Related Research Articles

Milton Friedman was an American economist and statistician who received the 1976 Nobel Memorial Prize in Economic Sciences for his research on consumption analysis, monetary history and theory and the complexity of stabilization policy. With George Stigler and others, Friedman was among the intellectual leaders of the Chicago school of economics, a neoclassical school of economic thought associated with the work of the faculty at the University of Chicago that rejected Keynesianism in favor of monetarism until the mid-1970s, when it turned to new classical macroeconomics heavily based on the concept of rational expectations. Several students, young professors and academics who were recruited or mentored by Friedman at Chicago went on to become leading economists, including Gary Becker, Robert Fogel, Thomas Sowell and Robert Lucas Jr.

Monetarism is a school of thought in monetary economics that emphasizes the role of governments in controlling the amount of money in circulation. Monetarist theory asserts that variations in the money supply have major influences on national output in the short run and on price levels over longer periods. Monetarists assert that the objectives of monetary policy are best met by targeting the growth rate of the money supply rather than by engaging in discretionary monetary policy. Monetarism is commonly associated with neoliberalism.

Monetary economics is the branch of economics that studies the different theories of money: it provides a framework for analyzing money and considers its functions, and it considers how money can gain acceptance purely because of its convenience as a public good. The discipline has historically prefigured, and remains integrally linked to, macroeconomics. This branch also examines the effects of monetary systems, including regulation of money and associated financial institutions and international aspects.

The causes of the Great Depression in the early 20th century in the United States have been extensively discussed by economists and remain a matter of active debate. They are part of the larger debate about economic crises and recessions. The specific economic events that took place during the Great Depression are well established.

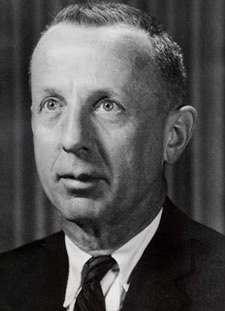

Roy Archibald Young was an American banker who served as the 4th chairman of the Federal Reserve from 1927 to 1930. During his tenure as chairman, the Wall Street Crash of 1929 occurred, which signaled the beginning of the Great Depression. Before and after his term at the Federal Reserve Board, Young also served as the president of the Federal Reserve Bank of Minneapolis from 1919 to 1927 and Federal Reserve Bank of Boston from 1930 to 1942.

Eugene Isaac Meyer was an American financier and newspaper publisher. Through his public career, he served as the 5th chairman of the Federal Reserve from 1930 to 1933 and was the first president of the World Bank Group from June to December 1946. Meyer published The Washington Post from 1933 to 1946, and the paper stayed in his family throughout the rest of the 20th century.

This history of central banking in the United States encompasses various bank regulations, from early wildcat banking practices through the present Federal Reserve System.

The Federal Reserve System has faced various criticisms since it was authorized in 1913. Nobel laureate economist Milton Friedman and his fellow monetarist Anna Schwartz criticized the Fed's response to the Wall Street Crash of 1929 arguing that it greatly exacerbated the Great Depression. More recent prominent critics include former Congressman Ron Paul.

Charles Poor Kindleberger was an American economic historian and author of over 30 books. His 1978 book Manias, Panics, and Crashes, about speculative stock market bubbles, was reprinted in 2000 after the dot-com bubble. He is well known for his role in developing what would become hegemonic stability theory, arguing that a hegemonic power was needed to maintain a stable international monetary system. He has been referred to as "the master of the genre" on financial crisis by The Economist.

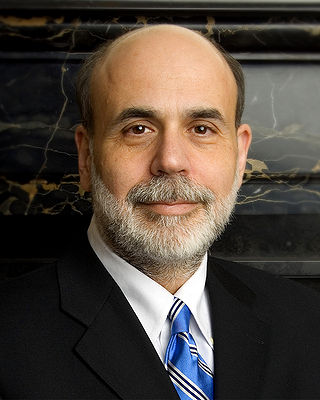

Ben Shalom Bernanke is an American economist who served as the 14th chairman of the Federal Reserve from 2006 to 2014. After leaving the Federal Reserve, he was appointed a distinguished fellow at the Brookings Institution. During his tenure as chairman, Bernanke oversaw the Federal Reserve's response to the late-2000s financial crisis, for which he was named the 2009 Time Person of the Year. Before becoming Federal Reserve chairman, Bernanke was a tenured professor at Princeton University and chaired the department of economics there from 1996 to September 2002, when he went on public service leave. Bernanke was awarded the 2022 Nobel Memorial Prize in Economic Sciences, jointly with Douglas Diamond and Philip H. Dybvig, "for research on banks and financial crises", more specifically for his analysis of the Great Depression.

