Related Research Articles

A tax is a compulsory financial charge or some other type of levy imposed on a taxpayer by a governmental organization in order to collectively fund government spending, public expenditures, or as a way to regulate and reduce negative externalities. Tax compliance refers to policy actions and individual behaviour aimed at ensuring that taxpayers are paying the right amount of tax at the right time and securing the correct tax allowances and tax relief. The first known taxation took place in Ancient Egypt around 3000–2800 BC. Taxes consist of direct or indirect taxes and may be paid in money or as its labor equivalent.

A sales tax is a tax paid to a governing body for the sales of certain goods and services. Usually laws allow the seller to collect funds for the tax from the consumer at the point of purchase.

A taxpayer is a person or organization subject to pay a tax. Modern taxpayers may have an identification number, a reference number issued by a government to citizens or firms.

Goods and Services Tax (GST) in Australia is a value added tax of 10% on most goods and services sales, with some exemptions and concessions. GST is levied on most transactions in the production process, but is in many cases refunded to all parties in the chain of production other than the final consumer.

Room service or in-room dining is a hotel service enabling guests to choose items of food and drink for delivery to their hotel room for consumption. Room service is organized as a subdivision within the food and beverage department of high-end hotel and resort properties. It is uncommon for room service to be offered in hotels that are not high-end, or in motels. Room service may also be provided for guests on cruise ships. Room service may be provided on a 24-hour basis or limited to late night hours only. Due to the cost of customized orders and delivery of room service, prices charged to the patron are typically much higher than in the hotel's restaurant or tuck shop, and a gratuity is expected in some regions.

The hospitality industry is a broad category of fields within the service industry that includes lodging, food and beverage service, event planning, theme parks, travel agency, tourism, hotels, restaurants and bars.

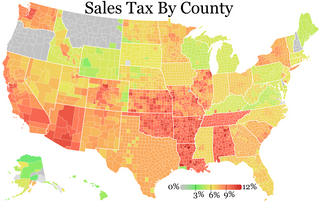

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. 45 states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

A fat tax is a tax or surcharge that is placed upon fattening food, beverages or on overweight individuals. It is considered an example of Pigovian taxation. A fat tax aims to discourage unhealthy diets and offset the economic costs of obesity.

The Louisiana Lottery Corporation (LLC) is a government-run lottery that is used to generate revenue without increasing taxes. The proceeds of the Lottery go to the Minimum Foundation Program that funds public education in Louisiana. The daily activities involved with running the cooperation are handled by the president of the Louisiana Lottery Cooperation. The president is under the supervision of the Lottery's nine-member governing board of directors.

The total gross state product for Connecticut for 2012 was $229.3 billion, up from $225.4 billion in 2011.

A sugary drink tax, soda tax, or sweetened beverage tax (SBT) is a tax or surcharge designed to reduce consumption of sweetened beverages. Drinks covered under a soda tax often include carbonated soft drinks, sports drinks and energy drinks. This policy intervention is an effort to decrease obesity and the health impacts related to being overweight, however the medical evidence supporting the benefits of a sugar tax on health is of very low certainty. The tax is a matter of public debate in many countries and beverage producers like Coca-Cola often oppose it. Advocates such as national medical associations and the World Health Organization promote the tax as an example of Pigovian taxation, aimed to discourage unhealthy diets and offset the growing economic costs of obesity.

The Tennessee Bottle Bill is citizen-supported container-deposit recycling legislation, which if enacted will place a 5-cent deposit on beverage containers sold in Tennessee. The bill applies to containers made of aluminum/bimetal, glass or any plastic, containing soft drinks, beer/malt beverages, carbonated or non-carbonated waters, plain or flavored waters, energy drinks, juices, iced teas or iced coffees. Milk/dairy, nutritional drinks and wine and spirits are not included in the program.

Road Improvement and Development Effort or RIDE is a plan for road projects in Horry County, South Carolina, including Carolina Bays Parkway, Veterans Highway and Robert Grissom Parkway. The first phase, costing $1.1 billion, was being paid for by hospitality taxes. The second phase, called RIDE II, was being paid for through a one-cent sales tax approved by Horry County voters November 7, 2006. RIDE III was being planned as of 2013 and voters approved a penny tax in 2016.

The northwestern U.S. state of Washington's economy grew 3.7% in 2016, nearly two and a half times the national rate. Average income per head in 2009 was $41,751, 12th among states of the U.S.

Taxes in California are collected by state and local governments through a number of tax categories.

Taxation may involve payments to a minimum of two different levels of government: central government through SARS or to local government. Prior to 2001 the South African tax system was "source-based", where in income is taxed in the country where it originates. Since January 2001, the tax system was changed to "residence-based" wherein taxpayers residing in South Africa are taxed on their income irrespective of its source. Non residents are only subject to domestic taxes.

Business improvement districts (BIDs), also known as local improvement districts (LIDs), are special districts within a city that are overseen by a nonprofit entity. In the United States, BIDs are typically funded by an additional tax assessment, with the tax increase going toward improvements of the area. BIDs have been used in nearly 1,000 major cities and small towns throughout the United States, including most major U.S. cities that have multiple BIDs. New York City alone has 76 BIDs.

The Fairfax County meals tax referendum is a 2016 referendum that proposes a 4% tax on all prepared meals sold in Fairfax County, Virginia. The 4% tax would be on top of the current 6% state sales tax, resulting in a total of 10% in taxes charged on all prepared meals. The referendum was voted on by Fairfax County residents in the general election on November 8, 2016.

A value-added tax (VAT), known in some countries as a goods and services tax (GST), is a type of tax that is assessed incrementally. It is levied on the price of a product or service at each stage of production, distribution, or sale to the end consumer. If the ultimate consumer is a business that collects and pays to the government VAT on its products or services, it can reclaim the tax paid. It is similar to, and is often compared with, a sales tax. VAT is an indirect tax because the person who ultimately bears the burden of the tax is not necessarily the same person as the one who pays the tax to the tax authorities.

The Tax Reform for Acceleration and Inclusion Law, officially designated as Republic Act No. 10963, is the initial package of the Comprehensive Tax Reform Program (CTRP) signed into law by President Rodrigo Duterte on December 19, 2017.

References

- 1 2 3 4 5 6 7 8 Chapter 105. Taxation., archived from the original on 3 Jul 2013

- 1 2 3 "North Carolina Tax Guide 2010" (PDF). Archived from the original (PDF) on 2013-10-21. Retrieved 2013-04-16.

- 1 2 3 4 Spanberg, Erik (23 Jan 2013). "Food fight in Carolina Panthers stadium talks". Charlotte Business Journal .

- 1 2 3 4 5 6 Wade, D'Anna, The Food Fight: an Examination of the Prepared Meals and Beverage Tax as a Viable Revenue Generation Source in North Carolina (PDF), archived from the original (PDF) on 5 Mar 2016

- 1 2 3 4 5 6 "North Carolina Department of State Treasurer". Archived from the original on 2013-04-18. Retrieved 2013-04-16.