Related Research Articles

Balance of trade can be measured in terms of commercial balance, or net exports. Balance of trade is the difference between the monetary value of a nation's exports and imports over a certain time period. Sometimes a distinction is made between a balance of trade for goods versus one for services. The balance of trade measures a flow variable of exports and imports over a given period of time. The notion of the balance of trade does not mean that exports and imports are "in balance" with each other.

In finance, an exchange rate is the rate at which one currency will be exchanged for another currency. Currencies are most commonly national currencies, but may be sub-national as in the case of Hong Kong or supra-national as in the case of the euro.

The global financial system is the worldwide framework of legal agreements, institutions, and both formal and informal economic action that together facilitate international flows of financial capital for purposes of investment and trade financing. Since emerging in the late 19th century during the first modern wave of economic globalization, its evolution is marked by the establishment of central banks, multilateral treaties, and intergovernmental organizations aimed at improving the transparency, regulation, and effectiveness of international markets. In the late 1800s, world migration and communication technology facilitated unprecedented growth in international trade and investment. At the onset of World War I, trade contracted as foreign exchange markets became paralyzed by money market illiquidity. Countries sought to defend against external shocks with protectionist policies and trade virtually halted by 1933, worsening the effects of the global Great Depression until a series of reciprocal trade agreements slowly reduced tariffs worldwide. Efforts to revamp the international monetary system after World War II improved exchange rate stability, fostering record growth in global finance.

In international economics, the balance of payments of a country is the difference between all money flowing into the country in a particular period of time and the outflow of money to the rest of the world. In other words, it is economic transactions between countries during a period of time. These financial transactions are made by individuals, firms and government bodies to compare receipts and payments arising out of trade of goods and services.

In macroeconomics and international finance, a country's current account records the value of exports and imports of both goods and services and international transfers of capital. It is one of the two components of the balance of payments, the other being the capital account. Current account measures the nation's earnings and spendings abroad and it consists of the balance of trade, net primary income or factor income and net unilateral transfers, that have taken place over a given period of time. The current account balance is one of two major measures of a country's foreign trade. A current account surplus indicates that the value of a country's net foreign assets grew over the period in question, and a current account deficit indicates that it shrank. Both government and private payments are included in the calculation. It is called the current account because goods and services are generally consumed in the current period.

The Bretton Woods system of monetary management established the rules for commercial relations among the United States, Canada, Western European countries, and Australia as well as 44 other countries after the 1944 Bretton Woods Agreement. The Bretton Woods system was the first example of a fully negotiated monetary order intended to govern monetary relations among independent states. The Bretton Woods system required countries to guarantee convertibility of their currencies into U.S. dollars to within 1% of fixed parity rates, with the dollar convertible to gold bullion for foreign governments and central banks at US$35 per troy ounce of fine gold. It also envisioned greater cooperation among countries in order to prevent future competitive devaluations, and thus established the International Monetary Fund (IMF) to monitor exchange rates and lend reserve currencies to nations with balance of payments deficits.

In macroeconomics and modern monetary policy, a devaluation is an official lowering of the value of a country's currency within a fixed exchange-rate system, in which a monetary authority formally sets a lower exchange rate of the national currency in relation to a foreign reference currency or currency basket. The opposite of devaluation, a change in the exchange rate making the domestic currency more expensive, is called a revaluation. A monetary authority maintains a fixed value of its currency by being ready to buy or sell foreign currency with the domestic currency at a stated rate; a devaluation is an indication that the monetary authority will buy and sell foreign currency at a lower rate.

Eurodollars are U.S. dollars held in time deposit accounts in banks outside the United States, which are not subject to the legal jurisdiction of the U.S. Federal Reserve. Consequently, such deposits are subject to much less regulation than deposits within the U.S. The term was originally applied to U.S. dollar accounts held in banks situated in Europe, but it expanded over the years to cover US dollar accounts held anywhere outside the U.S. Thus, a U.S. dollar-denominated deposit in Tokyo or Beijing would likewise be deemed a Eurodollar deposit. The offshore locations of the Eurodollar make it exposed to potential country risk and economic risk.

Foreign exchange reserves are cash and other reserve assets such as gold and silver held by a central bank or other monetary authority that are primarily available to balance payments of the country, influence the foreign exchange rate of its currency, and to maintain confidence in financial markets. Reserves are held in one or more reserve currencies, nowadays mostly the United States dollar and to a lesser extent the euro.

