Flow of funds accounts are a system of interrelated balance sheets for a nation, calculated periodically. There are two types of balance sheets: those showing

The aggregate assets and liabilities for financial and nonfinancial sectors, and

What sectors issue and hold financial assets (instruments) of a given type.

The sectors and instruments are listed below.

These balance sheets measure levels of assets and liabilities. From each balance sheet a corresponding flows statement can be derived by subtracting the levels data for the preceding period from the data for the current period. (In the statistical analysis of time series, this operation is known as "first differencing.") The change in a level item between two adjacent periods is known as a "fund flow"; hence the name for these accounts.

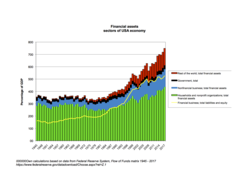

Financial assets of broad sectors of USA economy, 1945–2017. Source: Federal Reserve System, flow of funds data.Liabilities of broad sectors of USA economy, 1945–2017. Source: Federal Reserve System, flow of funds data.Financial net worth of broad sectors of USA economy, 1945–2017. Source: Federal Reserve System, flow of funds data.

Main topics covered in the FF accounts

Total debt broken down by issuer and holder

Connection to national accounts, and derivation of measures of aggregate saving

Fund flows originating in each sector

Levels:

Assets and liabilities for broad sectors and for specific financial sectors

Sectors issuing and holding instruments of a given class

Miscellaneous aggregate financial data

Organization of the flow of funds accounts of the US

The flow of funds (FOF) accounts of the United States are prepared by the Flow of Funds section of the Board of Governors of the Federal Reserve System and are published quarterly in a publication called the Z.1 Statistical Release. Current and historical releases available in PDF, CSV, or XML format. Data frequency is annual from yearend 1945 and quarterly beginning in 1952Q1. Detailed interactive documentation is also available.

The flow of funds accounts follow naturally from double-entry bookkeeping; every financial asset is also a liability of some domestic or foreign human entity. A fundamental fact about any economic sector is its balance sheet, a breakdown of its physical and financial assets, and of its liabilities. The only physical assets noted in the FF accounts are those of private nonfinancial sectors.

Organisation of the flow of funds accounts of the UK

The UK flow of funds accounts are prepared by the Office for National Statistics in a series of matrices. The first tables will be published in Blue Book 2014, to be released in September 2014. They contain the sectors and instruments shown below:

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.