A variety of measures of national income and output are used in economics to estimate total economic activity in a country or region, including gross domestic product (GDP), gross national product (GNP), net national income (NNI), and adjusted national income. All are specially concerned with counting the total amount of goods and services produced within the economy and by various sectors. The boundary is usually defined by geography or citizenship, and it is also defined as the total income of the nation and also restrict the goods and services that are counted. For instance, some measures count only goods & services that are exchanged for money, excluding bartered goods, while other measures may attempt to include bartered goods by imputing monetary values to them.

In accounting, fixed capital is any kind of real, physical asset that is used repeatedly in the production of a product. In economics, fixed capital is a type of capital good that as a real, physical asset is used as a means of production which is durable or isn't fully consumed in a single time period. It contrasts with circulating capital such as raw materials, operating expenses etc.

In accountancy, depreciation is a term that refers to two aspects of the same concept: first, an actual reduction in the fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wears, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used.

Stock valuation is the method of calculating theoretical values of companies and their stocks. The main use of these methods is to predict future market prices, or more generally, potential market prices, and thus to profit from price movement – stocks that are judged undervalued are bought, while stocks that are judged overvalued are sold, in the expectation that undervalued stocks will overall rise in value, while overvalued stocks will generally decrease in value. A target price is a price at which an analyst believes a stock to be fairly valued relative to its projected and historical earnings.

Fixed investment in economics is the purchasing of newly produced fixed capital. It is measured as a flow variable – that is, as an amount per unit of time.

In financial accounting, free cash flow (FCF) or free cash flow to firm (FCFF) is the amount by which a business's operating cash flow exceeds its working capital needs and expenditures on fixed assets. It is that portion of cash flow that can be extracted from a company and distributed to creditors and securities holders without causing issues in its operations. As such, it is an indicator of a company's financial flexibility and is of interest to holders of the company's equity, debt, preferred stock and convertible securities, as well as potential lenders and investors.

Capital accumulation is the dynamic that motivates the pursuit of profit, involving the investment of money or any financial asset with the goal of increasing the initial monetary value of said asset as a financial return whether in the form of profit, rent, interest, royalties or capital gains. The aim of capital accumulation is to create new fixed and working capitals, broaden and modernize the existing ones, grow the material basis of social-cultural activities, as well as constituting the necessary resource for reserve and insurance. The process of capital accumulation forms the basis of capitalism, and is one of the defining characteristics of a capitalist economic system.

Economics, business, accounting, and related fields often distinguish between quantities that are stocks and those that are flows. These differ in their units of measurement. A stock is measured at one specific time, and represents a quantity existing at that point in time, which may have accumulated in the past. A flow variable is measured over an interval of time. Therefore, a flow would be measured per unit of time. Flow is roughly analogous to rate or speed in this sense.

Consumption of fixed capital (CFC) is a term used in business accounts, tax assessments and national accounts for depreciation of fixed assets. CFC is used in preference to "depreciation" to emphasize that fixed capital is used up in the process of generating new output, and because unlike depreciation it is not valued at historic cost but at current market value ; CFC may also include other expenses incurred in using or installing fixed assets beyond actual depreciation charges. Normally the term applies only to producing enterprises, but sometimes it applies also to real estate assets.

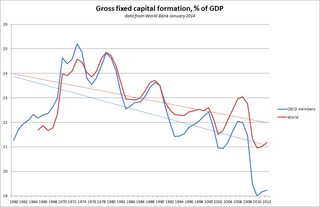

Gross fixed capital formation (GFCF) is a component of the expenditure on gross domestic product (GDP) that indicates how much of the new value added in an economy is invested rather than consumed. It measures the value of acquisitions of new or existing fixed assets by the business sector, governments, and "pure" households minus disposals of fixed assets.

Operating surplus is an accounting concept used in national accounts statistics and in corporate and government accounts. It is the balancing item of the Generation of Income Account in the UNSNA. It may be used in macro-economics as a proxy for total pre-tax profit income, although entrepreneurial income may provide a better measure of business profits. According to the 2008 SNA, it is the measure of the surplus accruing from production before deducting property income, e.g., land rent and interest.

Capital formation is a concept used in macroeconomics, national accounts and financial economics. Occasionally it is also used in corporate accounts. It can be defined in three ways:

Cash-flow return on investment (CFROI) is a valuation model that assumes the stock market sets prices based on cash flow, not on corporate performance and earnings.

The following outline is provided as an overview of and topical guide to finance:

In finance, the T-model is a formula that states the returns earned by holders of a company's stock in terms of accounting variables obtainable from its financial statements. The T-model connects fundamentals with investment return, allowing an analyst to make projections of financial performance and turn those projections into a required return that can be used in investment selection.

In financial accounting, an asset is any resource owned or controlled by a business or an economic entity. It is anything that can be used to produce positive economic value. Assets represent value of ownership that can be converted into cash . The balance sheet of a firm records the monetary value of the assets owned by that firm. It covers money and other valuables belonging to an individual or to a business. Total assets can also be called the balance sheet total.

A financial ratio or accounting ratio states the relative magnitude of two selected numerical values taken from an enterprise's financial statements. Often used in accounting, there are many standard ratios used to try to evaluate the overall financial condition of a corporation or other organization. Financial ratios may be used by managers within a firm, by current and potential shareholders (owners) of a firm, and by a firm's creditors. Financial analysts use financial ratios to compare the strengths and weaknesses in various companies. If shares in a company are traded in a financial market, the market price of the shares is used in certain financial ratios.

In macroeconomics, investment "consists of the additions to the nation's capital stock of buildings, equipment, software, and inventories during a year" or, alternatively, investment spending — "spending on productive physical capital such as machinery and construction of buildings, and on changes to inventories — as part of total spending" on goods and services per year.

This glossary of economics is a list of definitions of terms and concepts used in economics, its sub-disciplines, and related fields.