Notes

- ↑ "Occupational Privilege Tax @ Aurora, Colorado". www.auroragov.org. Archived from the original on 2006-10-01.

| | This tax-related article is a stub. You can help Wikipedia by expanding it. |

Various state and local taxing authorities in the US require an employer or the employee to withhold and remit a tax on the wages paid to an employee. Some states require both the employer and employee to remit a portion of the total occupational privilege tax (OPT), while others only require one or the other to do so. [1] As such, it is a type of payroll tax. The genesis of this tax is the state's claim in recovering accrued benefits provided to the taxpayer in enabling them to become employed and allowing for the state or municipality to further provide for taxpayers in the future.

| | This tax-related article is a stub. You can help Wikipedia by expanding it. |

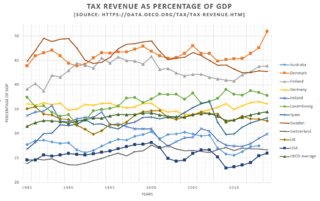

The United States of America has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2020, taxes collected by federal, state, and local governments amounted to 25.5% of GDP, below the OECD average of 33.5% of GDP. The United States had the seventh-lowest tax revenue-to-GDP ratio among OECD countries in 2020, with a higher ratio than Mexico, Colombia, Chile, Ireland, Costa Rica, and Turkey.

A pension is a fund into which a sum of money is added during an employee's employment years and from which payments are drawn to support the person's retirement from work in the form of periodic payments. A pension may be a "defined benefit plan", where a fixed sum is paid regularly to a person, or a "defined contribution plan", under which a fixed sum is invested that then becomes available at retirement age. Pensions should not be confused with severance pay; the former is usually paid in regular amounts for life after retirement, while the latter is typically paid as a fixed amount after involuntary termination of employment before retirement.

A pay-as-you-earn tax (PAYE), or pay-as-you-go (PAYG) in Australia, is a withholding of taxes on income payments to employees. Amounts withheld are treated as advance payments of income tax due. They are refundable to the extent they exceed tax as determined on tax returns. PAYE may include withholding the employee portion of insurance contributions or similar social benefit taxes. In most countries, they are determined by employers but subject to government review. PAYE is deducted from each paycheck by the employer and must be remitted promptly to the government. Most countries refer to income tax withholding by other terms, including pay-as-you-go tax.

Payroll taxes are taxes imposed on employers or employees, and are usually calculated as a percentage of the salaries that employers pay their employees. By law, some payroll taxes are the responsibility of the employee and others fall on the employer, but almost all economists agree that the true economic incidence of a payroll tax is unaffected by this distinction, and falls largely or entirely on workers in the form of lower wages. Because payroll taxes fall exclusively on wages and not on returns to financial or physical investments, payroll taxes may contribute to underinvestment in human capital such as higher education.

The Canada Revenue Agency is the revenue service of the federal government, and most provincial and territorial governments. The CRA collects taxes, administers tax law and policy, and delivers benefit programs and tax credits. Legislation administered by the CRA includes the Income Tax Act, parts of the Excise Tax Act, and parts of laws relating to the Canada Pension Plan, employment insurance (EI), tariffs and duties. The agency also oversees the registration of charities in Canada, and enforces much of the country's tax laws.

Garnishment is a legal process for collecting a monetary judgment on behalf of a plaintiff from a defendant. Garnishment allows the plaintiff to take the money or property of the debtor from the person or institution that holds that property. A similar legal mechanism called execution allows the seizure of money or property held directly by the debtor.

Three key types of withholding tax are imposed at various levels in the United States:

Form W-2 is an Internal Revenue Service (IRS) tax form used in the United States to report wages paid to employees and the taxes withheld from them. Employers must complete a Form W-2 for each employee to whom they pay a salary, wage, or other compensation as part of the employment relationship. An employer must mail out the Form W-2 to employees on or before January 31. This deadline gives these taxpayers about 2 months to prepare their returns before the April 15 income tax due date. The form is also used to report FICA taxes to the Social Security Administration. The Form W-2, along with Form W-3, generally must be filed by the employer with the Social Security Administration by the end of February. Relevant amounts on Form W-2 are reported by the Social Security Administration to the Internal Revenue Service. In territories, the W-2 is issued with a two letter code indicating which territory, such as W-2GU for Guam. If corrections are made, it can be done on a W-2c.

