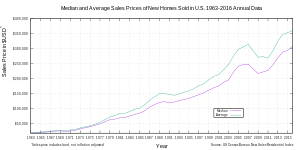

Housing prices peaked in early 2005, began declining in 2006 (see also United States housing market correction).

Housing prices peaked in early 2005, began declining in 2006 (see also United States housing market correction).

Year-to-year decreases in both U.S. home sales and home prices accelerates rather than slowing, with U.S. Treasury secretary Paulson calling "the housing decline ... the most significant risk to our economy." [54] Home sales continue to fall. The decrease in existing-home sales is the steepest since 1989. In Q1/2007, S&P/Case-Shiller house price index records first year-over-year decline in nationwide house prices since 1991. [55] The subprime mortgage industry collapses, foreclosure activity increases [56] and rising interest rates threaten to depress prices further as problems in the subprime markets spread to the near-prime and prime mortgage markets. [57]

Home sales continue to fall. Fears of a U.S. recession. Global stock market corrections and volatility.

April 2, the mark to market method of valuing mortgage backed securities were abolished improving confidence in the asset class and trust between banks.

The examples we have of past cycles indicate that major declines in real home prices—even 50 percent declines in some places—are entirely possible going forward from today or from the not too distant future.

The Federal National Mortgage Association (FNMA), commonly known as Fannie Mae, is a United States government-sponsored enterprise (GSE) and, since 1968, a publicly traded company. Founded in 1938 during the Great Depression as part of the New Deal, the corporation's purpose is to expand the secondary mortgage market by securitizing mortgage loans in the form of mortgage-backed securities (MBS), allowing lenders to reinvest their assets into more lending and in effect increasing the number of lenders in the mortgage market by reducing the reliance on locally based savings and loan associations. Its brother organization is the Federal Home Loan Mortgage Corporation (FHLMC), better known as Freddie Mac. In 2023, Fannie Mae was ranked number 28 on the Fortune 500 rankings of the largest United States corporations by total revenue.

The Community Reinvestment Act is a United States federal law designed to encourage commercial banks and savings associations to help meet the needs of borrowers in all segments of their communities, including low- and moderate-income neighborhoods. Congress passed the Act in 1977 to reduce discriminatory credit practices against low-income neighborhoods, a practice known as redlining.

The Federal Home Loan Mortgage Corporation (FHLMC), commonly known as Freddie Mac, is a publicly traded, government-sponsored enterprise (GSE), headquartered in Tysons, Virginia. The FHLMC was created in 1970 to expand the secondary market for mortgages in the US. Along with the Federal National Mortgage Association, Freddie Mac buys mortgages, pools them, and sells them as a mortgage-backed security (MBS) to private investors on the open market. This secondary mortgage market increases the supply of money available for mortgage lending and increases the money available for new home purchases. The name "Freddie Mac" is a variant of the FHLMC initialism of the company's full name that was adopted officially for ease of identification.

A mortgage-backed security (MBS) is a type of asset-backed security which is secured by a mortgage or collection of mortgages. The mortgages are aggregated and sold to a group of individuals that securitizes, or packages, the loans together into a security that investors can buy. Bonds securitizing mortgages are usually treated as a separate class, termed residential; another class is commercial, depending on whether the underlying asset is mortgages owned by borrowers or assets for commercial purposes ranging from office space to multi-dwelling buildings.

The 2000s United States housing bubble was a real-estate bubble affecting over half of the U.S. states. It was the impetus for the subprime mortgage crisis. Housing prices peaked in early 2006, started to decline in 2006 and 2007, and reached new lows in 2011. On December 30, 2008, the Case–Shiller home price index reported its largest price drop in its history. The credit crisis resulting from the bursting of the housing bubble is an important cause of the Great Recession in the United States.

In the United States, a jumbo mortgage is a mortgage loan that may have high credit quality, but is in an amount above conventional conforming loan limits. This standard is set by the two government-sponsored enterprises, Fannie Mae and Freddie Mac, and sets the limit on the maximum value of any individual mortgage they will purchase from a lender. Fannie Mae (FNMA) and Freddie Mac (FHLMC) are large agencies that purchase the bulk of U.S. residential mortgages from banks and other lenders, allowing them to free up liquidity to lend more mortgages. When FNMA and FHLMC limits don't cover the full loan amount, the loan is referred to as a "jumbo mortgage". Traditionally, the interest rates on jumbo mortgages are higher than for conforming mortgages, however with GSE fees increasing, Jumbo loans have recently seen lower interest rates than conforming loans.

Mortgage discrimination or mortgage lending discrimination is the practice of banks, governments or other lending institutions denying loans to one or more groups of people primarily on the basis of race, ethnic origin, sex or religion.

The United States subprime mortgage crisis was a multinational financial crisis that occurred between 2007 and 2010 that contributed to the 2007–2008 global financial crisis. The crisis led to a severe economic recession, with millions of people losing their jobs and many businesses going bankrupt. The U.S. government intervened with a series of measures to stabilize the financial system, including the Troubled Asset Relief Program (TARP) and the American Recovery and Reinvestment Act (ARRA).

