Related Research Articles

In the United States, Medicaid is a government program that provides health insurance for adults and children with limited income and resources. The program is partially funded and primarily managed by state governments, which also have wide latitude in determining eligibility and benefits, but the federal government sets baseline standards for state Medicaid programs and provides a significant portion of their funding.

Medicare is a federal health insurance program in the United States for people age 65 or older and younger people with disabilities, including those with end stage renal disease and amyotrophic lateral sclerosis. It was begun in 1965 under the Social Security Administration and is now administered by the Centers for Medicare and Medicaid Services (CMS).

Life insurance is a contract between an insurance policy holder and an insurer or assurer, where the insurer promises to pay a designated beneficiary a sum of money upon the death of an insured person. Depending on the contract, other events such as terminal illness or critical illness can also trigger payment. The policyholder typically pays a premium, either regularly or as one lump sum. The benefits may include other expenses, such as funeral expenses.

Health insurance or medical insurance is a type of insurance that covers the whole or a part of the risk of a person incurring medical expenses. As with other types of insurance, risk is shared among many individuals. By estimating the overall risk of health risk and health system expenses over the risk pool, an insurer can develop a routine finance structure, such as a monthly premium or payroll tax, to provide the money to pay for the health care benefits specified in the insurance agreement. The benefit is administered by a central organization, such as a government agency, private business, or not-for-profit entity.

Universal life insurance is a type of cash value life insurance, sold primarily in the United States. Under the terms of the policy, the excess of premium payments above the current cost of insurance is credited to the cash value of the policy, which is credited each month with interest. The policy is debited each month by a cost of insurance (COI) charge as well as any other policy charges and fees drawn from the cash value, even if no premium payment is made that month. Interest credited to the account is determined by the insurer but has a contractual minimum rate. When an earnings rate is pegged to a financial index such as a stock, bond or other interest rate index, the policy is an "Indexed universal life" contract. Such policies offer the advantage of guaranteed level premiums throughout the insured's lifetime at a substantially lower premium cost than an equivalent whole life policy at first. The cost of insurance always increases, as is found on the cost index table. That not only allows for easy comparison of costs between carriers but also works well in irrevocable life insurance trusts (ILITs) since cash is of no consequence.

Long-term care insurance is an insurance product, sold in the United States, United Kingdom and Canada that helps pay for the costs associated with long-term care. Long-term care insurance covers care generally not covered by health insurance, Medicare, or Medicaid.

Medicare Part D, also called the Medicare prescription drug benefit, is an optional United States federal-government program to help Medicare beneficiaries pay for self-administered prescription drugs. Part D was enacted as part of the Medicare Modernization Act of 2003 and went into effect on January 1, 2006. Under the program, drug benefits are provided by private insurance plans that receive premiums from both enrollees and the government. Part D plans typically pay most of the cost for prescriptions filled by their enrollees. However, plans are later reimbursed for much of this cost through rebates paid by manufacturers and pharmacies.

Long-term care (LTC) is a variety of services which help meet both the medical and non-medical needs of people with a chronic illness or disability who cannot care for themselves for long periods. Long-term care is focused on individualized and coordinated services that promote independence, maximize patients' quality of life, and meet patients' needs over a period of time.

The California Medical Assistance Program is the California implementation of the federal Medicaid program serving low-income individuals, including families, seniors, persons with disabilities, children in foster care, pregnant women, and childless adults with incomes below 138% of federal poverty level. Benefits include ambulatory patient services, emergency services, hospitalization, maternity and newborn care, mental health and substance use disorder treatment, dental (Denti-Cal), vision, and long-term care and support. Medi-Cal was created in 1965 by the California Medical Assistance Program a few months after the national legislation was passed. Approximately 15.28 million people were enrolled in Medi-Cal as of September 2022, or about 40% of California's population; in most counties, more than half of eligible residents were enrolled as of 2020.

The Balanced Budget Act of 1997 was an omnibus legislative package enacted by the United States Congress, using the budget reconciliation process, and designed to balance the federal budget by 2002. This act was enacted during Bill Clinton's second term as president.

In the United States, health insurance helps pay for medical expenses through privately purchased insurance, social insurance, or a social welfare program funded by the government. Synonyms for this usage include "health coverage", "health care coverage", and "health benefits". In a more technical sense, the term "health insurance" is used to describe any form of insurance providing protection against the costs of medical services. This usage includes both private insurance programs and social insurance programs such as Medicare, which pools resources and spreads the financial risk associated with major medical expenses across the entire population to protect everyone, as well as social welfare programs like Medicaid and the Children's Health Insurance Program, which both provide assistance to people who cannot afford health coverage.

Medicare Advantage is a type of health plan offered by Medicare-approved private companies that must follow rules set by Medicare. Most Medicare Advantage Plans include drug coverage. Under Part C, Medicare pays a sponsor a fixed payment. The sponsor then pays for the health care expenses of enrollees. Sponsors are allowed to vary the benefits from those provided by Medicare's Parts A and B as long as they provide the actuarial equivalent of those programs. The sponsors vary from primarily integrated health delivery systems to unions to other types of non profit charities to insurance companies.

