Related Research Articles

An oligopoly is a market in which control over an industry lies in the hands of a few large sellers who own a dominant share of the market. Oligopolistic markets have homogenous products, few market participants, and inelastic demand for the products in those industries. As a result of their significant market power, firms in oligopolistic markets can influence prices through manipulating the supply function. Firms in an oligopoly are also mutually interdependent, as any action by one firm is expected to affect other firms in the market and evoke a reaction or consequential action. As a result, firms in oligopolistic markets often resort to collusion as means of maximising profits.

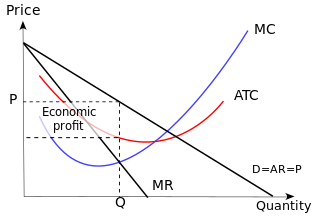

In economics, imperfect competition refers to a situation where the characteristics of an economic market do not fulfil all the necessary conditions of a perfectly competitive market. Imperfect competition causes market inefficiencies, resulting in market failure. Imperfect competition usually describes behaviour of suppliers in a market, such that the level of competition between sellers is below the level of competition in perfectly competitive market conditions.

Competition is a rivalry where two or more parties strive for a common goal which cannot be shared: where one's gain is the other's loss. Competition can arise between entities such as organisms, individuals, economic and social groups, etc. The rivalry can be over attainment of any exclusive goal, including recognition.

Retail is the sale of goods and services to consumers, in contrast to wholesaling, which is the sale to business or institutional customers. A retailer purchases goods in large quantities from manufacturers, directly or through a wholesaler, and then sells in smaller quantities to consumers for a profit. Retailers are the final link in the supply chain from producers to consumers.

Positioning refers to the place that a brand occupies in the minds of the customers and how it is distinguished from the products of the competitors. It is different from the concept of brand awareness. In order to position products or brands, companies may emphasize the distinguishing features of their brand or they may try to create a suitable image through the marketing mix. Once a brand has achieved a strong position, it can become difficult to reposition it. To effectively position a brand and create a lasting brand memory, brands need to be able to connect to consumers in an authentic way, creating a brand persona usually helps build this sort of connection.

Pricing is the process whereby a business sets the price at which it will sell its products and services and may be part of the business's marketing plan. In setting prices, the business will take into account the price at which it could acquire the goods, the manufacturing cost, the marketplace, competition, market condition, brand, and quality of the product.

In economics and marketing, product differentiation is the process of distinguishing a product or service from others to make it more attractive to a particular target market. This involves differentiating it from competitors' products as well as from a firm's other products. The concept was proposed by Edward Chamberlin in his 1933 book, The Theory of Monopolistic Competition.

In business, a competitive advantage is an attribute that allows an organization to outperform its competitors.

A price war is a form of market competition in which companies within an industry engage in aggressive pricing strategies, “characterized by the repeated cutting of prices below those of competitors”. This leads to a vicious cycle, where each competitor attempts to match or undercut the price of the other. Competitors are driven to follow the initial price-cut due to the downward pricing pressure, referred to as “price-cutting momentum”.

Marketing strategy refers to efforts undertaken by an organization to increase its sales and achieve competitive advantage. In other words, it is the method of advertising a company's products to the public through an established plan through the meticulous planning and organization of ideas, data, and information.

Anti-competitive practices are business or government practices that prevent or reduce competition in a market. Antitrust laws ensure businesses do not engage in competitive practices that harm other, usually smaller, businesses or consumers. These laws are formed to promote healthy competition within a free market by limiting the abuse of monopoly power. Competition allows companies to compete in order for products and services to improve; promote innovation; and provide more choices for consumers. In order to obtain greater profits, some large enterprises take advantage of market power to hinder survival of new entrants. Anti-competitive behavior can undermine the efficiency and fairness of the market, leaving consumers with little choice to obtain a reasonable quality of service.

In economics and commerce, the Bertrand paradox — named after its creator, Joseph Bertrand — describes a situation in which two players (firms) reach a state of Nash equilibrium where both firms charge a price equal to marginal cost ("MC"). The paradox is that in models such as Cournot competition, an increase in the number of firms is associated with a convergence of prices to marginal costs. In these alternative models of oligopoly, a small number of firms earn positive profits by charging prices above cost. Suppose two firms, A and B, sell a homogeneous commodity, each with the same cost of production and distribution, so that customers choose the product solely on the basis of price. It follows that demand is infinitely price-elastic. Neither A nor B will set a higher price than the other because doing so would yield the entire market to their rival. If they set the same price, the companies will share both the market and profits.

