Theoretical explanations

Loss aversion

The leading explanation for the aforementioned WTP-WTA gap is that of loss aversion. It was first linked by Kahneman and his colleagues that selling an endowment means the loss of the object, and as humans are aligned to be more loss-averse, less utility is obtained from acquirement of the same endowment. [4] They go on to suggest that the endowment effect, when considered as a facet of loss-aversion, would thus violate the Coase theorem, and was described as inconsistent with standard economic theory which asserts that a person's willingness to pay (WTP) for a good should be equal to their willingness to accept (WTA) compensation to be deprived of the good, a hypothesis which underlies consumer theory and indifference curves. Another aspect of loss aversion exhibited within the endowment effect is that opportunity costs are often undervalued. The overcharging of the selling item stems from the fixation of losing the item rather than the unattained gain if the sale falls through. [19]

The correlation between the two theories is so high that the endowment effect is often seen as the presentation of loss aversion in a riskless setting. However, these claims have been disputed and other researchers claim that psychological inertia, [20] differences in reference prices relied on by buyers and sellers, [3] and ownership (attribution of the item to self) and not loss aversion are the key to this phenomenon. [21]

Psychological inertia

David Gal proposed a psychological inertia account of the endowment effect. [22] [23] In this account, sellers require a higher price to part with an object than buyers are willing to pay because neither has a well-defined, precise valuation for the object and therefore there is a range of prices over which neither buyers nor sellers have much incentive to trade. For example, in the case of Kahneman et al.'s (1990) classic mug experiments (where sellers demanded about $7 to part with their mug whereas buyers were only willing to pay, on average, about $3 to acquire a mug) there was likely a range of prices for the mug ($4 to $6) that left the buyers and sellers without much incentive to either acquire or part with it. Buyers and sellers therefore maintained the status quo out of inertia. Conversely, a high price ($7 or more) yielded a meaningful incentive for an owner to part with the mug; likewise, a relatively low price ($3 or less) yielded a meaningful incentive for a buyer to acquire the mug.

Reference-dependent accounts

According to reference-dependent theories, consumers first evaluate the potential change in question as either being a gain or a loss. In line with prospect theory (Tversky and Kahneman, 1979 [24] ), changes that are framed as losses are weighed more heavily than are the changes framed as gains. Thus an individual owning "A" amount of a good, asked how much he/she would be willing to pay to acquire "B", would be willing to pay a value (B-A) that is lower than the value that he/she would be willing to accept to sell (C-A) units; the value function for perceived gains is not as steep as the value function for perceived losses.

Figure 1 presents this explanation in graphical form. An individual at point A, asked how much he/she would be willing to accept (WTA) as compensation to sell X units and move to point C, would demand greater compensation for that loss than he/she would be willing to pay for an equivalent gain of X units to move him/her to point B. Thus the difference between (B-A) and (C-A) would account for the endowment effect. In other words, he/she expects more money while selling; but wants to pay less while buying the same amount of goods.

-

- Figure 1: Prospect Theory and the Endowment Effect

Neoclassical explanations

Hanemann (1991), [25] develops a neoclassical explanation for the endowment effect, accounting for the effect without invoking prospect theory.

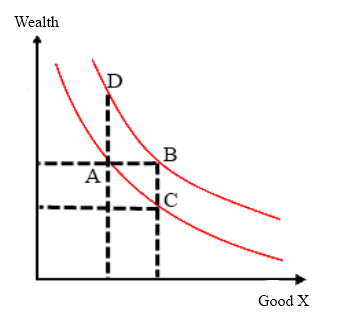

Figure 2 presents this explanation in graphical form. In the figure, two indifference curves for a particular good X and wealth are given. Consider an individual who is given goods X such that they move from point A (where they have X0 of good X) to point B (where they have the same wealth and X1 of good X). Their WTP represented by the vertical distance from B to C, because (after giving up that amount of wealth) the individual is indifferent about being at A or C. Now consider an individual who gives up goods such that they move from B to A. Their WTA represented by the (larger) vertical distance from A to D because (after receiving that much wealth) they are indifferent about either being at point B or D. Shogren et al. (1994) [26] has reported findings that lend support to Hanemann's hypothesis. However, Kahneman, Knetsch, and Thaler (1991) [6] find that the endowment effect continues even when wealth effects are fully controlled for.

-

- Figure 2: Hanemann's Endowment Effect Explanation

When goods are indivisible, a coalitional game can be set up so that a utility function can be defined on all subsets of the goods. Hu (2020) [27] shows the endowment effect when the utility function is superadditive, i.e., the value of the whole is greater than the sum of its parts. Hu (2020) also introduces a few unbiased solutions which mitigate endowment bias.

