HM Customs and Excise was a department of the British Government formed in 1909 by the merger of HM Customs and HM Excise; its primary responsibility was the collection of customs duties, excise duties, and other indirect taxes.

HM Revenue and Customs is a non-ministerial department of the UK Government responsible for the collection of taxes, the payment of some forms of state support, the administration of other regulatory regimes including the national minimum wage and the issuance of national insurance numbers. HMRC was formed by the merger of the Inland Revenue and HM Customs and Excise, which took effect on 18 April 2005. The department's logo is the St Edward's Crown enclosed within a circle.

Vehicle Excise Duty is an annual tax that is levied as an excise duty and which must be paid for most types of powered vehicles which are to be used on public roads in the United Kingdom. Registered vehicles that are not being used or parked on public roads and which have been taxed since 31 January 1998, must be covered by a Statutory Off Road Notification (SORN) to avoid VED. In 2016, VED generated approximately £6 billion for the Exchequer.

Taxation in the United Kingdom may involve payments to at least three different levels of government: central government, devolved governments and local government. Central government revenues come primarily from income tax, National Insurance contributions, value added tax, corporation tax and fuel duty. Local government revenues come primarily from grants from central government funds, business rates in England, Council Tax and increasingly from fees and charges such as those for on-street parking. In the fiscal year 2014–15, total government revenue was forecast to be £648 billion, or 37.7 per cent of GDP, with net taxes and National Insurance contributions standing at £606 billion.

A Finance Act is the headline fiscal (budgetary) legislation enacted by the UK Parliament, containing multiple provisions as to taxes, duties, exemptions and reliefs at least once per year, and in particular setting out the principal tax rates for each fiscal year.

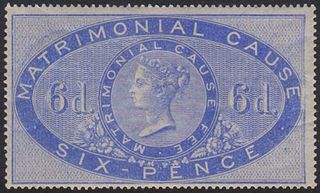

Stamp duty in the United Kingdom is a form of tax charged on legal instruments, and historically required a physical stamp to be attached to or impressed upon the document in question. The more modern versions of the tax no longer require a physical stamp.

The Revenue and Customs Prosecution Office (RCPO) was a non-departmental public body created under the Commissioners for Revenue and Customs Act 2005 as an independent prosecution body to take responsibility in the England, Wales and Northern Ireland for the prosecution of criminal offences in cases previously within the purview of the Inland Revenue and HM Customs and Excise (HMCE). In Scotland it was a Specialist Reporting Agency and the cases are then prosecuted by the Crown Office and Procurator Fiscal Service. It was merged with the Crown Prosecution Service on 1 January 2010.

The history of the English fiscal system affords the best known example of continuous financial development in terms of both institutions and methods. Although periods of great upheaval occurred from the time of the Norman Conquest to the beginning of the 20th century, the line of connection is almost entirely unbroken. Perhaps, the most revolutionary changes occurred in the 17th century as a result of the Civil War and, later, the Glorious Revolution of 1688; though even then there was no real breach of continuity.

HM Customs was the national Customs service of England until a merger with the Department of Excise in 1909. The phrase 'HM Customs', in use since the Middle Ages, referred both to the customs dues themselves and to the office of state established for their collection, assessment and administration.

Motoring taxation in the United Kingdom consists primarily of vehicle excise duty, which is levied on vehicles registered in the UK, and hydrocarbon oil duty, which is levied on the fuel used by motor vehicles. VED and fuel tax raised approximately £32 billion in 2009, a further £4 billion was raised from the value added tax on fuel purchases. Motoring-related taxes for fiscal year 2011/12, including fuel duties and VED, are estimated that will amount to more than £38 billion, representing almost 7% of total UK taxation.

His or Her Majesty's Excise refers to 'inland' duties levied on articles at the time of their manufacture. Excise duty was first raised in England in 1643. Like HM Customs, the Excise was administered by a Board of Commissioners who were accountable to the Lords Commissioners of the Treasury. While 'HM Revenue of Excise' was a phrase used in early legislation to refer to this form of duty, the body tasked with its collection and general administration was usually known as the Excise Office.

An excise, or excise tax, is any duty on manufactured goods that is normally levied at the moment of manufacture for internal consumption rather than at sale. Excises are often associated with customs duties, which are levied on pre-existing goods when they cross a designated border in a specific direction; customs are levied on goods that become taxable items at the border, while excise is levied on goods that came into existence inland.

The Inland Revenue Authority of Singapore (IRAS) is a statutory board under the Ministry of Finance of the Government of Singapore in charge of tax collection.

An important biofuel in the United Kingdom is biojet.

The Royal Malaysian Customs Department is a government department body under the Malaysian Ministry of Finance. RMCD functions as the country's main indirect tax collector, facilitating trade and enforcing laws. The top management of JKDM is led by the Director General of Customs and assisted by 3 deputies, namely, the Deputy Director General of Customs Enforcement/Compliance Division, the Deputy Director General of Customs Customs/Inland Tax Division and the Deputy Chief Director of Customs Management Division. The Royal Malaysian Customs Department consists of several divisions, namely the Enforcement Division, the Inland Tax Division, the Compliance Division, the Customs Division, and the Technical Services Division.

The history of taxation in the United Kingdom includes the history of all collections by governments under law, in money or in kind, including collections by monarchs and lesser feudal lords, levied on persons or property subject to the government, with the primary purpose of raising revenue.

The Board of Inland Revenue Stamping Department Archive in the British Library contains artefacts from 1710 onwards, and has come into existence through amendments in United Kingdom legislation.

Revenue stamps of the United Kingdom refer to the various revenue or fiscal stamps, whether adhesive, directly embossed or otherwise, which were issued by and used in the Kingdom of England, the Kingdom of Great Britain, the United Kingdom of Great Britain and Ireland and the United Kingdom of Great Britain and Northern Ireland, from the late 17th century to the present day.

Taxation in Malta is levied by the State and it is administered by the Commissioner for Revenue. The total tax revenues in 2014 amounted to €2.747 Billion, which represents 34.6% of the Maltese GDP. The main sources of tax revenue were value-added tax, income tax, and social security contributions.