Non-price competition is a marketing strategy "in which one firm tries to distinguish its product or service from competing products on the basis of attributes like design and workmanship". It often occurs in imperfectly competitive markets because it exists between two or more producers that sell goods and services at the same prices but compete to increase their respective market shares through non-price measures such as marketing schemes and greater quality. It is a form of competition that requires firms to focus on product differentiation instead of pricing strategies among competitors. Such differentiation measures allowing for firms to distinguish themselves, and their products from competitors, may include, offering superb quality of service, extensive distribution, customer focus, or any sustainable competitive advantage other than price. When price controls are not present, the set of competitive equilibria naturally correspond to the state of natural outcomes in Hatfield and Milgrom's two-sided matching with contracts model.

A business can use a variety of pricing strategies when selling a product or service. To determine the most effective pricing strategy for a company, senior executives need to first identify the company's pricing position, pricing segment, pricing capability and their competitive pricing reaction strategy. Pricing strategies and tactics vary from company to company, and also differ across countries, cultures, industries and over time, with the maturing of industries and markets and changes in wider economic conditions.

Once the strategic plan is in place, retail managers turn to the more managerial aspects of planning. A retail mix is devised for the purpose of coordinating day-to-day tactical decisions. The retail marketing mix typically consists of six broad decision layers including product decisions, place decisions, promotion, price, personnel and presentation. The retail mix is loosely based on the marketing mix, but has been expanded and modified in line with the unique needs of the retail context. A number of scholars have argued for an expanded marketing, mix with the inclusion of two new Ps, namely, Personnel and Presentation since these contribute to the customer's unique retail experience and are the principal basis for retail differentiation. Yet other scholars argue that the Retail Format should be included. The modified retail marketing mix that is most commonly cited in textbooks is often called the 6 Ps of retailing.

Market dominance is the control of a economic market by a firm. A dominant firm possesses the power to affect competition and influence market price. A firms' dominance is a measure of the power of a brand, product, service, or firm, relative to competitive offerings, whereby a dominant firm can behave independent of their competitors or consumers, and without concern for resource allocation. Dominant positioning is both a legal concept and an economic concept and the distinction between the two is important when determining whether a firm's market position is dominant.

In marketing, a customer value proposition (CVP) consists of the sum total of benefits which a vendor promises a customer will receive in return for the customer's associated payment.

In competition law, before deciding whether companies have significant market power which would justify government intervention, the test of small but significant and non-transitory increase in price (SSNIP) is used to define the relevant market in a consistent way. It is an alternative to ad hoc determination of the relevant market by arguments about product similarity.

The following outline is provided as an overview of and topical guide to marketing:

The retail life cycle theory holds that retail institutions experience the cycle of innovation, growth, maturity and decline, like goods and services that they sell, similar to that of the product life cycle. The market traits and strategies which are taken by retail institutions should differ in variable stages of retail life cycle. The theory of retail life cycle is first introduced by William Davidson W. R, Betas A. D and Bass S. J in 1976.

References

- ↑ DeSarbo, Wayne S., Rajdeep Grewal, and Jerry Wind. "Who competes with whom? A demand‐based perspective for identifying and representing asymmetric competition." Strategic Management Journal 27, no. 2 (2006): 101–129.

- ↑ Carpenter, Gregory S., Lee G. Cooper, Dominique M. Hanssens, and David F. Midgley. "Modeling asymmetric competition." Marketing Science 7, no. 4 (1988): 393–412.

- ↑ Gonzalez-Benito, Oscar, Pablo A. Munoz-Gallego, and Praveen K. Kopalle. "Asymmetric competition in retail store formats: Evaluating inter-and intra-format spatial effects." Journal of Retailing 81, no. 1 (2005): 59–73.

- ↑ Heath, Timothy B., Gangseog Ryu, Subimal Chatterjee, Michael S. McCarthy, David L. Mothersbaugh, Sandra Milberg, and Gary J. Gaeth. "Asymmetric competition in choice and the leveraging of competitive disadvantages." Journal of Consumer Research 27, no. 3 (2000): 291–308.

| | This marketing-related article is a stub. You can help Wikipedia by expanding it. |