United States housing prices experienced a major market correction after the housing bubble that peaked in early 2006. Prices of real estate then adjusted downwards in late 2006, causing a loss of market liquidity and subprime defaults.

The subprime mortgage crisis impact timeline lists dates relevant to the creation of a United States housing bubble and the 2005 housing bubble burst and the subprime mortgage crisis which developed during 2007 and 2008. It includes United States enactment of government laws and regulations, as well as public and private actions which affected the housing industry and related banking and investment activity. It also notes details of important incidents in the United States, such as bankruptcies and takeovers, and information and statistics about relevant trends. For more information on reverberations of this crisis throughout the global financial system see Financial crisis of 2007–2008.

Loss mitigation is used to describe a third party helping a homeowner, a division within a bank that mitigates the loss of the bank, or a firm that handles the process of negotiation between a homeowner and the homeowner's lender. Loss mitigation works to negotiate mortgage terms for the homeowner that will prevent foreclosure. These new terms are typically obtained through loan modification, short sale negotiation, short refinance negotiation, deed in lieu of foreclosure, cash-for-keys negotiation, a partial claim loan, repayment plan, forbearance, or other loan work-out. All of the options serve the same purpose, to stabilize the risk of loss the lender (investor) is in danger of realizing.

Observers and analysts have attributed the reasons for the 2001–2006 housing bubble and its 2007–10 collapse in the United States to "everyone from home buyers to Wall Street, mortgage brokers to Alan Greenspan". Other factors that are named include "Mortgage underwriters, investment banks, rating agencies, and investors", "low mortgage interest rates, low short-term interest rates, relaxed standards for mortgage loans, and irrational exuberance" Politicians in both the Democratic and Republican political parties have been cited for "pushing to keep derivatives unregulated" and "with rare exceptions" giving Fannie Mae and Freddie Mac "unwavering support".

The United States Housing and Economic Recovery Act of 2008 was designed primarily to address the subprime mortgage crisis. It authorized the Federal Housing Administration to guarantee up to $300 billion in new 30-year fixed rate mortgages for subprime borrowers if lenders wrote down principal loan balances to 90 percent of current appraisal value. It was intended to restore confidence in Fannie Mae and Freddie Mac by strengthening regulations and injecting capital into the two large U.S. suppliers of mortgage funding. States are authorized to refinance subprime loans using mortgage revenue bonds. Enactment of the Act led to the government conservatorship of Fannie Mae and Freddie Mac.

In September 2008 the Federal Housing Finance Agency (FHFA) announced that it would take over the Federal National Mortgage Association and the Federal Home Loan Mortgage Corporation. Both government-sponsored enterprises, which finance home mortgages in the United States by issuing bonds, had become illiquid as the market for those bonds collapsed in the subprime mortgage crisis. The FHFA established conservatorships in which each enterprise's management works under the FHFA's direction to reduce losses and to develop a new operating structure that will allow a return to self-management.

This article provides background information regarding the subprime mortgage crisis. It discusses subprime lending, foreclosures, risk types, and mechanisms through which various entities involved were affected by the crisis.

The U.S. subprime mortgage crisis was a set of events and conditions that led to a financial crisis and subsequent recession that began in 2007. It was characterized by a rise in subprime mortgage delinquencies and foreclosures, and the resulting decline of securities backed by said mortgages. Several major financial institutions collapsed in September 2008, with significant disruption in the flow of credit to businesses and consumers and the onset of a severe global recession.

Loan modification is the systematic alteration of mortgage loan agreements that help those having problems making the payments by reducing interest rates, monthly payments or principal balances. Lending institutions could make one or more of these changes to relieve financial pressure on borrowers to prevent the condition of foreclosure. Loan modifications have been practiced in the United States since the 1930s. During the Great Depression, loan modification programs took place at the state level in an effort to reduce levels of loan foreclosures.

Many factors directly and indirectly serve as the causes of the Great Recession that started in 2008 with the US subprime mortgage crisis. The major causes of the initial subprime mortgage crisis and the following recession include lax lending standards contributing to the real-estate bubbles that have since burst; U.S. government housing policies; and limited regulation of non-depository financial institutions. Once the recession began, various responses were attempted with different degrees of success. These included fiscal policies of governments; monetary policies of central banks; measures designed to help indebted consumers refinance their mortgage debt; and inconsistent approaches used by nations to bail out troubled banking industries and private bondholders, assuming private debt burdens or socializing losses.

The mortgage industry of the United States is a major financial sector. The federal government created several programs, or government sponsored entities, to foster mortgage lending, construction and encourage home ownership. These programs include the Government National Mortgage Association, the Federal National Mortgage Association and the Federal Home Loan Mortgage Corporation.

The 2007–2008 financial crisis, or Global Financial Crisis (GFC), was a severe worldwide economic crisis that occurred in the early 21st century. It was the most serious financial crisis since the Great Depression (1929). Predatory lending targeting low-income homebuyers, excessive risk-taking by global financial institutions, and the bursting of the United States housing bubble culminated in a "perfect storm".