Related Research Articles

Project management is the process of supervising the work of a team to achieve all project goals within the given constraints. This information is usually described in project documentation, created at the beginning of the development process. The primary constraints are scope, time and budget. The secondary challenge is to optimize the allocation of necessary inputs and apply them to meet predefined objectives.

A quality management system (QMS) is a collection of business processes focused on consistently meeting customer requirements and enhancing their satisfaction. It is aligned with an organization's purpose and strategic direction. It is expressed as the organizational goals and aspirations, policies, processes, documented information, and resources needed to implement and maintain it. Early quality management systems emphasized predictable outcomes of an industrial product production line, using simple statistics and random sampling. By the 20th century, labor inputs were typically the most costly inputs in most industrialized societies, so focus shifted to team cooperation and dynamics, especially the early signaling of problems via a continual improvement cycle. In the 21st century, QMS has tended to converge with sustainability and transparency initiatives, as both investor and customer satisfaction and perceived quality are increasingly tied to these factors. Of QMS regimes, the ISO 9000 family of standards is probably the most widely implemented worldwide – the ISO 19011 audit regime applies to both and deals with quality and sustainability and their integration.

Systems engineering is an interdisciplinary field of engineering and engineering management that focuses on how to design, integrate, and manage complex systems over their life cycles. At its core, systems engineering utilizes systems thinking principles to organize this body of knowledge. The individual outcome of such efforts, an engineered system, can be defined as a combination of components that work in synergy to collectively perform a useful function.

In commerce, supply chain management (SCM) deals with a system of procurement, operations management, logistics and marketing channels, through which raw materials can be developed into finished products and delivered to their end customers. A more narrow definition of supply chain management is the "design, planning, execution, control, and monitoring of supply chain activities with the objective of creating net value, building a competitive infrastructure, leveraging worldwide logistics, synchronising supply with demand and measuring performance globally". This can include the movement and storage of raw materials, work-in-process inventory, finished goods, and end to end order fulfilment from the point of origin to the point of consumption. Interconnected, interrelated or interlinked networks, channels and node businesses combine in the provision of products and services required by end customers in a supply chain.

Cost accounting is defined by the Institute of Management Accountants as "a systematic set of procedures for recording and reporting measurements of the cost of manufacturing goods and performing services in the aggregate and in detail. It includes methods for recognizing, allocating, aggregating and reporting such costs and comparing them with standard costs". Often considered a subset of managerial accounting, its end goal is to advise the management on how to optimize business practices and processes based on cost efficiency and capability. Cost accounting provides the detailed cost information that management needs to control current operations and plan for the future.

In management accounting or managerial accounting, managers use accounting information in decision-making and to assist in the management and performance of their control functions.

Logistics is the part of supply chain management that deals with the efficient forward and reverse flow of goods, services, and related information from the point of origin to the point of consumption according to the needs of customers. Logistics management is a component that holds the supply chain together. The resources managed in logistics may include tangible goods such as materials, equipment, and supplies, as well as food and other consumable items.

Inventory or stock refers to the goods and materials that a business holds for the ultimate goal of resale, production or utilisation.

Economies of scope are "efficiencies formed by variety, not volume". In the field of economics, "economies" is synonymous with cost savings and "scope" is synonymous with broadening production/services through diversified products. Economies of scope is an economic theory stating that average total cost (ATC) of production decrease as a result of increasing the number of different goods produced. For example, a gas station primarily sells gasoline, but can sell soda, milk, baked goods, etc. and thus achieve economies of scope since with the same facility, each new product attracts new dollars a customer would have spent elsewhere. The business historian Alfred Chandler argued that economies of scope contributed to the rise of American business corporations during the 20th century.

In industry, product lifecycle management (PLM) is the process of managing the entire lifecycle of a product from its inception through the engineering, design and manufacture, as well as the service and disposal of manufactured products. PLM integrates people, data, processes, and business systems and provides a product information backbone for companies and their extended enterprises.

A by-product or byproduct is a secondary product derived from a production process, manufacturing process or chemical reaction; it is not the primary product or service being produced.

Activity-based costing (ABC) is a costing method that identifies activities in an organization and assigns the cost of each activity to all products and services according to the actual consumption by each. Therefore, this model assigns more indirect costs (overhead) into direct costs compared to conventional costing.

Operations management is concerned with designing and controlling the production of goods and services, ensuring that businesses are efficient in using resources to meet customer requirements.

Manufacturing process management (MPM) is a collection of technologies and methods used to define how products are to be manufactured. MPM differs from ERP/MRP which is used to plan the ordering of materials and other resources, set manufacturing schedules, and compile cost data.

Direct costs, in accounting, are costs directly accountable to a cost object. The equivalent nomenclature in economics is specific cost. Direct costs may be either fixed or variable, but typically comprise materials, labour, and specific expenses such as, e.g. a royalty payment to a patent holder for a given production process, all, directly attributable to a cost object. Thus by industry:

Manufacturers incur many costs in the production process. It is the cost accountant's job to trace these costs back to a certain product or process during production. Some costs cannot be traced back to a single cost object. Some costs benefit more than one product or process in the manufacturing process. These costs are called joint costs. Almost all manufacturers incur joint costs at some level the manufacturing process. It can also be defined as the cost to operate joint-product processes including the disposal of waste. With regard to joint costs, it is essential to allocate the joint cost for the different joint products for determining individual product costs. Several methods are used to allocate joint costs. These methods are mainly classified onto engineering and non-engineering methods. Nonengineering methods are mainly based on the market share of the product; the higher market share, the higher proportion assigned to it e.g. net realizable value. In this method, the proportions are determined based on the sales value proportions. In the engineering based method, proportions are found based on physical quantities and measurements such as volume, weight, etc.

Cameron International Corporation (formerly Cooper Cameron Corporation (CCC) and Cooper Oil Tool, Cameron Iron Works) though now operating under Schlumberger, is a global provider of pressure control, production, processing, and flow control systems as well as project management and aftermarket services for the oil and gas and process industries. Cameron was acquired by Schlumberger (SLB) in 2016, and now operates as 'Cameron, an SLB Company.' At the start of the SLB acquisition in 2015, Cameron employed approximately 23,000 people and delivered $9.8 billion in revenue.

In economics, joint product is a product that results jointly with other products from processing a common input; this common process is also called joint production. A joint product can be the output of a process with fixed or variable proportions.

Further processing cost is the cost incurred to make joint products ready for further use or sale after the production process' split-off point.

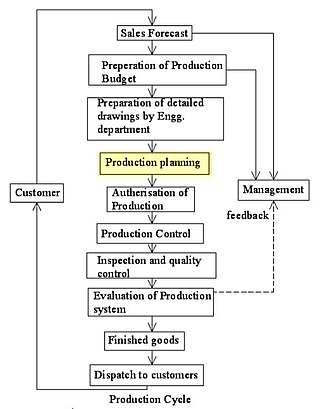

Production planning is the planning of production and manufacturing modules in a company or industry. It utilizes the resource allocation of activities of employees, materials and production capacity, in order to serve different customers.

References

- ↑ Wouters, Mark; Selto, Frank H.; Hilton, Ronald W.; Maher, Michael W. (2012): Cost Management: Strategies for Business Decisions, International Edition, McGraw-Hill, p. 538.

| | This business-related article is a stub. You can help Wikipedia by expanding it. |