A tax is a compulsory financial charge or some other type of levy imposed on a taxpayer by a governmental organization in order to collectively fund government spending, public expenditures, or as a way to regulate and reduce negative externalities. Tax compliance refers to policy actions and individual behaviour aimed at ensuring that taxpayers are paying the right amount of tax at the right time and securing the correct tax allowances and tax relief. The first known taxation took place in Ancient Egypt around 3000–2800 BC. Taxes consist of direct or indirect taxes and may be paid in money or as its labor equivalent.

A land value tax (LVT) is a levy on the value of land without regard to buildings, personal property and other improvements upon it. It is also known as a location value tax, a point valuation tax, a site valuation tax, split rate tax, or a site-value rating.

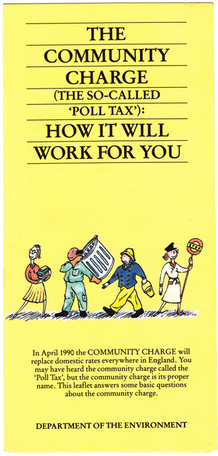

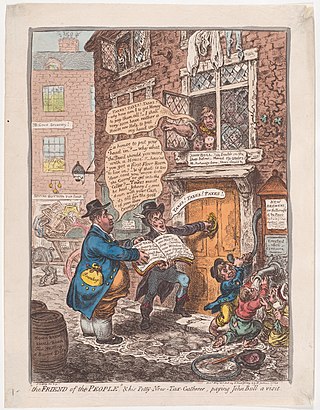

The Community Charge, commonly known as the poll tax, was a system of taxation introduced by Margaret Thatcher's government in replacement of domestic rates in Scotland from 1989, prior to its introduction in England and Wales from 1990. It provided for a single flat-rate, per-capita tax on every adult, at a rate set by the local authority. The charge was replaced by Council Tax in 1993, two years after its abolition was announced.

Corporation tax in the United Kingdom is a corporate tax levied in on the profits made by UK-resident companies and on the profits of entities registered overseas with permanent establishments in the UK.

In Canada, taxation is a prerogative shared between the federal government and the various provincial and territorial legislatures.

In the United Kingdom, taxation may involve payments to at least three different levels of government: central government, devolved governments and local government. Central government revenues come primarily from income tax, National Insurance contributions, value added tax, corporation tax and fuel duty. Local government revenues come primarily from grants from central government funds, business rates in England, Council Tax and increasingly from fees and charges such as those for on-street parking. In the fiscal year 2014–15, total government revenue was forecast to be £648 billion, or 37.7 per cent of GDP, with net taxes and National Insurance contributions standing at £606 billion.

An ad valorem tax is a tax whose amount is based on the value of a transaction or of a property. It is typically imposed at the time of a transaction, as in the case of a sales tax or value-added tax (VAT). An ad valorem tax may also be imposed annually, as in the case of a real or personal property tax, or in connection with another significant event. In some countries, a stamp duty is imposed as an ad valorem tax.

A Finance Act is the headline fiscal (budgetary) legislation enacted by the UK Parliament, containing multiple provisions as to taxes, duties, exemptions and reliefs at least once per year, and in particular setting out the principal tax rates for each fiscal year.

The Russian Tax Code is the primary tax law for the Russian Federation. The Code was created, adopted and implemented in three stages.

Business rates in England, or non-domestic rates, are a tax on the occupation of non-domestic property. Rates are a property tax with ancient roots that was formerly used to fund local services that was formalised with the Vagabonds Act 1572 and superseded by the Poor Relief Act 1601. The Local Government Finance Act 1988 introduced business rates in England and Wales from 1990, repealing its immediate predecessor, the General Rate Act 1967. The act also introduced business rates in Scotland but as an amendment to the existing system, which had evolved separately to that in the rest of Great Britain. Since the establishment in 1997 of a Welsh Assembly able to pass legislation, the English and Welsh systems have been able to diverge. In 2015, business rates for Wales were devolved.

The Tanzania Revenue Authority (TRA) is the government agency of Tanzania, charged with the responsibility of managing the assessment, collection and accounting of all central government revenue in Tanzania.

Business rates is the commonly used name of Non-Domestic Rates in Scotland, a tax on occupation of non-domestic property. Rates are a property tax used to fund local services that dates back to the Poor Law.

The Lyons Inquiry was an independent inquiry into the form, function and funding of local government in England. Appointed jointly by the Chancellor of the Exchequer and the Deputy Prime Minister in the summer of 2004, Sir Michael Lyons produced several reports over the next 3 years, culminating in a final report on the future of local government published alongside the Chancellor's Budget in March 2007.

Taxation in Norway is levied by the central government, the county municipality and the municipality. In 2012 the total tax revenue was 42.2% of the gross domestic product (GDP). Many direct and indirect taxes exist. The most important taxes – in terms of revenue – are VAT, income tax in the petroleum sector, employers' social security contributions and tax on "ordinary income" for persons. Most direct taxes are collected by the Norwegian Tax Administration and most indirect taxes are collected by the Norwegian Customs and Excise Authorities.

The history of taxation in the United Kingdom includes the history of all collections by governments under law, in money or in kind, including collections by monarchs and lesser feudal lords, levied on persons or property subject to the government, with the primary purpose of raising revenue.

The policy of taxation in the Philippines is governed chiefly by the Constitution of the Philippines and three Republic Acts.

Taxation in Bhutan is conducted by the national government and by its subsidiary local governments. All taxation is ultimately overseen by the Bhutan Ministry of Finance, Department of Revenue and Customs, which is part of the executive Lhengye Zhungtshog (cabinet). The modern legal basis for taxation in Bhutan derives from legislation. Several acts provide for taxation and enforcement only germane to their subject matter and at various levels of government, while a smaller number provide more comprehensive substantive tax law. As a result, the tax scheme of Bhutan is highly decentralized.

Fiscal policy are "measures employed by governments to stabilize the economy, specifically by manipulating the levels and allocations of taxes and government expenditures". In the Philippines, this is characterized by continuous and increasing levels of debt and budget deficits, though there were improvements in the last few years of the first decade of the 21st century.

Rates are a tax on property in the United Kingdom used to fund local government. Business rates are collected throughout the United Kingdom. Domestic rates are collected in Northern Ireland and were collected in England and Wales before 1990 and in Scotland before 1989.

Taxation in Wales typically comprises payments to one or more of the three different levels of government: the UK government, the Welsh Government, and local government.