This article needs to be updated.(January 2016) |

| Disability |

|---|

A disability pension is a form of pension given to those people who are permanently or temporarily unable to work due to a disability.

This article needs to be updated.(January 2016) |

| Disability |

|---|

A disability pension is a form of pension given to those people who are permanently or temporarily unable to work due to a disability.

An example of a disability pension is from a private or Public Pension Plan, or the Canada Pension Plan. Another example is Social Security Disability Insurance (SSDI) in the United States.

Generally, there is a minimum time of service required to be eligible for the disability retirement benefit. The claimant might be directed to sign a waiver for their medical records to be disclosed and commonly is scheduled for an independent medical evaluation (IME) to confirm they are permanently disabled. The pension is calculated based on years worked, so the disability retiree can retire earlier (since they are unable to work), but receives an equitable pension based on years of service.

Australian residents of working age who are unable to work for 15 hours a week for the next two years are eligible for the Disability Support Pension. Those intending to claim the DSP need to provide a report from their treating doctor. [1]

Beneficiaries of the Disability Support Pension receive significantly more than those on unemployment benefits; as of 1 October 2023 the basic rate is A$1096.70 per fortnight for singles with a child under care and A$826.70 for each member of a couple. [2]

The Disability Support Pension, previously known as the Invalid Pension, were first introduced in the state of New South Wales in 1908. The Commonwealth government introduced a nationwide Invalid Pension on 5 December 1910. [3] [4]

Australians who are temporarily unable to work due to illness, injury or a short-term disability may be eligible for Sickness Allowance. [5] Sickness Allowance pays less than the DSP; as of 1 January 2009, single recipients were entitled to a basic rate of A$449.30 per fortnight and couples A$405.30 for each person. [6] However Sickness allowance was discontinued since 20 September 2020. [7]

Like all Australian social security payments, eligibility for the DSP is not dependent on individual contributions; rather, benefits are paid out of general Commonwealth government revenue. [8]

In New Zealand income support exists for people with physical or mental health issues. The two main disability benefits are the Sickness Benefit, and the Invalid's Benefit. A doctor's referral and medical certificate (or equivalent) is needed to claim the benefits. The Invalid's Benefit is for someone who has a severe disability, and/or long term sickness, which is paid slightly more than the Sickness Benefit. In addition, there is the Disability Allowance, to supplement medical costs. If the Disability Allowance does not pay for all medical costs, then Temporary Additional Support is provided, but obtaining it is more difficult. All of these benefits have maximum limits, depending on such things as income (both the individual and their partner) and cash assets. Note that the Sickness Benefit and Invalid's Benefit are for people aged less than 65 but the Disability Allowance is for anyone over 18 years.

According to central government guidelines, the basic pension insurance is set to 40% of the insured monthly wage. The disabled person is also eligible to receive temporary and permanent disability benefits. Temporary benefits are in the amount of 100% of the individual's wage up to one year. There are 10 degrees of disability, with the percentage of the wage that the person receives ranging from 90%(for a first degree disability) to 60% (for a 6th degree disability). In addition to the pension, the person receives a benefit in the amount of 27 months worth of the person's previous wage (for a first degree disability) to 7 months of wages (for a 10th degree disability). The minimum amount of a benefit is determined by the minimum wage in the area. [9]

Disability pension calculations vary depending on the country. Countries like Czech Republic, Estonia, Ireland, Greece, Croatia, Latvia, Hungary, Slovakia, Finland, Sweden and the United Kingdom apply a risk-based logic. In this case the length of the period when the individual was insured is not important, only that he or she was insured when the invalidity occurred. Other countries use a pro-rata method, were the pension is higher for people who had been insured for a longer time. [10]

• To be able to apply for a disability pension or as it is calles in France pension d'invalidité there should be fulfilled the following conditions: 1-Age requirement: The person has not reached yet the legal age for retirement. (for this country is 62 years old.) 2-Working capacity: The person should have significantly lost his/her capability of working. The person must have a permanent disability over 80% (case of blind people) or vary to a range of 50%-60% disability which is the case of people certified as "unable to procure employment due to a disability". 3-Contributions: The person must have paid at least 12 months social security contributions before the day he/she is diagnosed. 4-Nationality: Being French is not a requirement. Having a proof that proves the legality of the residence in the country is necessary.

