In economics, the isoelastic function for utility, also known as the isoelastic utility function, or power utility function, is used to express utility in terms of consumption or some other economic variable that a decision-maker is concerned with. The isoelastic utility function is a special case of hyperbolic absolute risk aversion and at the same time is the only class of utility functions with constant relative risk aversion, which is why it is also called the CRRA (constant relative risk aversion) utility function. In statistics, the same function is called the Box-Cox transformation.

Contents

It is

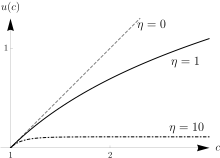

where is consumption, the associated utility, and is a constant that is positive for risk averse agents. [1] Since additive constant terms in objective functions do not affect optimal decisions, the –1 is sometimes omitted in the numerator (although it should be kept if one wishes to preserve mathematical consistency with the limiting case of ; see Special cases below). Since the family contains both power functions and the logarithmic function, it is sometimes called power-log utility. [2]

When the context involves risk, the utility function is viewed as a von Neumann–Morgenstern utility function, and the parameter is the degree of relative risk aversion.

The isoelastic utility function is a special case of the hyperbolic absolute risk aversion (HARA) utility functions, and is used in analyses that either include or do not include underlying risk.