Related Research Articles

A flat tax is a tax with a single rate on the taxable amount, after accounting for any deductions or exemptions from the tax base. It is not necessarily a fully proportional tax. Implementations are often progressive due to exemptions, or regressive in case of a maximum taxable amount. There are various tax systems that are labeled "flat tax" even though they are significantly different. The defining characteristic is the existence of only one tax rate other than zero, as opposed to multiple non-zero rates that vary depending on the amount subject to taxation.

A special-purpose local-option sales tax (SPLOST) is a financing method for funding capital outlay projects in the U.S. state of Georgia. It is an optional 1% sales tax levied by any county for the purpose of funding the building of parks, schools, roads, and other public facilities. The revenue generated cannot be used towards operating expenses or most maintenance projects.

The mill or mil is a unit of currency, used in several countries as one-thousandth of the base unit. In the United States, it is a notional unit equivalent to a thousandth of a United States dollar. In the United Kingdom, it was proposed during the decades of discussion on decimalisation as a 1⁄1000 division of sterling's pound. While this system was never adopted in the United Kingdom, the currencies of some British or formerly British territories did adopt it, such as the Palestine pound and the Maltese lira.

Proposition 13 is an amendment of the Constitution of California enacted during 1978, by means of the initiative process. The initiative was approved by California voters on June 6, 1978. It was upheld as constitutional by the United States Supreme Court in the case of Nordlinger v. Hahn, 505 U.S. 1 (1992). Proposition 13 is embodied in Article XIII A of the Constitution of the State of California.

A property tax is an ad valorem tax on the value of a property.

An ad valorem tax is a tax whose amount is based on the value of a transaction or of a property. It is typically imposed at the time of a transaction, as in the case of a sales tax or value-added tax (VAT). An ad valorem tax may also be imposed annually, as in the case of a real or personal property tax, or in connection with another significant event. In some countries, a stamp duty is imposed as an ad valorem tax.

Tax increment financing (TIF) is a public financing method that is used as a subsidy for redevelopment, infrastructure, and other community-improvement projects in many countries, including the United States. The original intent of a TIF program is to stimulate private investment in a blighted area that has been designated to be in need of economic revitalization. Similar or related value capture strategies are used around the world.

A consumption tax is a tax levied on consumption spending on goods and services. The tax base of such a tax is the money spent on consumption. Consumption taxes are usually indirect, such as a sales tax or a value-added tax. However, a consumption tax can also be structured as a form of direct, personal taxation, such as the Hall–Rabushka flat tax.

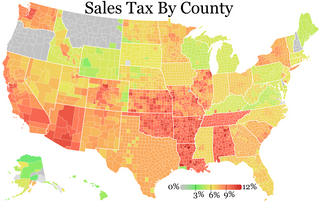

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. 45 states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

A hotel tax or lodging tax is charged in most of the United States, to travelers when they rent accommodations in a hotel, inn, tourist home or house, motel, or other lodging, generally unless the stay is for a period of 30 days or more. In addition to sales tax, it is collected when payment is made for the accommodation, and it is then remitted by the lodging operator to the city or county. It can also be called hotel occupancy tax in places like New York City and Texas. Despite its name, it generally applies to the same range of accommodations.

Proposition 218 is an adopted initiative constitutional amendment which revolutionized local and regional government finance and taxation in California. Named the "Right to Vote on Taxes Act," it was sponsored by the Howard Jarvis Taxpayers Association as a constitutional follow-up to the landmark property tax reduction initiative constitutional amendment, Proposition 13, approved in June 1978. Proposition 218 was approved and adopted by California voters during the November 5, 1996, statewide general election.

In the United States, a special assessment is a charge that public authorities can assess against real estate parcels for certain public projects. This charge is levied in a specific geographic area known as a special assessment district (SAD). A special assessment may only be levied against parcels of real estate which have been identified as having received a direct and unique "benefit" from the public project.

The School Infrastructure Local Option (SILO) is a 1% local option sales tax adopted on a county by county basis in Iowa, United States. Although the tax is collected by county, state mandate says the total amount collected is to be pooled and shared between the school districts. SILO was developed in 1998 by the Iowa General Assembly to give school districts a revenue options other than the property tax. The tax can be enacted for up to 10 years at a time. As of late 2005, only Linn and Johnson counties in Iowa had not enacted a SILO tax. In the spring of 2006 the Iowa legislature encouraged the two remaining counties to join the other 97 counties which had enacted this tax by offering an incentive provided the tax was enacted by July 1, 2008, allowing the districts to keep 100% of the money generated for the first half of the time it is collected instead of pooling it statewide. A vote was scheduled in both counties for February 13, 2007 where it was approved, 58% to 42% in Linn County and 67% to 33% in Johnson County. The tax for both counties went into effect on July 1, 2007 for a period of 10 years, making it a statewide tax. Iowa currently has a 6% state sales tax rate in addition to the 1% SILO tax and any other Local Option Sales Taxes (LOST) which may be in effect in each county, often an additional 1%.

An excise, or excise tax, is any duty on manufactured goods that is normally levied at the moment of manufacture for internal consumption rather than at sale. Excises are often associated with customs duties, which are levied on pre-existing goods when they cross a designated border in a specific direction; customs are levied on goods that become taxable items at the border, while excise is levied on goods that came into existence inland.

The U.S. state of New Jersey levies a state personal income tax and state corporate income tax and a state sales tax. Property taxes are also levied by municipalities, counties, and school districts.

Measure R was a ballot measure during the November 2008 elections in Los Angeles County, California, that proposed a half-cent sales taxes increase on each dollar of taxable sales for thirty years in order to pay for transportation projects and improvements. The measure was approved by voters with 67.22% of the vote, just over the two-thirds majority required by the state of California to raise local taxes. The project was touted as a way to "improve the environment by getting more Angelenos out of their cars and into the region's growing subway, light rail, and bus services." It will result in the construction or expansion of a dozen rail lines in the county.

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property, multiplied by an assessment ratio, multiplied by a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other types of taxes. The property tax typically produces the required revenue for municipalities' tax levies. One disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

Taxes in California are collected by state and local governments through a number of tax categories.

Colorado Amendment 64 was a successful popular initiative ballot measure to amend the Constitution of the State of Colorado, outlining a statewide drug policy for cannabis. The measure passed on November 6, 2012, and along with a similar measure in Washington state, marked "an electoral first not only for America but for the world."

Proposition 218 is an adopted initiative constitutional amendment in the state of California that appeared on the November 5, 1996, statewide election ballot. Proposition 218 revolutionized local and regional government finance in California. Called the “Right to Vote on Taxes Act,” Proposition 218 was sponsored by the Howard Jarvis Taxpayers Association as a constitutional follow-up to the landmark Proposition 13 property tax revolt initiative constitutional amendment approved by California voters on June 6, 1978. Proposition 218 was drafted by constitutional attorneys Jonathan Coupal and Jack Cohen.

References

- ↑ "What is the 'regular' local option sales tax (LOST)? | Iowa Department Of Revenue". tax.iowa.gov. Retrieved 2022-11-18.

- ↑ Brunori, David (2019-07-26). Local Tax Policy: A Primer. Rowman & Littlefield. p. 70. ISBN 978-1-5381-3117-6.

| | This tax-related article is a stub. You can help Wikipedia by expanding it. |