The Empowering Patients First Act is legislation sponsored by Rep. Tom Price, first introduced as H.R. 3400 in the 111th Congress. The bill was initially intended to be a Republican alternative to the America's Affordable Health Choices Act of 2009, but has since been positioned as a potential replacement to the Patient Protection and Affordable Care Act (PPACA). The bill was introduced in the 112th Congress as H.R. 3000, and in the 113th Congress as H.R. 2300. As of October 2014, the bill has 58 cosponsors. An identical version of the bill has been introduced in the Senate by Senator John McCain as S. 1851.

The Affordable Care Act (ACA), formally known as the Patient Protection and Affordable Care Act (PPACA) and colloquially as Obamacare, is a landmark U.S. federal statute enacted by the 111th United States Congress and signed into law by President Barack Obama on March 23, 2010. Together with the Health Care and Education Reconciliation Act of 2010 amendment, it represents the U.S. healthcare system's most significant regulatory overhaul and expansion of coverage since the enactment of Medicare and Medicaid in 1965. Most of the act's provisions are still in effect.

The Community Living Assistance Services and Supports Act was a U.S. federal law, enacted as Title VIII of the Patient Protection and Affordable Care Act. The CLASS Act would have created a voluntary and public long-term care insurance option for employees, but in October 2011 the Obama administration announced it was unworkable and would be dropped. The CLASS Act was repealed January 1, 2013.

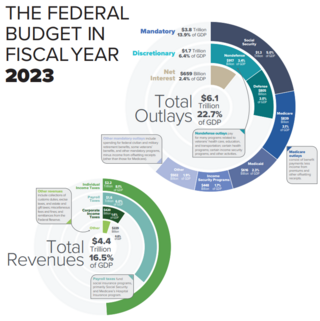

The United States federal budget consists of mandatory expenditures, discretionary spending for defense, Cabinet departments and agencies, and interest payments on debt. This is currently over half of U.S. government spending, the remainder coming from state and local governments.

James Claude Robinson is a professor of health economics at the University of California, Berkeley School of Public Health, where he has the title of the Leonard D. Schaeffer Endowed Chair in Health Economics and Policy. Robinson is also the Chair of the Berkeley Center for Health Technology, which supports research and professional education projects related to coverage, management, and payment methods for innovative technologies including biopharmaceuticals, medical devices, and diagnostics.

Health care finance in the United States discusses how Americans obtain and pay for their healthcare, and why U.S. healthcare costs are the highest in the world based on various measures.

As of 2017, approximately 1.4 million Americans live in a nursing home, two-thirds of whom rely on Medicaid to pay for their care. Residential nursing facilities receive Medicaid federal funding and approvals through a state health department. These facilities may be overseen by various types of state agency.

Life Care Funding, is an American financial, senior care advisory and life settlement company based in Portland, Maine and now operates as LCX LIFE. The company works with seniors to help them access funding solutions to pay for senior living and long term care, and specializes in settling life insurance policies into Long Term Care funds for customers who cannot afford long-term care. The company was founded by Chris Orestis in 2007. Life Care Funding has contributed to legislation reform to help middle-class people to obtain funding for long-term care.

References

- 1 2 Chris Orestis (April 22, 2014). "How a life insurance policy can fund your client's long-term care". Life Health Pro. Retrieved June 22, 2015.

- 1 2 3 4 "Alternative solutions to pay for LTC, part 2". Life Health Pro. May 23, 2011. Retrieved June 22, 2015.

- 1 2 3 "Questions About Long Term Care Benefit Plans". Settlement Benefits Association. Retrieved June 22, 2015.

- 1 2 3 "Conversion of Life-Insurance Policies to Long-Term Care Benefit Plans in Florida" (PDF). Florida State University. January 2012. Retrieved June 22, 2015.

- 1 2 "How Men Can Guard Against Poverty in Their Golden Years". CP Reports. June 18, 2014. Retrieved June 22, 2015.

- ↑ "Converting Life Insurance into Long Term Care Benefits: Life Care Funding's Plan". Paying for Senior Care. Retrieved June 22, 2015.

- ↑ Alex Veiga (October 5, 2014). "Take steps to prepare for possible long-term care costs". The Jackson Sun. Retrieved June 22, 2015.

- 1 2 3 4 "Feds Eye Life Settlements for LTC Funding". Insurance News Net Magazine. December 2013. Retrieved June 22, 2015.

- 1 2 3 Chris Orestis (June 29, 2011). "Alternative Solutions for Funding Long Term Care". Modern Health Talk. Retrieved June 22, 2015.

- ↑ "Home". Life Care Funding. Retrieved June 22, 2015.

- ↑ "Home". The Lifeline Program. Retrieved June 22, 2015.

- 1 2 3 4 Chris Orestis (January 5, 2011). "Funding Long Term Care with Life Insurance: Trend Catches On". Life Health Pro. Retrieved June 22, 2015.

- ↑ "Long term care benefit plans". Oregon Laws.org. Retrieved June 22, 2015.

- ↑ Donna Horowitz (12 February 2015). "Georgia Medicaid Bill Introduced". The Deal.

- ↑ "Life Insurance For Elderly Parents". mylifeinsuranceforelderly.com. Retrieved August 27, 2022.