of what is termed the modern era.

Macroeconomic theory has its origins in the study of business cycles and monetary theory. In general, early theorists believed monetary factors could not affect real factors such as real output. John Maynard Keynes attacked some of these "classical" theories and produced a general theory that described the whole economy in terms of aggregates rather than individual, microeconomic parts. Attempting to explain unemployment and recessions, he noticed the tendency for people and businesses to hoard cash and avoid investment during a recession. He argued that this invalidated the assumptions of classical economists who thought that markets always clear, leaving no surplus of goods and no willing labor left idle.

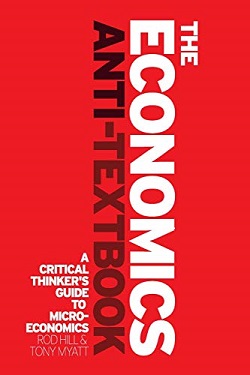

The Economics Anti-Textbook is both an introduction to, and critique of the typical approaches to economics teaching, written by Roderick Hill and Tony Myatt in 2010. The main thrust of the authors' argument is that basic economics courses, being centered on models of perfect competition, are biased towards the support of free market or laissez-faire ideologies, and neglect to mention conflicting evidence or give sufficient coverage of alternative descriptive models. This book has been updated and superseded by The Microeconomics Anti-Textbook and The Macroeconomics Anti-Textbook, by the same authors.

The Cambridge capital controversy, sometimes called "the capital controversy" or "the two Cambridges debate", was a dispute between proponents of two differing theoretical and mathematical positions in economics that started in the 1950s and lasted well into the 1960s. The debate concerned the nature and role of capital goods and a critique of the neoclassical vision of aggregate production and distribution. The name arises from the location of the principals involved in the controversy: the debate was largely between economists such as Joan Robinson and Piero Sraffa at the University of Cambridge in England and economists such as Paul Samuelson and Robert Solow at the Massachusetts Institute of Technology, in Cambridge, Massachusetts, United States.

Economyths is a book by the mathematician David Orrell about the problems with mainstream economics, written for the general reader. The book was initially published in 2010 by Icon Books in the UK with the subtitle Ten Ways That Economics Gets it Wrong, and by John Wiley & Sons in North America. Icon published a revised version in 2012, with the subtitle How the Science of Complex Systems Is Transforming Economic Thought. Translated versions were also published in Brazil, China, Japan, and Korea. In 2017, Icon published a revised and expanded version with the subtitle 11 Ways Economics Gets it Wrong.

Most economic models rest on a number of assumptions that are not entirely realistic. For example, agents are often assumed to have perfect information, and markets are often assumed to clear without friction. Or, the model may omit issues that are important to the question being considered, such as externalities. Any analysis of the results of an economic model must therefore consider the extent to which these results may be compromised by inaccuracies in these assumptions, and there is a growing literature debunking economics and economic models.