A land value tax (LVT) is a levy on the value of land without regard to buildings, personal property and other improvements. It is also known as a location value tax, a point valuation tax, a site valuation tax, split rate tax, or a site-value rating.

Council Tax is a local taxation system used in England, Scotland and Wales. It is a tax on domestic property, which was introduced in 1993 by the Local Government Finance Act 1992, replacing the short-lived Community Charge, which in turn replaced the domestic rates. Each property is assigned one of eight bands in England and Scotland, or nine bands in Wales, based on property value, and the tax is set as a fixed amount for each band. The more valuable the property, the higher the tax, except for properties valued above £320,000. Some property is exempt from the tax, and some people are exempt from the tax, while some get a discount.

A property tax or millage rate is an ad valorem tax on the value of a property.

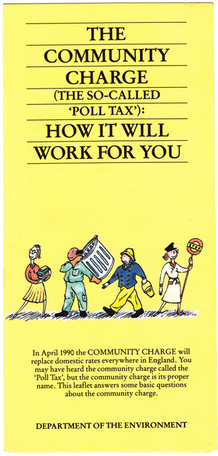

The Community Charge, commonly known as the poll tax, was a system of taxation introduced by Margaret Thatcher's government in replacement of domestic rates in Scotland from 1989, prior to its introduction in England and Wales from 1990. It provided for a single flat-rate, per-capita tax on every adult, at a rate set by the local authority. The charge was replaced by Council Tax in 1993, two years after its abolition was announced.

Rates are a type of property tax system in the United Kingdom, and in places with systems deriving from the British one, the proceeds of which are used to fund local government. Some other countries have taxes with a more or less comparable role, like France's taxe d'habitation.

Taxation in the United Kingdom may involve payments to at least three different levels of government: central government, devolved governments and local government. Central government revenues come primarily from income tax, National Insurance contributions, value added tax, corporation tax and fuel duty. Local government revenues come primarily from grants from central government funds, business rates in England, Council Tax and increasingly from fees and charges such as those for on-street parking. In the fiscal year 2014–15, total government revenue was forecast to be £648 billion, or 37.7 per cent of GDP, with net taxes and National Insurance contributions standing at £606 billion.

An ad valorem tax is a tax whose amount is based on the value of a transaction or of property. It is typically imposed at the time of a transaction, as in the case of a sales tax or value-added tax (VAT). An ad valorem tax may also be imposed annually, as in the case of a real or personal property tax, or in connection with another significant event. In some countries, a stamp duty is imposed as an ad valorem tax.

A Finance Act is the headline fiscal (budgetary) legislation enacted by the UK Parliament, containing multiple provisions as to taxes, duties, exemptions and reliefs at least once per year, and in particular setting out the principal tax rates for each fiscal year.

The Valuation Office Agency is a government body in England and Wales. It is an executive agency of His Majesty's Revenue and Customs.

Business rates in England, or non-domestic rates, are a tax on the occupation of non-domestic property. Rates are a property tax with ancient roots that was formerly used to fund local services that was formalised with the Poor Law 1572 and superseded by the Poor Law of 1601. The Local Government Finance Act 1988 introduced business rates in England and Wales from 1990, repealing its immediate predecessor, the General Rate Act 1967. The act also introduced business rates in Scotland but as an amendment to the existing system, which had evolved separately to that in the rest of Great Britain. Since the establishment in 1997 of a Welsh Assembly able to pass legislation, the English and Welsh systems have been able to diverge. In 2015, business rates for Wales were devolved.

In England and Wales the poor rate was a tax on property levied in each parish, which was used to provide poor relief. It was collected under both the Old Poor Law and the New Poor Law. It was absorbed into 'general rate' local taxation in the 1920s, and has continuity with the currently existing Council Tax.

Energy performance certificates (EPCs) are a rating scheme to summarise the energy efficiency of buildings. The building is given a rating between A - G (Inefficient), the EPC will also include tips the most cost effective ways to improve your homes energy rating. Energy performance certificates are used in many countries.

The Lyons Inquiry was an independent inquiry into the form, function and funding of local government in England. Appointed jointly by the Chancellor of the Exchequer and the Deputy Prime Minister in the summer of 2004, Sir Michael Lyons produced several reports over the next 3 years, culminating in a final report on the future of local government published alongside the Chancellor's Budget in March 2007.

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property times an assessment ratio times a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other taxes. The property tax typically produces the required revenue for municipalities' tax levies. A disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

Taxation in Norway is levied by the central government, the county municipality and the municipality. In 2012 the total tax revenue was 42.2% of the gross domestic product (GDP). Many direct and indirect taxes exist. The most important taxes – in terms of revenue – are VAT, income tax in the petroleum sector, employers' social security contributions and tax on "ordinary income" for persons. Most direct taxes are collected by the Norwegian Tax Administration and most indirect taxes are collected by the Norwegian Customs and Excise Authorities.

The history of taxation in the United Kingdom includes the history of all collections by governments under law, in money or in kind, including collections by monarchs and lesser feudal lords, levied on persons or property subject to the government, with the primary purpose of raising revenue.

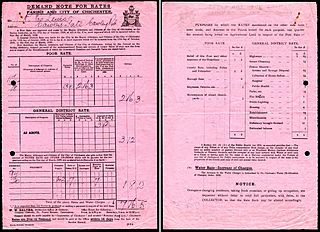

Rates are a tax on property in the United Kingdom used to fund local government. Business rates are collected throughout the United Kingdom. Domestic rates are collected in Northern Ireland and were collected in England and Wales before 1990 and in Scotland before 1989.

Business rates is the commonly used name of Non-Domestic Rates in Wales, a tax on occupation of non-domestic property. Rates are a property tax used to fund local services that date back to ancient times.

Taxation in Wales typically comprises payments to one or more of the three different levels of government: the UK government, the Welsh Government, and local government.