Export-oriented industrialization (EOI), sometimes called export substitution industrialization (ESI), export-led industrialization (ELI), or export-led growth, is a trade and economic policy aiming to speed up the industrialization process of a country by exporting goods for which the nation has a comparative advantage. Export-led growth implies opening domestic markets to foreign competition in exchange for market access in other countries.

The history of the United States dollar began with moves by the Founding Fathers of the United States of America to establish a national currency based on the Spanish silver dollar, which had been in use in the North American colonies of the Kingdom of Great Britain for over 100 years prior to the United States Declaration of Independence. The new Congress's Coinage Act of 1792 established the United States dollar as the country's standard unit of money, creating the United States Mint tasked with producing and circulating coinage. Initially defined under a bimetallic standard in terms of a fixed quantity of silver or gold, it formally adopted the gold standard in 1900, and finally eliminated all links to gold in 1971.

Foreign trade of Argentina includes economic activities both within and outside Argentina especially with regards to merchandise exports and imports, as well as trade in services.

In its economic relations, Japan is both a major trading nation and one of the largest international investors in the world. In many respects, international trade is the lifeblood of Japan's economy. Imports and exports totaling the equivalent of nearly US$1.309.2 Trillion in 2017, which meant that Japan was the world's fourth largest trading nation after China, the United States and Germany. Trade was once the primary form of Japan's international economic relationships, but in the 1980s its rapidly rising foreign investments added a new and increasingly important dimension, broadening the horizons of Japanese businesses and giving Japan new world prominence.

The economic history of Brazil covers various economic events and traces the changes in the Brazilian economy over the course of the history of Brazil. Portugal, which first colonized the area in the 16th century, enforced a colonial pact with Brazil, an imperial mercantile policy, which drove development for the subsequent three centuries. Independence was achieved in 1822. Slavery was fully abolished in 1888. Important structural transformations began in the 1930s, when important steps were taken to change Brazil into a modern, industrialized economy.

Monetary hegemony is an economic and political concept in which a single state has decisive influence over the functions of the international monetary system. A monetary hegemon would need:

Soviet foreign trade played only a minor role in the Soviet economy. In 1985, for example, exports and imports each accounted for only 4 percent of the Soviet gross national product. The Soviet Union maintained this low level because it could draw upon a large energy and raw material base, and because it historically had pursued a policy of self-sufficiency. Other foreign economic activity included economic aid programs, which primarily benefited the less developed Council for Mutual Economic Assistance (COMECON) countries of Cuba, Mongolia, and Vietnam.

The Anglo-American Loan Agreement was a loan made to the United Kingdom by the United States on 15 July 1946, enabling its economy after the Second World War to keep afloat. The loan was negotiated by British economist John Maynard Keynes and American diplomat William L. Clayton. Problems arose on the American side, with many in Congress reluctant, and with sharp differences between the treasury and state departments. The loan was for US$3.75 billion at a low 2% interest rate; Canada loaned an additional US$1.9 billion. The British economy in 1947 was hurt by a provision that called for convertibility into dollars of the wartime sterling balances the British had borrowed from India and others, but by 1948, the Marshall Plan included financial support that was not expected to be repaid. The entire loan was paid off in 2006, after it was extended six years.

Michael Hudson is an American economist, Professor of Economics at the University of Missouri–Kansas City and a researcher at the Levy Economics Institute at Bard College, former Wall Street analyst, political consultant, commentator and journalist. He is a contributor to The Hudson Report, a weekly economic and financial news podcast produced by Left Out.

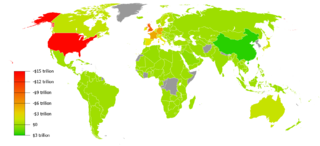

Foreign trade of the United States comprises the international imports and exports of the United States. The country is among the top three global importers and exporters.

Currency war, also known as competitive devaluations, is a condition in international affairs where countries seek to gain a trade advantage over other countries by causing the exchange rate of their currency to fall in relation to other currencies. As the exchange rate of a country's currency falls, exports become more competitive in other countries, and imports into the country become more and more expensive. Both effects benefit the domestic industry, and thus employment, which receives a boost in demand from both domestic and foreign markets. However, the price increases for import goods are unpopular as they harm citizens' purchasing power; and when all countries adopt a similar strategy, it can lead to a general decline in international trade, harming all countries.

References

- ↑ Encyclopedia of Tariffs and Trade in U.S. History. Vol. 1. Cynthia Clark Northrup, Elaine C. Prange Turney. Westport, CT: Greenwood Press. 2003. p. 115. ISBN 978-0-313319-43-3. OCLC 57478673.

{{cite book}}: CS1 maint: others (link)