A dividend is a distribution of profits by a corporation to its shareholders. When a corporation earns a profit or surplus, it is able to pay a portion of the profit as a dividend to shareholders. Any amount not distributed is taken to be re-invested in the business. The current year profit as well as the retained earnings of previous years are available for distribution; a corporation is usually prohibited from paying a dividend out of its capital. Distribution to shareholders may be in cash or, if the corporation has a dividend reinvestment plan, the amount can be paid by the issue of further shares or by share repurchase. In some cases, the distribution may be of assets.

A security is a tradable financial asset. The term commonly refers to any form of financial instrument, but its legal definition varies by jurisdiction. In some countries and languages people commonly use the term "security" to refer to any form of financial instrument, even though the underlying legal and regulatory regime may not have such a broad definition. In some jurisdictions the term specifically excludes financial instruments other than equities and fixed income instruments. In some jurisdictions it includes some instruments that are close to equities and fixed income, e.g., equity warrants.

An initial public offering (IPO) or stock launch is a public offering in which shares of a company are sold to institutional investors and usually also to retail (individual) investors. An IPO is typically underwritten by one or more investment banks, who also arrange for the shares to be listed on one or more stock exchanges. Through this process, colloquially known as floating, or going public, a privately held company is transformed into a public company. Initial public offerings can be used to raise new equity capital for companies, to monetize the investments of private shareholders such as company founders or private equity investors, and to enable easy trading of existing holdings or future capital raising by becoming publicly traded.

The Sarbanes–Oxley Act of 2002 is a United States federal law that mandates certain practices in financial record keeping and reporting for corporations. The act,, also known as the "Public Company Accounting Reform and Investor Protection Act" and "Corporate and Auditing Accountability, Responsibility, and Transparency Act" and more commonly called Sarbanes–Oxley, SOX or Sarbox, contains eleven sections that place requirements on all U.S. public company boards of directors and management and public accounting firms. A number of provisions of the Act also apply to privately held companies, such as the willful destruction of evidence to impede a federal investigation.

The Harken Energy Scandal refers to a series of transactions entered into during 1990 involving Harken Energy. These transactions are alleged to involve either issues relating to insider trading, or influence peddling. Although no wrongdoings were found by any investigating authorities, the matter generated political controversy.

The Securities Act of 1933, also known as the 1933 Act, the Securities Act, the Truth in Securities Act, the Federal Securities Act, and the '33 Act, was enacted by the United States Congress on May 27, 1933, during the Great Depression and after the stock market crash of 1929. It is an integral part of United States securities regulation. It is legislated pursuant to the Interstate Commerce Clause of the Constitution.

An American depositary receipt is a negotiable security that represents securities of a foreign company and allows that company's shares to trade in the U.S. financial markets.

An exchange-traded fund (ETF) is a type of investment fund that is also an exchange-traded product, i.e., it is traded on stock exchanges. ETFs own financial assets such as stocks, bonds, currencies, debts, futures contracts, and/or commodities such as gold bars. The list of assets that each ETF owns, as well as their weightings, is posted on the website of the issuer daily, or quarterly in the case of active non-transparent ETFs. Many ETFs provide some level of diversification compared to owning an individual stock.

Stock valuation is the method of calculating theoretical values of companies and their stocks. The main use of these methods is to predict future market prices, or more generally, potential market prices, and thus to profit from price movement – stocks that are judged undervalued are bought, while stocks that are judged overvalued are sold, in the expectation that undervalued stocks will overall rise in value, while overvalued stocks will generally decrease in value. A target price is a price at which an analyst believes a stock to be fairly valued relative to its projected and historical earnings.

Employee stock options (ESO) is a label that refers to compensation contracts between an employer and an employee that carries some characteristics of financial options.

Investor relations (IR) is a "strategic management responsibility that is capable of integrating finance, communication, marketing and securities law compliance to enable the most effective two-way communication between a company, the financial community, and other constituencies, which ultimately contributes to a company's securities achieving fair valuation." as defined by National Investor Relations Institute (NIRI). IR is also function to assess the impact of a company actions on the company's position in the capital markets.

Shares outstanding are all the shares of a corporation that have been authorized, issued and purchased by investors and are held by them. They are distinguished from treasury shares, which are shares held by the corporation itself, thus representing no exercisable rights. Shares outstanding and treasury shares together amount to the number of issued shares.

Regulation FD (Fair Disclosure), ordinarily referred to as Regulation FD or Reg FD, is a regulation that was promulgated by the U.S. Securities and Exchange Commission (SEC) in August 2000. The regulation is codified as 17 CFR 243. Although "FD" stands for "fair disclosure", as can be learned from the adopting release, the regulation was and is codified in the Code of Federal Regulations simply as Regulation FD. Subject to certain limited exceptions, the rules generally prohibit public companies from disclosing previously nonpublic, material information to certain parties unless the information is distributed to the public first or simultaneously.

Securities fraud, also known as stock fraud and investment fraud, is a deceptive practice in the stock or commodities markets that induces investors to make purchase or sale decisions on the basis of false information. The setups are generally made to result in monetary gain for the deceivers, and generally result in unfair monetary losses for the investors. They are generally violating securities laws.

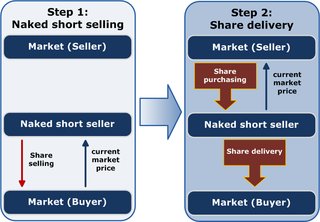

Naked short selling, or naked shorting, is the practice of short-selling a tradable asset of any kind without first borrowing the asset from someone else or ensuring that it can be borrowed. When the seller does not obtain the asset and deliver it to the buyer within the required time frame, the result is known as a "failure to deliver" (FTD). The transaction generally remains open until the asset is acquired and delivered by the seller, or the seller's broker settles the trade on their behalf.

A preannouncement occurs when a company or individual announces something either prior to the time that they do it or prior to the time that they would normally announce it. Preannouncements can take the form of a press release, filing a form with the government, a conference call, or a webcast.

Share repurchase, also known as share buyback or stock buyback, is the reacquisition by a company of its own shares. It represents an alternate and more flexible way of returning money to shareholders. When used in coordination with increased corporate leverage, buybacks can increase share prices.

Regulation S-K is a prescribed regulation under the US Securities Act of 1933 that lays out reporting requirements for various SEC filings used by public companies. Companies are also often called issuers, filers or registrants.

A financial ratio or accounting ratio states the relative magnitude of two selected numerical values taken from an enterprise's financial statements. Often used in accounting, there are many standard ratios used to try to evaluate the overall financial condition of a corporation or other organization. Financial ratios may be used by managers within a firm, by current and potential shareholders (owners) of a firm, and by a firm's creditors. Financial analysts use financial ratios to compare the strengths and weaknesses in various companies. If shares in a company are traded in a financial market, the market price of the shares is used in certain financial ratios.

The technology company Facebook, Inc., held its initial public offering (IPO) on Friday, May 18, 2012. The IPO was one of the biggest in technology and Internet history, with a peak market capitalization of over $104 billion.