• Categories [11] For considering the amount of disability benefit there are 2 factors considered: 1) The salary and the social security contributions and 2) The category of the disability. Categories are divided as follow: 1- 1st Category: This category belongs to people who are still able to do some job that can be paid. The benefit is calculated in this form: SAM X 30%. (Average annual income*30%). The maximum annual amount of the pension is equal to 993.30 Euro per month, considering the social security threshold: €11,919.60. 2- 2nd Category: This category belongs to people who are not capable of paid working and cannot perform professional activities anymore. The benefit is calculated in this form: SAM X 50%. (Average annual income*50%). The maximum annual amount of the pension is equal to €1,655.50 per month, considering the SST (social security threshold): €19,866. 3- 3rd Category: This category belongs to people who are not capable of performing paid working and cannot perform professional activities anymore and are obliged to use assistance of a third person to meet the needs of everyday life. Comparing to previous category, the normal pension is increased by 40% reaching the maximum amount of €2,763 per month.

[SAM: Average yearly income. It represents the pension scheme of employees in its 10 best performance which are revalued and divided by 10. (in the case there are 10 years of work) SST: Social security threshold is the maximum total that is defined each year under basis of which contributions and certain social security allowances are calculated.(In 2018 estimation, annual amount was €39,732)

• Allowance for adults that have disabilities. [12] Apart from pension d'invalidité People with significant disabilities and low incomes can manage to receive an addition allowance named as AAH (allocation aux adultes handicapés). To benefit from this additional help, the factor of low income is strongly considered. For example: in 2017 a single disabled person with no children can be considered in AAH benefit only if the income was lower than 9,730.68 EUR per year.

In the United Kingdom, the government department responsible for benefits for sick and disabled people is the Department for Work and Pensions (DWP).

The United Kingdom pension types for disabled people are:

In order to cover loss of income from illness and disability, there is also Statutory Sick Pay, and its long term equivalent - Employment and Support Allowance (ESA). The new Universal Credit scheme will include an equivalent element for those with long-term unfitness to work; ESA will consequently be abolished by the roll out of Universal Credit.

There used to be a partial and full disability pensions, but as of 2010, there is no longer a difference between these two types. Depending on how severe the disability of the individual is, (i.e. how much their ability to work has decreased) they can be categorized into one of three degrees of disability. The degree of disability is determined by a health and capacity to work evaluation conducted by the Czech Social Security Administration's evaluation service. [13]

| Decrease in ability to work | Degree of disability |

|---|---|

| 35–49% | First degree |

| 50–69% | Second degree |

| 70% and more | Third degree |

An individual has to meet certain requirements in order to apply for a disability pension. A person is not eligible for a disability pension if they have already reached the age of 65, when one is already eligible for a standard old-age pension. The applicant must also meet the required term of insurance which rises with rising age. In case of an individual younger than 20 years, less than one year of insurance contributions are required. When the applicant is over 28 years old it is required that he has made at least 5 years of insurance contributions in his past 10 years. At an age higher than 38, 10 ears of previous insurance contributions are required. The required term of insurance is waived if the applicant's disability is from an accident at work or occupational disease or if the applicant has been declared disabled since childhood. [13]

The disability pension consists of two components. The first is a basic amount which is fixed to 9% of average wages (2,700 CZK in 2018) . The second components is a percentage amount from the average of previous wages. The percentage is determined individually from the number of insured years. This amount is higher for higher degrees of disabilities.

