Debt is an obligation that requires one party, the debtor, to pay money borrowed or otherwise withheld from another party, the creditor. Debt may be owed by sovereign state or country, local government, company, or an individual. Commercial debt is generally subject to contractual terms regarding the amount and timing of repayments of principal and interest. Loans, bonds, notes, and mortgages are all types of debt. In financial accounting, debt is a type of financial transaction, as distinct from equity.

A reverse mortgage is a mortgage loan, usually secured by a residential property, that enables the borrower to access the unencumbered value of the property. The loans are typically promoted to older homeowners and typically do not require monthly mortgage payments. Borrowers are still responsible for property taxes or homeowner's insurance. Reverse mortgages allow older people to immediately access the home equity they have built up in their homes, and defer payment of the loan until they die, sell, or move out of the home. Because there are no required mortgage payments on a reverse mortgage, the interest is added to the loan balance each month. The rising loan balance can eventually grow to exceed the value of the home, particularly in times of declining home values or if the borrower continues to live in the home for many years. However, the borrower is generally not required to repay any additional loan balance in excess of the value of the home.

In economics, consumer debt is the amount owed by consumers. It includes debts incurred on purchase of goods that are consumable and/or do not appreciate. In macroeconomic terms, it is debt which is used to fund consumption rather than investment.

Household debt is the combined debt of all people in a household, including consumer debt and mortgage loans. A significant rise in the level of this debt coincides historically with many severe economic crises and was a cause of the U.S. and subsequent European economic crises of 2007–2012. Several economists have argued that lowering this debt is essential to economic recovery in the U.S. and selected Eurozone countries.

Lenders mortgage insurance (LMI), also known as private mortgage insurance (PMI) in the US, is insurance payable to a lender or trustee for a pool of securities that may be required when taking out a mortgage loan. It is insurance to offset losses in the case where a mortgagor is not able to repay the loan and the lender is not able to recover its costs after foreclosure and sale of the mortgaged property. Typical rates are $55/mo. per $100,000 financed, or as high as $125/mo. for a typical $200,000 loan.

Real estate economics is the application of economic techniques to real estate markets. It tries to describe, explain, and predict patterns of prices, supply, and demand. The closely related field of housing economics is narrower in scope, concentrating on residential real estate markets, while the research on real estate trends focuses on the business and structural changes affecting the industry. Both draw on partial equilibrium analysis, urban economics, spatial economics, basic and extensive research, surveys, and finance.

Canada Mortgage and Housing Corporation is Canada's federal crown corporation responsible for administering the National Housing Act, with the mandate to improve housing by living conditions in the country.

The loan-to-value (LTV) ratio is a financial term used by lenders to express the ratio of a loan to the value of an asset purchased.

A real-estate bubble or property bubble is a type of economic bubble that occurs periodically in local or global real estate markets, and it typically follows a land boom. A land boom is a rapid increase in the market price of real property such as housing until they reach unsustainable levels and then declines. This period, during the run-up to the crash, is also known as froth. The questions of whether real estate bubbles can be identified and prevented, and whether they have broader macroeconomic significance, are answered differently by schools of economic thought, as detailed below.

In the United States, a conforming loan is a mortgage loan that both meets the underwriting guidelines of Fannie Mae and Freddie Mac and that does not exceed the conforming loan limit. The most well-known guideline is the size of the loan which, for 2022, was generally limited to $647,200 for one-unit single family homes in the continental US. Other guidelines include borrower's loan-to-value ratio, debt-to-income ratio, credit score and history, documentation requirements, etc.

In the consumer mortgage industry, debt-to-income ratio is the percentage of a consumer's monthly gross income that goes toward paying debts. There are two main kinds of DTI, as discussed below.

This article gives descriptions of mortgage terminology in the United Kingdom.

Affordable housing is housing which is deemed affordable to those with a household income at or below the median as rated by the national government or a local government by a recognized housing affordability index. Most of the literature on affordable housing refers to mortgages and a number of forms that exist along a continuum – from emergency homeless shelters, to transitional housing, to non-market rental, to formal and informal rental, indigenous housing, and ending with affordable home ownership.

Real estate investing involves the purchase, management and sale or rental of real estate for profit. Someone who actively or passively invests in real estate is called a real estate entrepreneur or a real estate investor. Some investors actively develop, improve or renovate properties to make more money from them.

A mortgage loan or simply mortgage, in civil law jurisdicions known also as a hypothec loan, is a loan used either by purchasers of real property to raise funds to buy real estate, or by existing property owners to raise funds for any purpose while putting a lien on the property being mortgaged. The loan is "secured" on the borrower's property through a process known as mortgage origination. This means that a legal mechanism is put into place which allows the lender to take possession and sell the secured property to pay off the loan in the event the borrower defaults on the loan or otherwise fails to abide by its terms. The word mortgage is derived from a Law French term used in Britain in the Middle Ages meaning "death pledge" and refers to the pledge ending (dying) when either the obligation is fulfilled or the property is taken through foreclosure. A mortgage can also be described as "a borrower giving consideration in the form of a collateral for a benefit (loan)".

Mortgage underwriting is the process a lender uses to determine if the risk of offering a mortgage loan to a particular borrower under certain parameters is acceptable. Most of the risks and terms that underwriters consider fall under the three C's of underwriting: credit, capacity and collateral.

An Alt-A mortgage, short for Alternative A-paper, is a type of U.S. mortgage that, for various reasons, is considered riskier than A-paper, or "prime", and less risky than "subprime," the riskiest category. For these reasons, as well as in some cases their size, Alt-A loans are not eligible for purchase by Fannie Mae or Freddie Mac. Alt-A interest rates, which are determined by credit risk, therefore tend to be between those of prime and subprime home loans, although there is no single accepted definition of Alt-A. Typically Alt-A mortgages are characterized by borrowers with less than full documentation, average credit scores, higher loan-to-values, and more investment properties and secondary homes. A-minus is related to Alt-A, with some lenders categorizing them the same, but A-minus is traditionally defined as mortgage borrowers with a FICO score of below 680 while Alt-A is traditionally defined as loans lacking full documentation. Alt-A mortgages may have excellent credit but may not meet underwriting criteria for other reasons. During the past decade, a significant amount of Alt-A mortgages resulted from refinancings, rather than property purchases.

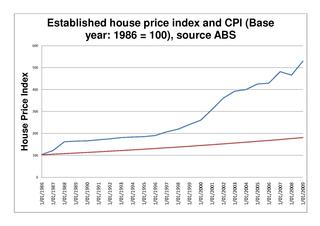

The Australian property bubble is the economic theory that the Australian property market has become or is becoming significantly overpriced and due for a significant downturn. Since the early 2010s, various commentators, including one Treasury official, have claimed the Australian property market is in a significant bubble.

A housing affordability index (HAI) is an index that measures housing affordability, usually the degree to which the median person or family in a particular country or region can afford housing/housing-related costs.

Affordable housing in Canada is housing that is deemed affordable to those with a median household income in Canada.