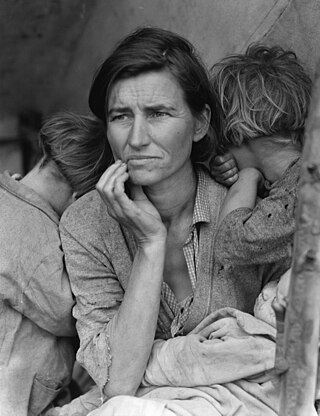

In the United States, the Great Depression began with the Wall Street Crash of October 1929 and then spread worldwide. The nadir came in 1931–1933, and recovery came in 1940. The stock market crash marked the beginning of a decade of high unemployment, poverty, low profits, deflation, plunging farm incomes, and lost opportunities for economic growth as well as for personal advancement. Altogether, there was a general loss of confidence in the economic future.

Anna Jacobson Schwartz was an American economist who worked at the National Bureau of Economic Research in New York City and a writer for The New York Times. Paul Krugman has said that Schwartz is "one of the world's greatest monetary scholars."[1]

A Monetary History of the United States, 1867–1960 is a book written in 1963 by Nobel Prize–winning economist Milton Friedman and Anna J. Schwartz. It uses historical time series and economic analysis to argue the then-novel proposition that changes in the money supply profoundly influenced the U.S. economy, especially the behavior of economic fluctuations. The implication they draw is that changes in the money supply had unintended adverse effects, and that sound monetary policy is necessary for economic stability. Orthodox economic historians see it as one of the most influential economics books of the century. The chapter dealing with the causes of the Great Depression was published as a stand-alone book titled The Great Contraction, 1929–1933.

Debt deflation is a theory that recessions and depressions are due to the overall level of debt rising in real value because of deflation, causing people to default on their consumer loans and mortgages. Bank assets fall because of the defaults and because the value of their collateral falls, leading to a surge in bank insolvencies, a reduction in lending and by extension, a reduction in spending.

The Great Depression (1929–1939) was an economic shock that impacted most countries across the world. It was a period of economic depression that became evident after a major fall in stock prices in the United States. The economic contagion began around September 1929 and led to the Wall Street stock market crash of October 24. It was the longest, deepest, and most widespread depression of the 20th century.

The Depression of 1920–1921 was a sharp deflationary recession in the United States, United Kingdom and other countries, beginning 14 months after the end of World War I. It lasted from January 1920 to July 1921. The extent of the deflation was not only large, but large relative to the accompanying decline in real product.

In economics, stimulus refers to attempts to use monetary policy or fiscal policy to stimulate the economy. Stimulus can also refer to monetary policies such as lowering interest rates and quantitative easing.

The Panic of 1930 was a financial crisis that occurred in the United States which led to a severe decline in the money supply during a period of declining economic activity. A series of bank failures from agricultural areas during this time period sparked panic among depositors which led to widespread bank runs across the country.

Michael David Bordo is a Canadian and American economist, currently Board of Governors Professor of Economics and Distinguished Professor of Economics at Rutgers University. He is a research associate at the National Bureau of Economic Research as well as a Distinguished Visiting Fellow at the Hoover Institution at Stanford University. He is the third most influential economic historian worldwide according to the RePEc/IDEAS rankings. He was a student of Milton Friedman and has co-authored numerous books and articles with Anna Schwartz.

The real bills doctrine says that as long as bankers lend to businessmen only against the security (collateral) of short-term 30-, 60-, or 90-day commercial paper representing claims to real goods in the process of production, the loans will be just sufficient to finance the production of goods. The doctrine seeks to have real output determine its own means of purchase without affecting prices. Under the real bills doctrine, there is only one policy role for the central bank: lending commercial banks the necessary reserves against real customer bills, which the banks offer as collateral. The term "real bills doctrine" was coined by Lloyd Mints in his 1945 book, A History of Banking Theory. The doctrine was previously known as "the commercial loan theory of banking".

References

- 1 2 3 Milton Friedman; Anna Schwartz (2008). The Great Contraction, 1929–1933 (New ed.). Princeton University Press. ISBN 978-0691137940.

- ↑ Ben S. Bernanke (Nov. 8, 2002), Federal Reserve Board Speech: "Remarks by Governor Ben S. Bernanke", Conference to Honor Milton Friedman, University of Chicago

| | This economic history-related article is a stub. You can help Wikipedia by expanding it. |

| | This article about a book on economics or finance is a stub. You can help Wikipedia by expanding it. |