Balance of trade is the difference between the monetary value of a nation's exports and imports of goods over a certain time period. Sometimes services are also considered but the official IMF definition only considers goods. The balance of trade measures a flow variable of exports and imports over a given period of time. The notion of the balance of trade does not mean that exports and imports are "in balance" with each other.

A gold standard is a monetary system in which the standard economic unit of account is based on a fixed quantity of gold. The gold standard was the basis for the international monetary system from the 1870s to the early 1920s, and from the late 1920s to 1932 as well as from 1944 until 1971 when the United States unilaterally terminated convertibility of the US dollar to gold, effectively ending the Bretton Woods system. Many states nonetheless hold substantial gold reserves.

John Maynard Keynes, 1st Baron Keynes, was an English economist and philosopher whose ideas fundamentally changed the theory and practice of macroeconomics and the economic policies of governments. Originally trained in mathematics, he built on and greatly refined earlier work on the causes of business cycles. One of the most influential economists of the 20th century, he produced writings that are the basis for the school of thought known as Keynesian economics, and its various offshoots. His ideas, reformulated as New Keynesianism, are fundamental to mainstream macroeconomics. He is known as the "father of macroeconomics".

The Bretton Woods Conference, formally known as the United Nations Monetary and Financial Conference, was the gathering of 730 delegates from all 44 allied nations at the Mount Washington Hotel, in Bretton Woods, New Hampshire, United States, to regulate what would be the international monetary and financial order after the conclusion of World War II., likewise with adjusting its proponents.

The global financial system is the worldwide framework of legal agreements, institutions, and both formal and informal economic action that together facilitate international flows of financial capital for purposes of investment and trade financing. Since emerging in the late 19th century during the first modern wave of economic globalization, its evolution is marked by the establishment of central banks, multilateral treaties, and intergovernmental organizations aimed at improving the transparency, regulation, and effectiveness of international markets. In the late 1800s, world migration and communication technology facilitated unprecedented growth in international trade and investment. At the onset of World War I, trade contracted as foreign exchange markets became paralyzed by money market illiquidity. Countries sought to defend against external shocks with protectionist policies and trade virtually halted by 1933, worsening the effects of the global Great Depression until a series of reciprocal trade agreements slowly reduced tariffs worldwide. Efforts to revamp the international monetary system after World War II improved exchange rate stability, fostering record growth in global finance.

Within the budgetary process, deficit spending is the amount by which spending exceeds revenue over a particular period of time, also called simply deficit, or budget deficit, the opposite of budget surplus. The term may be applied to the budget of a government, private company, or individual. A central point of controversy in economics, government deficit spending was first identified as a necessary economic tool by John Maynard Keynes in the wake of the Great Depression.

In international economics, the balance of payments of a country is the difference between all money flowing into the country in a particular period of time and the outflow of money to the rest of the world. In other words, it is economic transactions between countries during a period of time. These financial transactions are made by individuals, firms and government bodies to compare receipts and payments arising out of trade of goods and services.

In macroeconomics and international finance, a country's current account records the value of exports and imports of both goods and services and international transfers of capital. It is one of the two components of the balance of payments, the other being the capital account. Current account measures the nation's earnings and spendings abroad and it consists of the balance of trade, net primary income or factor income and net unilateral transfers, that have taken place over a given period of time. The current account balance is one of two major measures of a country's foreign trade. A current account surplus indicates that the value of a country's net foreign assets grew over the period in question, and a current account deficit indicates that it shrank. Both government and private payments are included in the calculation. It is called the current account because goods and services are generally consumed in the current period.

The Bretton Woods system of monetary management established the rules for commercial relations among the United States, Canada, Western European countries, and Australia and other countries, a total of 44 countries after the 1944 Bretton Woods Agreement. The Bretton Woods system was the first example of a fully negotiated monetary order intended to govern monetary relations among independent states. The Bretton Woods system required countries to guarantee convertibility of their currencies into U.S. dollars to within 1% of fixed parity rates, with the dollar convertible to gold bullion for foreign governments and central banks at US$35 per troy ounce of fine gold. It also envisioned greater cooperation among countries in order to prevent future competitive devaluations, and thus established the International Monetary Fund (IMF) to monitor exchange rates and lend reserve currencies to nations with balance of payments deficits.

Stuart Kingsley Holland is a British economist and former politician. As a Member of Parliament for the Labour Party, Holland represented the Vauxhall constituency in Lambeth, London, from 1979 to 1989, when he resigned his seat to take up a post at the European University Institute in Florence.

