A transaction account, also called a checking account, chequing account, current account, demand deposit account, or share draft account at credit unions, is a deposit account held at a bank or other financial institution. It is available to the account owner "on demand" and is available for frequent and immediate access by the account owner or to others as the account owner may direct. Access may be in a variety of ways, such as cash withdrawals, use of debit cards, cheques (checks) and electronic transfer. In economic terms, the funds held in a transaction account are regarded as liquid funds. In accounting terms, they are considered as cash.

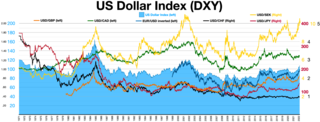

The foreign exchange market is a global decentralized or over-the-counter (OTC) market for the trading of currencies. This market determines foreign exchange rates for every currency. It includes all aspects of buying, selling and exchanging currencies at current or determined prices. In terms of trading volume, it is by far the largest market in the world, followed by the credit market.

A giro transfer, often shortened to giro, is a payment transfer from one bank account to another bank account and initiated by the payer, not the payee. The debit card has a similar model. Giros are primarily used in Europe; although electronic payment systems exist in the United States, it is not possible to perform third-party transfers with them. In the European Union, there is the Single Euro Payments Area (SEPA), which allows electronic giro or debit card payments in euros to be executed to any euro bank account in the area.

The Australian financial system consists of the arrangements covering the borrowing and lending of funds and the transfer of ownership of financial claims in Australia, comprising:

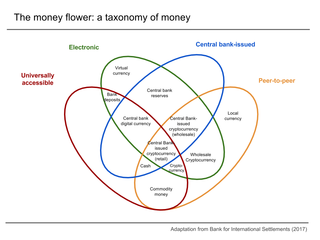

Digital currency is any currency, money, or money-like asset that is primarily managed, stored or exchanged on digital computer systems, especially over the internet. Types of digital currencies include cryptocurrency, virtual currency and central bank digital currency. Digital currency may be recorded on a distributed database on the internet, a centralized electronic computer database owned by a company or bank, within digital files or even on a stored-value card.

A cheque, or check, is a document that orders a bank to pay a specific amount of money from a person's account to the person in whose name the cheque has been issued. The person writing the cheque, known as the drawer, has a transaction banking account where the money is held. The drawer writes various details including the monetary amount, date, and a payee on the cheque, and signs it, ordering their bank, known as the drawee, to pay the amount of money stated to the payee.

Bacs Payment Schemes Limited (Bacs), previously known as Bankers' Automated Clearing System, is responsible for the clearing and settlement of UK automated direct debit and Bacs Direct Credit and the provision of third-party services. Bacs became a subsidiary of Pay.UK on 1 May 2018, and responsibility for direct debit, Bacs Direct Credit, the Current Account Switch Service, Cash ISA Transfer Service and the Industry Sort Code Directory was given to Pay.UK.

A payment system is any system used to settle financial transactions through the transfer of monetary value. This includes the institutions, instruments, people, rules, procedures, standards, and technologies that make its exchange possible. A common type of payment system, called an operational network, links bank accounts and provides for monetary exchange using bank deposits. Some payment systems also include credit mechanisms, which are essentially a different aspect of payment.

A direct debit or direct withdrawal is a financial transaction in which one organisation withdraws funds from a payer's bank account. Formally, the organisation that calls for the funds instructs their bank to collect an amount directly from another's bank account designated by the payer and pay those funds into a bank account designated by the payee. Before the payer's banker will allow the transaction to take place, the payer must have advised the bank that they have authorized the payee to directly draw the funds. It is also called pre-authorized debit (PAD) or pre-authorized payment (PAP). After the authorities are set up, the direct debit transactions are usually processed electronically.

A payment is the voluntary tender of money or its equivalent or of things of value by one party to another in exchange for goods or services provided by them or to fulfill a legal obligation. The party making the payment is commonly called the payer, while the payee is the party receiving the payment.

The Central Bank of Iran (CBI), also known as Bank Markazi, officially the Central Bank of the Islamic Republic of Iran is the central bank of Iran.

A correspondent account is an account established by a banking institution to receive deposits from, make payments on behalf of, or handle other financial transactions for another financial institution. Correspondent accounts are established through bilateral agreements between the two banks.

The Asian Clearing Union (ACU) was established on December 9, 1974, at the initiative of the United Nations Economic and Social Commission for Asia and the Pacific (ESCAP). The primary objective of ACU, at the time of its establishment, was to secure regional co-operation regarding the clearing of eligible monetary transactions among the members of the Union to provide a system for clearing payments among the member countries on a multilateral basis.

Payment and Settlement Systems in India are used for financial transactions. They are covered by the Payment and Settlement Systems Act of 2007, legislated in December 2007 and regulated by the Reserve Bank of India and the Board for Regulation and Supervision of Payment and Settlement Systems.

The Central Bank of Kosovo is the central bank of Kosovo. It was founded in June 2008, the same year Kosovo declared its independence from Serbia, with the approval of Law No. 03/L-074 on the Central Bank of the Republic of Kosovo by the Kosovo Assembly. Before being established as the Central Bank of Kosovo, it operated as the Central Banking Authority of Kosovo. The official currency in Kosovo is the euro, which has been adopted unilaterally in 2002; however, Kosovo is not a member of the Eurozone. The headquarters of the CBK are located in the capital of Kosovo, Pristina.

A bank is a financial institution that accepts deposits from the public and creates a demand deposit while simultaneously making loans. Lending activities can be directly performed by the bank or indirectly through capital markets.

A foreign portfolio investment is a grouping of assets such as stocks, bonds, and cash equivalents. Portfolio investments are held directly by an investor or managed by financial professionals. In economics, foreign portfolio investment is the entry of funds into a country where foreigners deposit money in a country's bank or make purchases in the country's stock and bond markets, sometimes for speculation.

A non-bank foreign exchange company also known as foreign exchange broker or simply forex broker is a company that offers currency exchange and international payments to private individuals and companies. The term is typically used for currency exchange companies that offer physical delivery rather than speculative trading. i.e. there is a physical delivery of currency to a bank account.

A deposit account is a bank account maintained by a financial institution in which a customer can deposit and withdraw money. Deposit accounts can be savings accounts, current accounts or any of several other types of accounts explained below.

CLS Group, or simply CLS, is a specialized financial infrastructure group whose main entity is the New York-based CLS Bank. It started operations in 2002 and operates a unique global multicurrency cash settlement system, known as the CLS System, which plays a critical role in the foreign exchange market. Although the forex market is decentralised and has no central exchange or clearing facility, firms that chose to use CLS to settle their FX transactions can mitigate the settlement risk associated with their trades.