Related Research Articles

In finance, a derivative is a contract that derives its value from the performance of an underlying entity. This underlying entity can be an asset, index, or interest rate, and is often simply called the underlying. Derivatives can be used for a number of purposes, including insuring against price movements (hedging), increasing exposure to price movements for speculation, or getting access to otherwise hard-to-trade assets or markets.

A commodity market is a market that trades in the primary economic sector rather than manufactured products, such as cocoa, fruit and sugar. Hard commodities are mined, such as gold and oil. Futures contracts are the oldest way of investing in commodities. Commodity markets can include physical trading and derivatives trading using spot prices, forwards, futures, and options on futures. Farmers have used a simple form of derivative trading in the commodity market for centuries for price risk management.

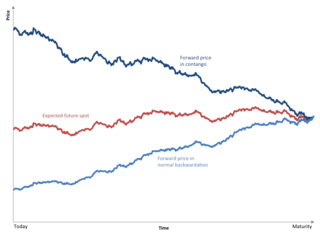

Contango is a situation where the futures price of a commodity is higher than the expected spot price of the contract at maturity. In a contango situation, arbitrageurs or speculators are "willing to pay more [now] for a commodity [to be received] at some point in the future than the actual expected price of the commodity [at that future point]. This may be due to people's desire to pay a premium to have the commodity in the future rather than paying the costs of storage and carry costs of buying the commodity today." On the other side of the trade, hedgers are happy to sell futures contracts and accept the higher-than-expected returns. A contango market is also known as a normal market, or carrying-cost market.

In finance, speculation is the purchase of an asset with the hope that it will become more valuable shortly. It can also refer to short sales in which the speculator hopes for a decline in value.

In finance, a futures contract is a standardized legal contract to buy or sell something at a predetermined price for delivery at a specified time in the future, between parties not yet known to each other. The asset transacted is usually a commodity or financial instrument. The predetermined price of the contract is known as the forward price or delivery price. The specified time in the future when delivery and payment occur is known as the delivery date. Because it derives its value from the value of the underlying asset, a futures contract is a derivative.

A hedge is an investment position intended to offset potential losses or gains that may be incurred by a companion investment. A hedge can be constructed from many types of financial instruments, including stocks, exchange-traded funds, insurance, forward contracts, swaps, options, gambles, many types of over-the-counter and derivative products, and futures contracts.

The foreign exchange market is a global decentralized or over-the-counter (OTC) market for the trading of currencies. This market determines foreign exchange rates for every currency. It includes all aspects of buying, selling and exchanging currencies at current or determined prices. In terms of trading volume, it is by far the largest market in the world, followed by the credit market.

An interest rate future is a financial derivative with an interest-bearing instrument as the underlying asset. It is a particular type of interest rate derivative.

In finance, a contract for difference (CFD) is a legally binding agreement that creates, defines, and governs mutual rights and obligations between two parties, typically described as "buyer" and "seller", stipulating that the buyer will pay to the seller the difference between the current value of an asset and its value at contract time. If the closing trade price is higher than the opening price, then the seller will pay the buyer the difference, and that will be the buyer's profit. The opposite is also true. That is, if the current asset price is lower at the exit price than the value at the contract's opening, then the seller, rather than the buyer, will benefit from the difference.

In finance, an asset class is a group of financial instruments that have similar financial characteristics and behave similarly in the marketplace. We can often break these instruments into those having to do with real assets and those having to do with financial assets. Often, assets within the same asset class are subject to the same laws and regulations; however, this is not always true. For instance, futures on an asset are often considered part of the same asset class as the underlying instrument but are subject to different regulations than the underlying instrument.

The Dalian Commodity Exchange (DCE) is a Chinese futures exchange based in Dalian, Liaoning province, China. It is a non-profit, self-regulating and membership legal entity established on February 28, 1993.

The price of oil, or the oil price, generally refers to the spot price of a barrel of benchmark crude oil—a reference price for buyers and sellers of crude oil such as West Texas Intermediate (WTI), Brent Crude, Dubai Crude, OPEC Reference Basket, Tapis crude, Bonny Light, Urals oil, Isthmus, and Western Canadian Select (WCS). Oil prices are determined by global supply and demand, rather than any country's domestic production level.

There are two basic financial market participant distinctions, investors versus speculators and institutional versus retail. Action in financial markets by central banks is usually regarded as intervention rather than participation.