Experiments in cognitive psychology have demonstrated that the endowment effect can be brought about by asymmetries in cognitive processing in judging owned and not-owned goods. A 2007 fMRI study by Knutson et al. demonstrated that the insula, an area of the brain associated with loss aversion, is stimulated when people ponder relinquishing goods they already possess. This is consistent with the hypothesis that the endowment effect entails not only ownership bias but also emotional attachment and loss anticipation neural processes. Further, the effect is also conditioned by cultural environment and personality difference in risk sensitivity. [28]

Connection-based, or "psychological ownership" theories

Connection-based theories propose that the attachment or association with the self-induced by owning a good is responsible for the endowment effect (for a review, see Morewedge & Giblin, 2015 [2] ). Work by Morewedge, Shu, Gilbert and Wilson (2009) [21] provides support for these theories, as does work by Maddux et al. (2010). [29] For example, research participants who were given one mug and asked how much they would pay for a second mug ("owner-buyers") were WTP as much as "owners-sellers," another group of participants who were given a mug and asked how much they were WTA to sell it (both groups valued the mug in question more than buyers who were not given a mug). [21] Others have argued that the short duration of ownership or highly prosaic items typically used in endowment effect type studies is not sufficient to produce such a connection, conducting research demonstrating support for those points (e.g. Liersch & Rottenstreich, Working Paper).

Two paths by which attachment or self-associations increase the value of a good have been proposed (Morewedge & Giblin, 2015). [2] An attachment theory suggests that ownership creates a non-transferable balanced association between the self and the good. The good is incorporated into the self-concept of the owner, becoming part of her identity and imbuing it with attributes related to her self-concept. Self-associations may take the form of an emotional attachment to the good. Once an attachment has formed, the potential loss of the good is perceived as a threat to the self. [7] A real-world example of this would be an individual refusing to part with a college T-shirt because it supports one's identity as an alumnus of that university. A second route by which ownership may increase value is through a self-referential memory effect (SRE) – the better encoding and recollection of stimuli associated with the self-concept. [30] People have a better memory for goods they own than goods they do not own. The self-referential memory effect for owned goods may act thus as an endogenous framing effect. During a transaction, attributes of a good may be more accessible to its owners than are other attributes of the transaction. Because most goods have more positive than negative features, this accessibility bias should result in owners more positively evaluating their goods than do non-owners. [2]

Greater sensitivity to market demands for sellers

Sellers may dictate a price based on the desires of multiple potential buyers, whereas buyers may consider their own taste. This can lead to differences between buying and selling prices because the market price is typically higher than one's idiosyncratic price estimate. According to this account, the endowment effect can be viewed as under-pricing for buyers compared to the market price; or over-pricing for sellers compared to their individual taste. Two recent lines of study support this argument. Weaver and Frederick (2012) [3] presented their participants with retail prices of products, and then asked them to specify either their buying or selling price for these products. The results revealed that sellers' valuations were closer to the known retail prices than those of buyers. A second line of studies is a meta-analysis of buying and selling of lotteries. [31] A review of over 30 empirical studies showed that selling prices were closer to the lottery's expected value, which is the normative price of the lottery: hence the endowment effect was consistent with buyers' tendency to under-price lotteries as compared to the normative price. One possible reason for this tendency of buyers to indicate lower prices is their risk aversion. By contrast, sellers may assume that the market is heterogeneous enough to include buyers with potential risk neutrality and therefore adjust their price closer to a risk neutral expected value.

Biased information processing theories

Several cognitive accounts of the endowment effect suggest that it is induced by the way endowment status changes the search for, attention to, recollection of, and weighting of information regarding the transaction. Frames evoked by acquisition of a good (e.g., buying, choosing it rather than another good) may increase the cognitive accessibility of information favoring the decision to keep one's money and not acquire the good. By contrast, frames evoked by disposition of the good (e.g., selling) may increase the cognitive accessibility of information favoring the decision to keep the good rather than trade or dispose of it for money (for a review, see Morewedge & Giblin, 2015). [2] For example, Johnson and colleagues (2007) [32] found that prospective mug buyers tended to recall reasons to keep their money before recalling reasons to buy the mug, whereas sellers tended to recall reasons to keep their mug before reasons to sell it for money.

Evolutionary arguments

Huck, Kirchsteiger & Oechssler (2005) [33] have raised the hypothesis that natural selection may favor individuals whose preferences embody an endowment effect given that it may improve one's bargaining position in bilateral trades. Thus in a small tribal society with a few alternative sellers (i.e. where the buyer may not have the option of moving to an alternative seller), having a predisposition towards embodying the endowment effect may be evolutionarily beneficial. This may be linked with findings (Shogren, et al., 1994 [26] ) that suggest the endowment effect is less strong when the relatively artificial sense of scarcity induced in experimental settings is lessened. Countervailing evidence for an evolutionary account is provided by studies showing that the endowment effect is moderated by exposure to modern exchange markets (e.g., hunter gatherer tribes with market exposure are more likely to exhibit the endowment effect than tribes that do not), [34] and that the endowment effect is moderated by culture (Maddux et al., 2010 [29] ).