In macroeconomics and international finance, the capital account, also known as the capital and financial account, records the net flow of investment into an economy. It is one of the two primary components of the balance of payments, the other being the current account. Whereas the current account reflects a nation's net income, the capital account reflects net change in ownership of national assets.

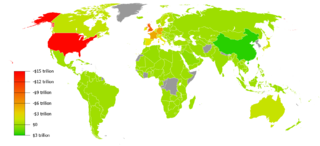

The Triffin dilemma is the conflict of economic interests that arises between short-term domestic and long-term international objectives for countries whose currencies serve as global reserve currencies. This dilemma was identified in the 1960s by Belgian-American economist Robert Triffin. He noted that a country whose currency is the global reserve currency, held by other nations as foreign exchange (FX) reserves to support international trade, must somehow supply the world with its currency in order to fulfill world demand for these FX reserves. This supply function is nominally accomplished by international trade, with the country holding reserve currency status being required to run an inevitable trade deficit. After going off of the gold standard in 1971 and setting up the petrodollar system later in the 1970s, the United States accepted the burden of such an ongoing trade deficit in 1985 with its permanent transformation from a creditor to a debtor nation. The U.S. goods trade deficit is currently on the order of one trillion dollars per year. Such a continuing drain to the United States in its balance of trade leads to ongoing tension between its national trade policies and its global monetary policy to maintain the U.S. dollar as the current global reserve currency. Alternatives to international trade that address this tension include direct transfer of dollars via foreign aid and swap lines.

The bancor was a supranational currency that John Maynard Keynes and E. F. Schumacher conceptualised in the years 1940–1942 and which the United Kingdom proposed to introduce after World War II. The name was inspired by the French banque or. This newly created supranational currency would then be used in international trade as a unit of account within a multilateral clearing system—the International Clearing Union—which would also need to be founded.

Monetary hegemony is an economic and political concept in which a single state has decisive influence over the functions of the international monetary system. A monetary hegemon would need:

Capital controls are residency-based measures such as transaction taxes, other limits, or outright prohibitions that a nation's government can use to regulate flows from capital markets into and out of the country's capital account. These measures may be economy-wide, sector-specific, or industry specific. They may apply to all flows, or may differentiate by type or duration of the flow.

The term exorbitant privilege refers to the benefits the United States has due to its own currency being the international reserve currency. For example, the US would not face a balance of payments crisis, because their imports are purchased in their own currency. Exorbitant privilege as a concept cannot refer to currencies that have a regional reserve currency role, only to global reserve currencies.

Following the global 2007–2008 financial crisis, there was a worldwide resurgence of interest in Keynesian economics among prominent economists and policy makers. This included discussions and implementation of economic policies in accordance with the recommendations made by John Maynard Keynes in response to the Great Depression of the 1930s, most especially fiscal stimulus and expansionary monetary policy.

An international monetary system is a set of internationally agreed rules, conventions and supporting institutions that facilitate international trade, cross border investment and generally the reallocation of capital between states that have different currencies. It should provide means of payment acceptable to buyers and sellers of different nationalities, including deferred payment. To operate successfully, it needs to inspire confidence, to provide sufficient liquidity for fluctuating levels of trade, and to provide means by which global imbalances can be corrected. The system can grow organically as the collective result of numerous individual agreements between international economic factors spread over several decades. Alternatively, it can arise from a single architectural vision, as happened at Bretton Woods in 1944.

Currency war, also known as competitive devaluations, is a condition in international affairs where countries seek to gain a trade advantage over other countries by causing the exchange rate of their currency to fall in relation to other currencies. As the exchange rate of a country's currency falls, exports become more competitive in other countries, and imports into the country become more and more expensive. Both effects benefit the domestic industry, and thus employment, which receives a boost in demand from both domestic and foreign markets. However, the price increases for import goods are unpopular as they harm citizens' purchasing power; and when all countries adopt a similar strategy, it can lead to a general decline in international trade, harming all countries.

Ioannis Georgiou "Yanis" Varoufakis is a Greek economist and politician. Since 2018, he has been Secretary-General of Democracy in Europe Movement 2025 (DiEM25), a left-wing pan-European political party he co-founded in 2016. Previously, he was a member of Syriza and was Greece's Minister of Finance between January 2015 and July 2015, negotiating on behalf of the Greek government during the 2009-2018 Greek government-debt crisis.