Westdeutsche Landesbank was a major German bank based in Düsseldorf, mainly controlled by the German state of North Rhine-Westphalia. It was created in 1969 by the merger of two predecessor entities respectively for the Rhineland and Westphalia. As a Landesbank, WestLB's core business was wholesale banking on behalf of the region's Sparkassen, but it expanded into numerous risky activities that ultimately led to its restructuring and dismantlement in the late 2000s. As of 30 June 2012, the residual operations of WestLB were transferred to a legacy non-bank entity, Portigon Financial Services AG.

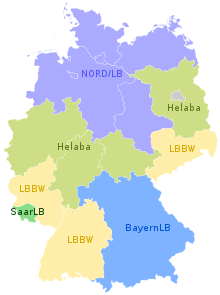

Helaba, short for Landesbank Hessen-Thüringen, is a commercial bank with core regions in Hesse and Thuringia, Germany offering financial services to companies, banks, institutional investors and the public sector, both within Germany and internationally. At the same time, it is the central clearing institution and service provider for 40 percent of German savings banks. Helaba is an institution incorporated under public law. With approximately 6,300 employees and two headquarters in Frankfurt and Erfurt, the bank maintains branches in Düsseldorf and Kassel as well as offices in Berlin, Stuttgart, Munich and Muenster. On an international level, Helaba acts through branches and representative offices in Paris, London, New York, Madrid, Moscow, Shanghai, and Singapore. Frankfurter Sparkasse, the leading retail bank in the Rhine-Main region, is a wholly owned subsidiary of Helaba. The Helaba Group also comprises the online bank 1822direkt, LBS Hessen-Thüringen and WIBank. The latter implements development programmes of the State of Hesse. Further Helaba subsidiaries are Helaba Invest Kapitalanlagegesellschaft, Frankfurter Bankgesellschaft and the OFB Group.

Bayerische Landesbank, also known as BayernLB, is a publicly regulated bank based in Munich, Germany and one of the six Landesbanken. It is 75% owned by the Free State of Bavaria and 25% owned by the Sparkassenverband Bayern, the umbrella organization of Bavarian Sparkassen. With a balance of €285,70 billion and 7,703 employees, it is the seventh-largest financial institution in Germany.

Landesbank Berlin Holding is a large commercial bank based in Berlin, Germany. It is the holding company of the Berliner Sparkasse and Landesbank. In 2007, LBB was taken over by the Deutscher Sparkassen- und Giroverband (DSGV). Berlin was forced to sell its stake by the European Commission as a condition of permitting the bailout of the then Bankgesellschaft Berlin, which had gotten into difficulties due to a real-estate scandal. In 2010, a net profit of EUR 317 million was reported.

The Norddeutsche Landesbank Girozentrale is a German Landesbank and one of the largest commercial banks in Germany. It is a public corporation majority-owned by the federal states of Lower Saxony and Saxony-Anhalt with its head office in Hanover and branches in Braunschweig and Magdeburg. Regional Sparkassen hold a minority stake of 35 percent.

The Association of German Public Banks is a leading association within the German banking sector, bringing together most of the German public banking sector except the local-level savings banks. Its membership includes 63 banks, including the Landesbanks that are also members of the Deutscher Sparkassen- und Giroverband (DSGV) and form part of the Sparkassen-Finanzgruppe, and promotional and development banks owned by the Federal Republic of Germany or the individual German federal states.

In German-speaking jurisdictions, Landesbank, lit. 'bank of the Land', generally refers to a bank operating within a territorial subdivision that has autonomy but not full sovereignty. It is occasionally translated as "provincial bank".

The Deutscher Sparkassen- und Giroverband is the association of German savings banks and the apex entity of the Sparkassen-Finanzgruppe, the European Union's second-largest financial services group with 2.4 trillion euros combined assets as of end-2021. Germany's savings banks, owned by local governments, play a major role in the country's economy, together operating some 15,860 branches and employing about 284,800 people.

Georg Fahrenschon is a German politician of the Christian Social Union (CSU). From 2008 to 2011, he served as finance minister in the Bavarian State Ministry of Finance. He was a member of the Bundestag of Germany until 2007.

DekaBank Deutsche Girozentrale is the central provider of asset management and capital market solutions of the Sparkassen-Finanzgruppe, a network of public banks that together form the largest financial services group in Germany and in all of Europe. It is registered in both Frankfurt and Berlin, with main operational headquarters in Frankfurt. It traces its origins to the Deutsche Girozentrale, established in 1918 as a hub for payments within the German savings banks system.

The German Cooperative Financial Group is a major cooperative banking network in Germany that includes local banks named Volksbanken and Raiffeisenbanken, the latter in tribute to 19th-century cooperative movement pioneer Friedrich Wilhelm Raiffeisen. The Cooperative Group represents one of the three "pillars" of Germany's banking sector, the other two being, respectively, the Sparkassen-Finanzgruppe of public banks, and the commercial banking sector represented by the Association of German Banks.

The Stadt- und Kreissparkasse Leipzig is a Sparkasse, a public savings bank, based in Leipzig, Saxony. It is one of the largest financial institutions in the new German Länder.

Hamburger Sparkasse AG (Haspa) is one of 5 free public savings banks in Germany based in Hamburg. With a balance sheet total of around 41.9 billion euros and about 5,000 employees, it is the largest savings bank in Germany. It was founded in 1827 in the legal form of the old Hamburg law. In 2003 the bank was separated to a stock corporation and the original Hamburger Sparkasse changed its name to Haspa Finanzholding.

The Sparkasse Mittelholstein AG, based in Rendsburg, is one of five free public savings banks existing in Germany.

As a transaction bank, the Deutsche WertpapierService Bank AG (dwpbank) handles the securities processing for financial institutions from the savings bank and cooperative sector, but also from the private and commercial banking sector in Germany. dwpbank currently manages around 5.34 million securities accounts.

The Berlin Hyp AG, based in Berlin, is one of the large German real estate and mortgage banks. The bank was created in 1996 from the merger of Berliner Hypotheken- und Pfandbriefbank AG and Braunschweig-Hannoversche Hypothekenbank AG.

The German public banking sector represents a significant share of the broader banking sector in Germany. Unlike in most other Western and Central European countries, German public-sector banks have been present since the early phases of formalization of banking entities in the early modern period and have never lost their collective significance. They are typically referred to as one of the three “pillars” of the German banking system, the other two pillars being the cooperative banks and commercial banks.

The Sparkassengruppe Österreich brings together all savings banks in Austria. Tracing its origins to 1819, it serves around 4 million customers in 797 branches with more than 15,500 employees, with a customer share in Austria around 31.2% as of December 2022. The group has a complex decentralized structure but relies critically on Erste Group Bank AG, which owns the main local savings bank in Vienna, operates central functions, owns and manages subsidiaries outside of Austria, and consolidates group accounts. The Österreichischer Sparkassenverband acts as the group's national representative body.

The Österreichischer Sparkassenverband (ÖSPV) is the national representative body of the Sparkassengruppe Österreich, acting as a trade association.