The world food price crisis refers to a period of time when the cost of food increased significantly and had a profound impact on the availability and affordability of food for people around the world. This crisis is often characterized by sharp spikes in the prices of key staple foods such as wheat, rice, and corn, as well as other agricultural commodities such as sugar and oil. The causes of the world food price crisis are complex and multifaceted, but they generally involve a combination of factors including droughts and other weather-related events, increased demand for biofuels, trade policies, and financial speculation. The consequences of the world food price crisis can be severe, particularly for people in low-income countries who spend a large portion of their income on food. According to IMF if prices eventually rise again, there will likely be sizeable differences between countries. Due to various factors, it is probable that the effect would be felt most by consumers in emerging markets and developing economies still wrestling with the effects of the pandemic.

Agflation is an economic phenomenon of an advanced increase in the price for food and for industrial agricultural crops when compared with the general rise in prices or with the rise in prices in the non-agricultural sector. The term was increasingly used in the analytical reports, for example, by the investment banks Merrill Lynch in early 2007 and Goldman Sachs in early 2008. They used the term to denote a sharp rise in prices for agricultural products, or, more precisely, a rapid increase in food prices against the background of a decrease in its reserves, a relatively low general inflation rate, and insignificant growth in the level of wages. Agflation has become an increasingly important issue for many governments. From time to time agflation may become so severe that the World Food Programme has described the phenomenon as a "silent tsunami". Agflation endangers food security, particularly for developing countries, and can cause social unrest.

Weather risk management is a type of risk management done by organizations to address potential financial losses caused by unusual weather.

A commodity index fund is a fund whose assets are invested in financial instruments based on or linked to a commodity price index. In just about every case the index is in fact a commodity futures index.

A commodity trading advisor (CTA) is US financial regulatory term for an individual or organization who is retained by a fund or individual client to provide advice and services related to trading in futures contracts, commodity options and/or swaps. They are responsible for the trading within managed futures accounts. The definition of CTA may also apply to investment advisors for hedge funds and private funds including mutual funds and exchange-traded funds in certain cases. CTAs are generally regulated by the United States federal government through registration with the Commodity Futures Trading Commission (CFTC) and membership of the National Futures Association (NFA).

Food prices refer to the average price level for food across countries, regions and on a global scale. Food prices affect producers and consumers of food.

Securities market participants in the United States include corporations and governments issuing securities, persons and corporations buying and selling a security, the broker-dealers and exchanges which facilitate such trading, banks which safe keep assets, and regulators who monitor the markets' activities. Investors buy and sell through broker-dealers and have their assets retained by either their executing broker-dealer, a custodian bank or a prime broker. These transactions take place in the environment of equity and equity options exchanges, regulated by the U.S. Securities and Exchange Commission (SEC), or derivative exchanges, regulated by the Commodity Futures Trading Commission (CFTC). For transactions involving stocks and bonds, transfer agents assure that the ownership in each transaction is properly assigned to and held on behalf of each investor.

References

- ↑ Gunther Capelle-Blancard,Dramane Coulibaly (2011). "Index trading and agricultural commodity prices: A panel Granger causality analysis". Économie Internationale. 2–3 (126): 51–72.

- ↑ Smith, Adam (1977) [1776]. An Inquiry into the Nature and Causes of the Wealth of Nations. University of Chicago Press. ISBN 0-226-76374-9.

- ↑ "Food speculation". Global Justice Now . 2014-12-09. Retrieved 2019-08-21.

- 1 2 Vidal, John (2011-01-23). "Food speculation: aFood speculation: 'People die from hunger while banks make a killing on food'". the Guardian. Retrieved 2019-08-21.

- ↑ Islam, M. Shahidul. "Of Agflation and Agriculture: Time to Fix the Structural Problems" (PDF). National University of Singapore . Retrieved 23 June 2021.

- ↑ Anna Chadwick (2015). Food Commodity Speculation, Hunger, and the Global Food Crisis: Whither Regulation (Thesis). London School of Economics and Political Science. S2CID 155654460.

- ↑ GHOSH, JAYATI (2010). "The Unnatural Coupling: Food and Global Finance". Journal of Agrarian Change. Wiley. 10 (1): 72–86. Bibcode:2010JAgrC..10...72G. doi:10.1111/j.1471-0366.2009.00249.x. ISSN 1471-0358.

- 1 2 3 4 5 6 7 "The real hunger games: How banks gamble on food prices – and the poor lose out". The Independent. Archived from the original on April 3, 2012. Retrieved April 1, 2012.