This article includes a list of general references, but it lacks sufficient corresponding inline citations .(July 2020) |

Christine Maria Jasch (born 7 November 1960 in Vienna) is an Austrian economist, author and accountant. [1] [2]

This article includes a list of general references, but it lacks sufficient corresponding inline citations .(July 2020) |

Christine Maria Jasch (born 7 November 1960 in Vienna) is an Austrian economist, author and accountant. [1] [2]

Christine Jasch completed secondary school in Vienna, where she matriculated in 1979 to study at the University of Vienna's Department of Economics, and at the University of Natural Resources and Life Sciences, Vienna. In 1984 she applied for a Studium Irregulare for Ecological Economics. She became a certified public accountant in 1989 and lead verifier according to the EU EMAS Regulation in 1995. In 1989 she founded the Vienna Institute for Environmental Management and Economics, IÖW. In 1999, she habilitated (qualified for professorship) in Environmental Management and Economics at the Austrian University for Agriculture. Since 2011 she has been responsible for the auditing of sustainability reports and certification of environmental management systems for Ernst & Young Climate Change and Sustainability Services, Vienna.

Jasch's work focuses on the combination of environmental and sustainability issues with economic instruments, including environmental cost accounting and sustainability reporting. Her IÖW work has included methodological development as well as practical implementation guidelines for environmental management tools.

Working areas include environmental performance evaluation and sustainability indicators, integrated information and management systems, environmental and sustainability accounting, material flow cost accounting, impact assessment, ISO standardization for environmental management, sustainability reporting, sustainable product service systems and socially responsible investing, cleaner technologies.

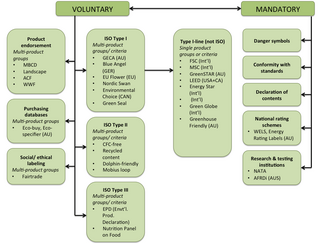

On behalf of the Austrian environmental ministry since 1993 she negotiated the ISO standards ISO 14001 environmental management systems, ISO 14031 Environmental Performance Evaluation and ISO 14041 Material Flow Cost Accounting.

In 2000, via the Sustainability Group of the Austrian Chamber for Accountants and Auditors, which she chairs, she founded the Austrian Sustainability Reporting Awards, ASRA, which are granted annually since in cooperation with partners.

From 2000 – 2006 she was member of the United Nations Working Group on Environmental Management Accounting. For them she wrote a book on principles and procedures for environmental management accounting, which was the basis for her later work on the IFAC Guidance document on environmental management accounting, released in 2005. UNIDO is using this approach to combine it with Cleaner Technologies and Environmental Management Systems and thus establish arguments and a baseline for environmental protection and related cost savings by improved resource efficiency. In Austria the national law for the implementation of the EU emission trading scheme requests a separately qualified accounting expert for data monitoring in the audit team, in addition to a process engineer and a chemist. Christine Jasch has qualified as such in 2005 and works on CO2 audits with TUEV Austria. In April 2008 she was voted into the board of directors of oekostrom AG where she served till 2013. Lecturing engagements exist or existed with the University of Natural Resources and Life Sciences, Vienna, the University of Klagenfurt, the University of Applied Sciences Wiener Neustadt Campus Wieselburg, the University of Applied Sciences Kufstein, the University of Applied Sciences Technikum Wien, Vienna and the Danube University Krems.

ISO 14000 is a family of standards by the International Organization for Standardization (ISO) related to environmental management that exists to help organizations (a) minimize how their operations negatively affect the environment ; (b) comply with applicable laws, regulations, and other environmentally oriented requirements; and (c) continually improve in the above.

The following outline is provided as an overview of and topical guide to sustainable agriculture:

Industrial ecology (IE) is the study of material and energy flows through industrial systems. The global industrial economy can be modelled as a network of industrial processes that extract resources from the Earth and transform those resources into by-products, products and services which can be bought and sold to meet the needs of humanity. Industrial ecology seeks to quantify the material flows and document the industrial processes that make modern society function. Industrial ecologists are often concerned with the impacts that industrial activities have on the environment, with use of the planet's supply of natural resources, and with problems of waste disposal. Industrial ecology is a young but growing multidisciplinary field of research which combines aspects of engineering, economics, sociology, toxicology and the natural sciences.

An audit is an "independent examination of financial information of any entity, whether profit oriented or not, irrespective of its size or legal form when such an examination is conducted with a view to express an opinion thereon." Auditing also attempts to ensure that the books of accounts are properly maintained by the concern as required by law. Auditors consider the propositions before them, obtain evidence, and evaluate the propositions in their auditing report.

A green economy is an economy that aims at reducing environmental risks and ecological scarcities, and that aims for sustainable development without degrading the environment. It is closely related with ecological economics, but has a more politically applied focus. The 2011 UNEP Green Economy Report argues "that to be green, an economy must not only be efficient, but also fair. Fairness implies recognizing global and country level equity dimensions, particularly in assuring a Just Transition to an economy that is low-carbon, resource efficient, and socially inclusive."

Environmental resource management is the management of the interaction and impact of human societies on the environment. It is not, as the phrase might suggest, the management of the environment itself. Environmental resources management aims to ensure that ecosystem services are protected and maintained for future human generations, and also maintain ecosystem integrity through considering ethical, economic, and scientific (ecological) variables. Environmental resource management tries to identify factors affected by conflicts that rise between meeting needs and protecting resources. It is thus linked to environmental protection, sustainability, integrated landscape management, natural resource management, fisheries management, forest management, and wildlife management, and others.

