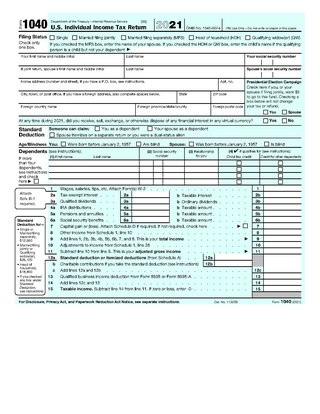

Form 1040, officially, the U.S. Individual Income Tax Return, is an IRS tax form used for personal federal income tax returns filed by United States residents. The form calculates the total taxable income of the taxpayer and determines how much is to be paid to or refunded by the government.

The United States of America has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2020, taxes collected by federal, state, and local governments amounted to 25.5% of GDP, below the OECD average of 33.5% of GDP.

Under United States tax law, itemized deductions are eligible expenses that individual taxpayers can claim on federal income tax returns and which decrease their taxable income, and are claimable in place of a standard deduction, if available.

Payroll taxes are taxes imposed on employers or employees, and are usually calculated as a percentage of the salaries that employers pay their employees. By law, some payroll taxes are the responsibility of the employee and others fall on the employer, but almost all economists agree that the true economic incidence of a payroll tax is unaffected by this distinction, and falls largely or entirely on workers in the form of lower wages. Because payroll taxes fall exclusively on wages and not on returns to financial or physical investments, payroll taxes may contribute to underinvestment in human capital, such as higher education.

Three key types of withholding tax are imposed at various levels in the United States:

A tax refund or tax rebate is a payment to the taxpayer due to the taxpayer having paid more tax than they owed.

An Individual Taxpayer Identification Number (ITIN) is a United States tax processing number issued by the Internal Revenue Service (IRS). It is a nine-digit number beginning with the number “9”, has a range of numbers from "50" to "65", "70" to "88", “90” to “92” and “94” to “99” for the fourth and fifth digits, and is formatted like a SSN. ITIN numbers are issued by the IRS to individuals who do not have and are not eligible to obtain a valid U.S. Social Security Number, but who are required by law to file a U.S. Individual Income Tax Return.

Form W-2 is an Internal Revenue Service (IRS) tax form used in the United States to report wages paid to employees and the taxes withheld from them. Employers must complete a Form W-2 for each employee to whom they pay a salary, wage, or other compensation as part of the employment relationship. An employer must mail out the Form W-2 to employees on or before January 31 of any year in which an employment relationship existed and which was not contractually independent. This deadline gives these taxpayers about 2 months to prepare their returns before the April 15 income tax due date. The form is also used to report FICA taxes to the Social Security Administration. Form W-2 along with Form W-3 generally must be filed by the employer with the Social Security Administration by the end of February following employment the previous year. Relevant amounts on Form W-2 are reported by the Social Security Administration to the Internal Revenue Service. In US territories, the W-2 is issued with a two letter territory code, such as W-2GU for Guam. Corrections can be filed using Form W-2c.

Form 1099 is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

Tax withholding, also known as tax retention, pay-as-you-earn tax or tax deduction at source, is income tax paid to the government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient. In most jurisdictions, tax withholding applies to employment income. Many jurisdictions also require withholding taxes on payments of interest or dividends. In most jurisdictions, there are additional tax withholding obligations if the recipient of the income is resident in a different jurisdiction, and in those circumstances withholding tax sometimes applies to royalties, rent or even the sale of real estate. Governments use tax withholding as a means to combat tax evasion, and sometimes impose additional tax withholding requirements if the recipient has been delinquent in filing tax returns, or in industries where tax evasion is perceived to be common.

The United States federal government and most state governments impose an income tax. They are determined by applying a tax rate, which may increase as income increases, to taxable income, which is the total income less allowable deductions. Income is broadly defined. Individuals and corporations are directly taxable, and estates and trusts may be taxable on undistributed income. Partnerships are not taxed, but their partners are taxed on their shares of partnership income. Residents and citizens are taxed on worldwide income, while nonresidents are taxed only on income within the jurisdiction. Several types of credits reduce tax, and some types of credits may exceed tax before credits. Most business expenses are deductible. Individuals may deduct certain personal expenses, including home mortgage interest, state taxes, contributions to charity, and some other items. Some deductions are subject to limits, and an Alternative Minimum Tax (AMT) applies at the federal and some state levels.

Tax preparation is the process of preparing tax returns, often income tax returns, often for a person other than the taxpayer, and generally for compensation. Tax preparation may be done by the taxpayer with or without the help of tax preparation software and online services. Tax preparation may also be done by a licensed professional such as an attorney, certified public accountant or enrolled agent, or by an unlicensed tax preparation business. Because United States income tax laws are considered to be complicated, many taxpayers seek outside assistance with taxes.

Taxpayers in the United States may face various penalties for failures related to Federal, state, and local tax matters. The Internal Revenue Service (IRS) is primarily responsible for charging these penalties at the Federal level. The IRS can assert only those penalties specified imposed under Federal tax law. State and local rules vary widely, are administered by state and local authorities, and are not discussed herein.

The United States Internal Revenue Service (IRS) uses forms for taxpayers and tax-exempt organizations to report financial information, such as to report income, calculate taxes to be paid to the federal government, and disclose other information as required by the Internal Revenue Code (IRC). There are over 800 various forms and schedules. Other tax forms in the United States are filed with state and local governments.

E-file is a system for submitting tax documents to the US Internal Revenue Service through the Internet or direct connection, usually without the need to submit any paper documents. Tax preparation software with e-filing capabilities includes stand-alone programs or websites. Tax professionals use tax preparation software from major software vendors for commercial use.

Customer Account Data Engine (CADE) is the name of two Internal Revenue Service (IRS) tax processing systems, used for filing United States income tax returns. Work on the original CADE, designed to replace the Individual Master File (IMF) system, was begun in 2000 and stopped in 2009. The original CADE is in active use; for instance, in 2009, it was used to process over 40 million tax returns.

The United States taxes citizens and residents on their worldwide income. Citizens and residents living and working outside the U.S. may be entitled to a foreign earned income exclusion that reduces taxable income. For 2024, the maximum exclusion is $126,500 per taxpayer. Taxpayers filing a joint return are entitled to up to two exclusions if both have earned income. In addition, the taxpayer may exclude housing expenses in excess of 16% of this maximum but with limits.

Tax protesters in the United States advance a number of administrative arguments asserting that the assessment and collection of the federal income tax violates regulations enacted by responsible agencies –primarily the Internal Revenue Service (IRS)– tasked with carrying out the statutes enacted by the United States Congress and signed into law by the President. Such arguments generally include claims that the administrative agency fails to create a duty to pay taxes, or that its operation conflicts with some other law, or that the agency is not authorized by statute to assess or collect income taxes, to seize assets to satisfy tax claims, or to penalize persons who fail to file a return or pay the tax.

In the United States, an income tax audit is the examination of a business or individual tax return by the Internal Revenue Service (IRS) or state tax authority. The IRS and various state revenue departments use the terms audit, examination, review, and notice to describe various aspects of enforcement and administration of the tax laws.

Form 1095 is a collection of Internal Revenue Service (IRS) tax forms in the United States which are used to determine whether an individual is required to pay the individual shared responsibility provision. Individuals can also use the health insurance information contained in the form/forms to help them fill out their tax returns. The individual forms are Form 1095-A "A Health Insurance Marketplace Statement", Form 1095-B "Health Coverage", and Form 1095-C "Employer-Provided Health Insurance Offer and Coverage". Individuals may receive one or multiple versions of Form 1095.