An individual is entitled to a disability pension [Pensão de invalidez] when the incompetency to work is certified by Sistema de Verificação de Incapacidades (SVI) [Incapacity Verification System], and the beneficiary has met the minimum qualifying period requirement. [14]

Disability is classified into two categories. It may be relative or absolute. In the case of a relative disability, the beneficiary's earning capacity for his or her own occupation is reduced, and he or she is not expected to recover within the next three years, and the beneficiary has registered earnings for at least five calendar years, consecutive or not. In the case of an absolute disability, the beneficiary is permanently and definitively incapable of working in any occupation and has registered earnings for at least 3 calendar years, consecutive or not. [14]

The amount to be paid as a disability pension varies depending on the beneficiary's registered earnings and security contributions. There are minimum rates, for specific time ranges of contributions of the beneficiary. In addition to monthly disability pensions, the beneficiaries receive an extra payment in July and December as a holiday and Christmas bonus. [14]

Disability pension in Finland is usually paid to an individual after they have already received a sickness benefit for around a year. In the case of not being able to work in their job or a similar one even after that one year, the individual can apply for a disability pension. "Disability pension can be granted to people aged 18–62 who are part of the earnings-related pension system." [15] In case an individual is unable to work at all (specifically if their ability to work has decreased b at least 3/5), they may receive a full disability pension (työkyvyttömyyseläke). If the individual is partially unable to work (specifically if their ability to work has decreased by 2/5), they may receive a partial disability pension, which is half of the full disability pension. [16]

When calculating the amount of the pension, there is a so-called projected pension component added to the pension. The projected pension component is made if the individual

The accrued rate is 1.5% of gross wages for the 5 years prior to disability retirement.

The disability pension can also be increased by a rehabilitation benefit which is an additional 33% of the original pension amount. (2019)

In the United States, Social Security is the commonly used term for the federal Old-Age, Survivors, and Disability Insurance (OASDI) program and is administered by the Social Security Administration (SSA). The Social Security Act was passed in 1935, and the existing version of the Act, as amended, encompasses several social welfare and social insurance programs.

Unemployment benefits, also called unemployment insurance, unemployment payment, unemployment compensation, or simply unemployment, are payments made by authorized bodies to unemployed people. In the United States, benefits are funded by a compulsory governmental insurance system, not taxes on individual citizens. Depending on the jurisdiction and the status of the person, those sums may be small, covering only basic needs, or may compensate the lost time proportionally to the previous earned salary.

State disability insurance is a type of insurance for workers who are ill, unable or injured. It partially replaces wages in the event a worker is unable to perform their work due to a disability. In some states, there are many types of organisations that provide different disability insurance. These organisations have specific definitions regarding what is a disability and how a person should qualify in order to receive the benefit.

Jobseeker's Allowance (JSA) is an unemployment benefit paid by the Government of the United Kingdom to people who are unemployed and actively seeking work. It is part of the social security benefits system and is intended to cover living expenses while the claimant is out of work.

Social Security Disability Insurance is a payroll tax-funded federal insurance program of the United States government. It is managed by the Social Security Administration and designed to provide monthly benefits to people who have a medically determinable disability that restricts their ability to be employed. SSDI does not provide partial or temporary benefits but rather pays only full benefits and only pays benefits in cases in which the disability is "expected to last at least one year or result in death." Relative to disability programs in other countries in the Organisation for Economic Co-operation and Development (OECD), the SSDI program in the United States has strict requirements regarding eligibility.

Income Support is an income-related benefit in the United Kingdom for some people who are on a low income, but have a reason for not actively seeking work. Claimants of Income Support may be entitled to certain other benefits, for example, Housing Benefit, Council Tax Reduction, Child Benefit, Carer's Allowance, Child Tax Credit and help with health costs. A person with capital over £16,000 cannot get Income Support, and savings over £6,000 affect how much Income Support can be received. Claimants must be between 16 and Pension Credit age, work fewer than 16 hours a week, and have a reason why they are not actively seeking work.

Social welfare has long been an important part of New Zealand society and a significant political issue. It is concerned with the provision by the state of benefits and services. Together with fiscal welfare and occupational welfare, it makes up the social policy of New Zealand. Social welfare is mostly funded through general taxation. Since the 1980s welfare has been provided on the basis of need; the exception is universal superannuation.

Social security, in Australia, refers to a system of social welfare payments provided by Australian Government to eligible Australian citizens, permanent residents, and limited international visitors. These payments are almost always administered by Centrelink, a program of Services Australia. In Australia, most payments are means tested.