Tax withholding, also known as tax retention, Pay-as-You-Go, Pay-as-You-Earn, or a Prélèvement à la source, is income tax paid to the government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient. In most jurisdictions, tax withholding applies to employment income. Many jurisdictions also require withholding taxes on payments of interest or dividends. In most jurisdictions, there are additional tax withholding obligations if the recipient of the income is resident in a different jurisdiction, and in those circumstances withholding tax sometimes applies to royalties, rent or even the sale of real estate. Governments use tax withholding as a means to combat tax evasion, and sometimes impose additional tax withholding requirements if the recipient has been delinquent in filing tax returns, or in industries where tax evasion is perceived to be common.

Income taxes in the United States are imposed by the federal government, and most states. The income taxes are determined by applying a tax rate, which may increase as income increases, to taxable income, which is the total income less allowable deductions. Income is broadly defined. Individuals and corporations are directly taxable, and estates and trusts may be taxable on undistributed income. Partnerships are not taxed, but their partners are taxed on their shares of partnership income. Residents and citizens are taxed on worldwide income, while nonresidents are taxed only on income within the jurisdiction. Several types of credits reduce tax, and some types of credits may exceed tax before credits. An alternative tax applies at the federal and some state levels.

Salaries tax is a type of income tax that is levied in Hong Kong, chargeable on income from any office, employment and pension for a year of assessment arising in or derived from the territory. For purposes of calculating liability, the period of assessment is from April 1 to March 31 of the following year.

Tax protesters in the United States have advanced a number of arguments asserting that the assessment and collection of the federal income tax violates statutes enacted by the United States Congress and signed into law by the President. Such arguments generally claim that certain statutes fail to create a duty to pay taxes, that such statutes do not impose the income tax on wages or other types of income claimed by the tax protesters, or that provisions within a given statute exempt the tax protesters from a duty to pay.

Internal Revenue Service (IRS) tax forms are forms used for taxpayers and tax-exempt organizations to report financial information to the Internal Revenue Service of the United States. They are used to report income, calculate taxes to be paid to the federal government, and disclose other information as required by the Internal Revenue Code (IRC). There are over 800 various forms and schedules. Other tax forms in the United States are filed with state and local governments.

Taxation in Colombia is determined by the Congress of Colombia, every Department Assembly and every City Council, which determine what kind of taxes can be levied and which rates can be applied. The country inherited a harsh and diffused taxation policy from the Spanish Empire characterized by a heavy reliance on customs duties.

Taxation in Sweden on salaries for an employee involves contributing to three different levels of government: the municipality, the county council, and the central government. Social security contributions are paid to finance the social security system.

A company car is a vehicle which companies or organisations lease or own and which employees use for their personal and business travel. Take-home vehicle is a vehicle which can be taken home by company employees. Depending on the company, company cars may be available to all employees or just top level personnel.

Taxation in Finland is mainly carried out through the Finnish Tax Administration, an agency of the Ministry of Finance. Finnish Customs and the Finnish Transport and Communications Agency Traficom, also collect taxes. Taxes collected are distributed to the Government, municipalities, church, and the Social Insurance Institution, Kela.

Taxation may involve payments to a minimum of two different levels of government: central government through SARS or to local government. Prior to 2001 the South African tax system was "source-based", wherein income is taxed in the country where it originates. Since January 2001, the tax system was changed to "residence-based" wherein taxpayers residing in South Africa are taxed on their income irrespective of its source. Non residents are only subject to domestic taxes.

Taxation in Estonia consists of state and local taxes. A relatively high proportion of government revenue comes from consumption taxes whilst revenue from capital taxes is one of the lowest in the European Union.

In the United States, the combination of payroll taxes withheld from a household employee and the employment taxes paid by their employer are commonly referred to as the nanny tax. Under US law, any family or individual that pays a household employee more than $2,100 a year must withhold and pay Social Security and Medicare taxes, also known as FICA. The law mandates that all domestic workers, such as cooks, nannies, housekeepers and gardeners, are subject to the nanny tax. Federal unemployment insurance taxes must also be paid if the household pays any number of employees a total of $1,000 or more in a calendar quarter. State unemployment insurance taxes have the same requirement with the exceptions of California ($750), New York ($500), and Washington, D.C. ($500) have lower thresholds.