Ecolabels and Green Stickers are labeling systems for food and consumer products. The use of ecolabels is voluntary, whereas green stickers are mandated by law; for example, in North America major appliances and automobiles use Energy Star. They are a form of sustainability measurement directed at consumers, intended to make it easy to take environmental concerns into account when shopping. Some labels quantify pollution or energy consumption by way of index scores or units of measurement, while others assert compliance with a set of practices or minimum requirements for sustainability or reduction of harm to the environment. Many ecolabels are focused on minimising the negative ecological impacts of primary production or resource extraction in a given sector or commodity through a set of good practices that are captured in a sustainability standard. Through a verification process, usually referred to as "certification", a farm, forest, fishery, or mine can show that it complies with a standard and earn the right to sell its products as certified through the supply chain, often resulting in a consumer-facing ecolabel.

Environmental accounting is a subset of accounting proper, its target being to incorporate both economic and environmental information. It can be conducted at the corporate level or at the level of a national economy through the System of Integrated Environmental and Economic Accounting, a satellite system to the National Accounts of Countries.

Material flow analysis (MFA), also referred to as substance flow analysis (SFA), is an analytical method to quantify flows and stocks of materials or substances in a well-defined system. MFA is an important tool to study the bio-physical aspects of human activity on different spatial and temporal scales. It is considered a core method of industrial ecology or anthropogenic, urban, social and industrial metabolism. MFA is used to study material, substance, or product flows across different industrial sectors or within ecosystems. MFA can also be applied to a single industrial installation, for example, for tracking nutrient flows through a waste water treatment plant. When combined with an assessment of the costs associated with material flows this business-oriented application of MFA is called material flow cost accounting. MFA is an important tool to study the circular economy and to devise material flow management. Since the 1990s, the number of publications related to material flow analysis has grown steadily. Peer-reviewed journals that publish MFA-related work include the Journal of Industrial Ecology, Ecological Economics, Environmental Science and Technology, and Resources, Conservation, and Recycling.

Sustainability accounting was originated about 20 years ago and is considered a subcategory of financial accounting that focuses on the disclosure of non-financial information about a firm's performance to external stakeholders, such as capital holders, creditors, and other authorities. Sustainability accounting represents the activities that have a direct impact on society, environment, and economic performance of an organisation. Sustainability accounting in managerial accounting contrasts with financial accounting in that managerial accounting is used for internal decision making and the creation of new policies that will have an effect on the organisation's performance at economic, ecological, and social level. Sustainability accounting is often used to generate value creation within an organisation.

This page is an index of sustainability articles.

In 1997, a core set of six principles was established by ecological economist Robert Costanza for the sustainability governance of the oceans. These six principles became known as the "Lisbon Principles": together they provide basic guidelines for administering the use of common natural and social resources.

Small and Medium Enterprises (SMEs) are defined by the European Commission as having less than 250 employees, independent and with an annual turnover of no more than €50 million or annual balance sheet of €43 million.

Environmental certification is a form of environmental regulation and development where a company can voluntarily choose to comply with predefined processes or objectives set forth by the certification service. Most certification services have a logo which can be applied to products certified under their standards. This is seen as a form of corporate social responsibility allowing companies to address their obligation to minimise the harmful impacts to the environment by voluntarily following a set of externally set and measured objectives.

Natural capital accounting is the process of calculating the total stocks and flows of natural resources and services in a given ecosystem or region. Accounting for such goods may occur in physical or monetary terms. This process can subsequently inform government, corporate and consumer decision making as each relates to the use or consumption of natural resources and land, and sustainable behaviour.

Social accounting is the process of communicating the social and environmental effects of organizations' economic actions to particular interest groups within society and to society at large. Social Accounting is different from public interest accounting as well as from critical accounting.

Environmental systems analysis (ESA) is a systematic and systems based approach for describing human actions impacting on the natural environment to support decisions and actions aimed at perceived current or future environmental problems. Impacts of different types of objects are studied that ranges from projects, programs and policies, to organizations, and products. Environmental systems analysis encompasses a family of environmental assessment tools and methods, including life cycle assessment (LCA), material flow analysis (MFA) and substance flow analysis (SFA), and environmental impact assessment (EIA), among others.

Edeltraud 'Edel' Günther is a German business and sustainability assessment researcher, and university educator. Günther is currently the Director of the United Nations University Institute for Integrated Management of Material Fluxes and of Resources (UNU-FLORES) while on leave from the Technische Universität Dresden, where she has held the Chair of Business Management, esp. Sustainability Management and Environmental Accounting since 1996. She has also undertaken multiple international visiting professorships, and is the founding member of the Centre for Performance and Policy Research in Sustainability Measurement and Assessment (PRISMA).

Marina Fischer-Kowalski is an Austrian sociologist and social ecologist and a professor emeritus of the University of Klagenfurt, currently teaching at the University of Natural Resources and Life Sciences, Vienna, the University of Klagenfurt and the University of Vienna. She is known for founding the Vienna School of Social Ecology and for her pioneering work on the widely used metric for material and energy flows to complement economic accounting. Fischer-Kowalski works on socio-environmental change, sustainable development and the Anthropocene.

| International | |

|---|---|

| National | |

| Academics | |

| Other | |