A debit card is a payment card that can be used in place of cash to make purchases. It is similar to a credit card, but unlike a credit card, the money for the purchase must be in the cardholder's bank account at the time of a purchase and is immediately transferred directly from that account to the merchant's account to pay for the purchase.

Electronic funds transfer at point of sale is an electronic payment system involving electronic funds transfers based on the use of payment cards, such as debit or credit cards, at payment terminals located at points of sale. EFTPOS technology was developed during the 1980s. In Australia and New Zealand, it is also the brand name of a specific system used for such payments; these systems are mainly country-specific and do not interconnect. In Singapore, it is known as NETS.

A smart card, chip card, or integrated circuit card is a physical electronic authorization device, used to control access to a resource. It is typically a plastic credit card-sized card with an embedded integrated circuit (IC) chip. Many smart cards include a pattern of metal contacts to electrically connect to the internal chip. Others are contactless, and some are both. Smart cards can provide personal identification, authentication, data storage, and application processing. Applications include identification, financial, mobile phones (SIM), public transit, computer security, schools, and healthcare. Smart cards may provide strong security authentication for single sign-on (SSO) within organizations. Numerous nations have deployed smart cards throughout their populations.

A stored-value card (SVC) is a payment card with a monetary value stored on the card itself, not in an external account maintained by a financial institution. This means no network access is required by the payment collection terminals as funds can be withdrawn and deposited straight from the card. Like cash, payment cards can be used anonymously as the person holding the card can use the funds. They are an electronic development of token coins and are typically used in low-value payment systems or where network access is difficult or expensive to implement, such as parking machines, public transport systems, closed payment systems in locations such as ships or within companies.

Mastercard Inc. is an American multinational financial services corporation headquartered in the Mastercard International Global Headquarters in Purchase, New York. The Global Operations Headquarters is located in O'Fallon, Missouri, a municipality of St. Charles County, Missouri. Throughout the world, its principal business is to process payments between the banks of merchants and the card-issuing banks or credit unions of the purchasers who use the "Mastercard" brand debit, credit and prepaid cards to make purchases. Mastercard Worldwide has been a publicly traded company since 2006. Prior to its initial public offering, Mastercard Worldwide was a cooperative owned by the more than 25,000 financial institutions that issue its branded cards.

Interac is a Canadian interbank network that links financial institutions and other enterprises for the purpose of exchanging electronic financial transactions. Interac serves as the Canadian debit card system and the predominant funds transfer network via its e-Transfer service. There are over 59,000 automated teller machines that can be accessed through the Interac network in Canada, and over 450,000 merchant locations accepting Interac debit payments.

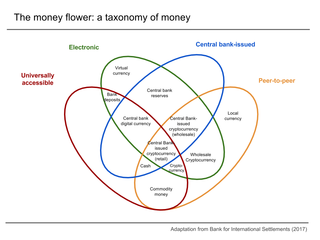

Digital currency is any currency, money, or money-like asset that is primarily managed, stored or exchanged on digital computer systems, especially over the internet. Types of digital currencies include cryptocurrency, virtual currency and central bank digital currency. Digital currency may be recorded on a distributed database on the internet, a centralized electronic computer database owned by a company or bank, within digital files or even on a stored-value card.

Mondex was a smart card electronic cash system, implemented as a stored-value card owned by Mastercard.

An e-commerce payment system facilitates the acceptance of electronic payment for offline transfer, also known as a subcomponent of electronic data interchange (EDI), e-commerce payment systems have become increasingly popular due to the widespread use of the internet-based shopping and banking.

Verifone is an American multinational corporation headquartered in Coral Springs, Florida, that provides technology for electronic payment transactions and value-added services at the point-of-sale. Verifone sells merchant-operated, consumer-facing and self-service payment systems to the financial, retail, hospitality, petroleum, government and healthcare industries. The company's products consist of POS electronic payment devices that run its own operating systems, security and encryption software, and certified payment software, and that are designed for both consumer-facing and unattended environments.

A payment is the voluntary tender of money or its equivalent or of things of value by one party to another in exchange for goods, or services provided by them, or to fulfill a legal obligation. The party making the payment is commonly called the payer, while the payee is the party receiving the payment.

Payment cards are part of a payment system issued by financial institutions, such as a bank, to a customer that enables its owner to access the funds in the customer's designated bank accounts, or through a credit account and make payments by electronic transfer and access automated teller machines (ATMs). Such cards are known by a variety of names including bank cards, ATM cards, client cards, key cards or cash cards.

3-D Secure is a protocol designed to be an additional security layer for online credit and debit card transactions. The name refers to the "three domains" which interact using the protocol: the merchant/acquirer domain, the issuer domain, and the interoperability domain.

Merchant Account Providers give businesses the ability to accept debit and credit cards in payment for goods and services. This can be face-to-face, on the telephone, or over the internet.

Gemalto was an international digital security company providing software applications, secure personal devices such as smart cards and tokens, and managed services. It was formed in June 2006 by the merger of two companies, Axalto and Gemplus International. Gemalto N.V.'s revenue in 2018 was €2.969 billion.

Network for Electronic Transfers, colloquially known as NETS, is a Singaporean electronic payment service provider. Founded in 1985, by a consortium of local banks, it aims to establish the debit network and drive the adoption of electronic payments in Singapore. It is owned by DBS Bank, OCBC Bank and United Overseas Bank (UOB).

Contactless payment systems are credit cards and debit cards, key fobs, smart cards, or other devices, including smartphones and other mobile devices, that use radio-frequency identification (RFID) or near-field communication for making secure payments. The embedded integrated circuit chip and antenna enable consumers to wave their card, fob, or handheld device over a reader at the point of sale terminal. Contactless payments are made in close physical proximity, unlike other types of mobile payments which use broad-area cellular or WiFi networks and do not involve close physical proximity.

A credit card is a payment card issued to users (cardholders) to enable the cardholder to pay a merchant for goods and services based on the cardholder's accrued debt. The card issuer creates a revolving account and grants a line of credit to the cardholder, from which the cardholder can borrow money for payment to a merchant or as a cash advance. There are two credit card groups: consumer credit cards and business credit cards. Most cards are plastic, but some are metal cards, and a few gemstone-encrusted metal cards.

A payment processor is a system that enables financial transactions, commonly employed by a merchant, to handle transactions with customers from various channels such as credit cards and debit cards or bank accounts. They are usually broken down into two types: front-end and back-end.

Atom TechnologiesLimited is a payment services provider company, headquartered in Mumbai, India. Atom was started in 2006 as a subsidiary of the Financial Technologies Group, founded by Jignesh Shah.