Retirement Insurance Benefits or old-age insurance benefits are a form of social insurance payments made by the U.S. Social Security Administration paid based upon the attainment of old age. Benefit payments are made on the 3rd of the month, or the 2nd, 3rd, or 4th Wednesday of the month, based upon the date of birth and entitlement to other benefits.

Social security is divided by the French government into five branches: illness; old age/retirement; family; work accident; and occupational disease. From an institutional point of view, French social security is made up of diverse organismes. The system is divided into three main Regimes: the General Regime, the Farm Regime, and the Self-employed Regime. In addition there are numerous special regimes dating from prior to the creation of the state system in the mid-to-late 1940s.

Welfare in France includes all systems whose purpose is to protect people against the financial consequences of social risks.

Disability benefits are funds provided from public or private sources to a person who is ill or who has a disability.

Social security or welfare in Finland is very comprehensive compared to what almost all other countries provide. In the late 1980s, Finland had one of the world's most advanced welfare systems, which guaranteed decent living conditions to all Finns. Created almost entirely during the first three decades after World War II, the social security system was an outgrowth of the traditional Nordic belief that the state is not inherently hostile to the well-being of its citizens and can intervene benevolently on their behalf. According to some social historians, the basis of this belief was a relatively benign history that had allowed the gradual emergence of a free and independent peasantry in the Nordic countries and had curtailed the dominance of the nobility and the subsequent formation of a powerful right wing. Finland's history was harsher than the histories of the other Nordic countries but didn't prevent the country from following their path of social development.

Unemployment benefits in Spain are contributory and non-contributory. They are part of social security system in Spain and are managed by the State Public Employment Service (SEPE). Employers and employees contribute to the unemployment contingency fund and if an unemployed person fulfills certain criteria they can claim an allowance which is based on the time they have contributed and their average wage. A non-contributory benefit is also available to those who no longer receive a contributory benefit dependent on a maximum level of income.

The Social Security Institution is the governing authority of the Turkish social security system. It was established by the Social Security Institution Law No:5502, which was published in the Official Gazette No: 26173 on June 20, 2006. This brought five different retirement systems that affected civil servants, contractual paid workers, agricultural paid workers, and self-employed workers into a single retirement system offering equal actuarial rights and obligations.

Carer's Allowance is a non-contributory benefit in the United Kingdom payable to people who care for a disabled person for at least 35 hours a week. It was first established as Invalid Care Allowance in 1976, and married women were not eligible. This policy was held to be unlawful sexual discrimination by the European Court in 1986 in the case of Jackie Drake. See Carers rights movement In May 2020 around 1.1 million people in England were entitled to Carer’s Allowance, of which 780,000 people were being paid it, according to the National Audit Office.

Invalidity Benefit was a benefit from the United Kingdom's National Insurance scheme that was introduced in 1971 by Edward Heath's government. It was paid to people who had been invalided out of their trade or occupation after sustaining an injury or developing a long-term illness. It was replaced by Incapacity Benefit in 1995.

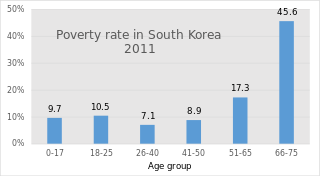

South Korea's pension scheme was introduced relatively recently, compared to other democratic nations. Half of the country's population aged 65 and over lives in relative poverty, or nearly four times the 13% average for member countries of the Organisation for Economic Co-operation and Development (OECD). This makes old age poverty an urgent social problem. Public social spending by general government is half the OECD average, and is the lowest as a percentage of GDP among OECD member countries.

Welfare in Israel refers to the series of social welfare schemes in the Israeli government which are administered by the Ministry of Social Affairs and Social Services, and by Israel's national social security agency, Bituah Leumi. All residents of Israel must pay insurance contributions in order to qualify for welfare.

The Instituto Nacional do Seguro Social or INSS is a Brazilian government agency linked to the Ministry of Labor and Employment that collects contributions for the maintenance of the General Social Security System (RGPS), which is responsible for paying retirement pensions, maternity, death, reclusion, sickness and accident benefits, and other services belonging to the core of Exclusive State Activities, for those who are entitled to these benefits in accordance with the law. The INSS works in conjunction with Dataprev, the technology company that processes all social security data.