A land value tax (LVT) is a levy on the value of land without regard to buildings, personal property and other improvements upon it. It is also known as a location value tax, a point valuation tax, a site valuation tax, split rate tax, or a site-value rating.

Council Tax is a local taxation system used in England, Scotland and Wales. It is a tax on domestic property, which was introduced in 1993 by the Local Government Finance Act 1992, replacing the short-lived Community Charge, which in turn replaced the domestic rates. Each property is assigned one of eight bands in England and Scotland, or nine bands in Wales, based on property value, and the tax is set as a fixed amount for each band. The higher the band, the higher the tax. Some property is exempt from the tax, and some people are exempt from the tax, while some get a discount.

A property tax is an ad valorem tax on the value of a property.

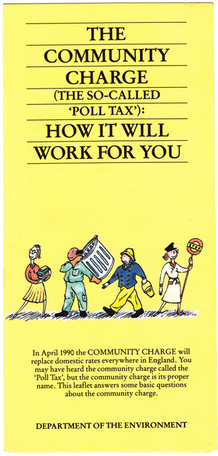

The Community Charge, commonly known as the poll tax, was a system of taxation introduced by Margaret Thatcher's government in replacement of domestic rates in Scotland from 1989, prior to its introduction in England and Wales from 1990. It provided for a single flat-rate, per-capita tax on every adult, at a rate set by the local authority. The charge was replaced by Council Tax in 1993, two years after its abolition was announced.

Rates are a type of property tax system in the United Kingdom, and in places with systems deriving from the British one, the proceeds of which are used to fund local government. Some other countries have taxes with a more or less comparable role, like France's taxe d'habitation.

Taxation in the United Kingdom may involve payments to at least three different levels of government: central government, devolved governments and local government. Central government revenues come primarily from income tax, National Insurance contributions, value added tax, corporation tax and fuel duty. Local government revenues come primarily from grants from central government funds, business rates in England, Council Tax and increasingly from fees and charges such as those for on-street parking. In the fiscal year 2014–15, total government revenue was forecast to be £648 billion, or 37.7 per cent of GDP, with net taxes and National Insurance contributions standing at £606 billion.

Distraint or distress is "the seizure of someone’s property in order to obtain payment of rent or other money owed", especially in common law countries. Distraint is the act or process "whereby a person, traditionally even without prior court approval, seizes the personal property of another located upon the distrainor's land in satisfaction of a claim, as a pledge for performance of a duty, or in reparation of an injury." Distraint typically involves the seizure of goods (chattels) belonging to the tenant by the landlord to sell the goods for the payment of the rent. In the past, distress was often carried out without court approval. Today, some kind of court action is usually required, the main exception being certain tax authorities – such as HM Revenue and Customs in the United Kingdom and the Internal Revenue Service in the United States – and other agencies that retain the legal power to levy assets without a court order.

Proposition 2½ is a Massachusetts statute that limits property tax assessments and, secondarily, automobile excise tax levies by Massachusetts municipalities. The name of the initiative refers to the 2.5% ceiling on total property taxes annually as well as the 2.5% limit on property tax increases. It was passed by ballot measure, specifically called an initiative petition within Massachusetts state law for any form of referendum voting, in 1980 and went into effect in 1982. The effort to enact the proposition was led by the anti-tax group Citizens for Limited Taxation. It is similar to other "tax revolt" measures passed around the same time in other parts of the United States. This particular proposition followed the movements of states such as California.

Taxation in Ireland in 2017 came from Personal Income taxes, and Consumption taxes, being VAT and Excise and Customs duties. Corporation taxes represents most of the balance, but Ireland's Corporate Tax System (CT) is a central part of Ireland's economic model. Ireland summarises its taxation policy using the OECD's Hierarchy of Taxes pyramid, which emphasises high corporate tax rates as the most harmful types of taxes where economic growth is the objective. The balance of Ireland's taxes are Property taxes and Capital taxes.

Taxes in New Zealand are collected at a national level by the Inland Revenue Department (IRD) on behalf of the Government of New Zealand. National taxes are levied on personal and business income, and on the supply of goods and services. Capital gains tax applies in limited situations, such as the sale of some rental properties within 10 years of purchase. Some "gains" such as profits on the sale of patent rights are deemed to be income – income tax does apply to property transactions in certain circumstances, particularly speculation. There are currently no land taxes, but local property taxes (rates) are managed and collected by local authorities. Some goods and services carry a specific tax, referred to as an excise or a duty, such as alcohol excise or gaming duty. These are collected by a range of government agencies such as the New Zealand Customs Service. There is no social security (payroll) tax.

The Valuation Office Agency is a government body in England and Wales. It is an executive agency of His Majesty's Revenue and Customs.

A house in multiple occupation (HMO), or a house of multiple occupancy, is a British English term which refers to residential properties where 'common areas' exist and are shared by more than one household.

Business rates in England, or non-domestic rates, are a tax on the occupation of non-domestic property. Rates are a property tax with ancient roots that was formerly used to fund local services that was formalised with the Poor Law 1572 and superseded by the Poor Law of 1601. The Local Government Finance Act 1988 introduced business rates in England and Wales from 1990, repealing its immediate predecessor, the General Rate Act 1967. The act also introduced business rates in Scotland but as an amendment to the existing system, which had evolved separately to that in the rest of Great Britain. Since the establishment in 1997 of a Welsh Assembly able to pass legislation, the English and Welsh systems have been able to diverge. In 2015, business rates for Wales were devolved.

A mortgage loan or simply mortgage, in civil law jurisdicions known also as a hypothec loan, is a loan used either by purchasers of real property to raise funds to buy real estate, or by existing property owners to raise funds for any purpose while putting a lien on the property being mortgaged. The loan is "secured" on the borrower's property through a process known as mortgage origination. This means that a legal mechanism is put into place which allows the lender to take possession and sell the secured property to pay off the loan in the event the borrower defaults on the loan or otherwise fails to abide by its terms. The word mortgage is derived from a Law French term used in Britain in the Middle Ages meaning "death pledge" and refers to the pledge ending (dying) when either the obligation is fulfilled or the property is taken through foreclosure. A mortgage can also be described as "a borrower giving consideration in the form of a collateral for a benefit (loan)".

Tax assessment, or assessment, is the job of determining the value, and sometimes determining the use, of property, usually to calculate a property tax. This is usually done by an office called the assessor or tax assessor.

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property, multiplied by an assessment ratio, multiplied by a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other types of taxes. The property tax typically produces the required revenue for municipalities' tax levies. One disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

Taxes in Germany are levied by the federal government, the states (Länder) as well as the municipalities (Städte/Gemeinden). Many direct and indirect taxes exist in Germany; income tax and VAT are the most significant.

The parcel tax is a form of real estate tax. Unlike most real estate taxes or a land value tax, it is not directly based on property value. It funds K–12 public education and community facilities districts, which are usually known as "Mello-Roos" districts. The California parcel tax, in its typical form as a flat tax, is regressive.

The local property tax (LPT) is annual self-assessed tax charged on the market value of all residential properties in Ireland. It came into effect on 1 July 2013 and is collected by the Revenue Commissioners. The tax is assessed on residential properties. The owner of a property is liable. The revenue raised is used to fund the provision of services by local authorities and includes transfers between local authorities.

Rates are a tax on property in the United Kingdom used to fund local government. Business rates are collected throughout the United Kingdom. Domestic rates are collected in Northern Ireland and were collected in England and Wales before 1990 and in Scotland before 1989.