Related Research Articles

A debit card, also known as a check card or bank card is a payment card that can be used in place of cash to make purchases. The term plastic card includes the above and as an identity document. These are similar to a credit card, but unlike a credit card, the money for the purchase must be in the cardholder's bank account at the time of a purchase and is immediately transferred directly from that account to the merchant's account to pay for the purchase.

Electronic funds transfer at point of sale is an electronic payment system involving electronic funds transfers based on the use of payment cards, such as debit or credit cards, at payment terminals located at points of sale. EFTPOS technology was developed during the 1980s. In Australia and New Zealand, it is also the brand name of a specific system used for such payments; these systems are mainly country-specific and do not interconnect. In Singapore, it is known as NETS.

A transaction account, also called a checking account, chequing account, current account, demand deposit account, or share draft account at credit unions, is a deposit account held at a bank or other financial institution. It is available to the account owner "on demand" and is available for frequent and immediate access by the account owner or to others as the account owner may direct. Access may be in a variety of ways, such as cash withdrawals, use of debit cards, cheques (checks) and electronic transfer. In economic terms, the funds held in a transaction account are regarded as liquid funds. In accounting terms, they are considered as cash.

The Australian financial system consists of the arrangements covering the borrowing and lending of funds and the transfer of ownership of financial claims in Australia, comprising:

In banking and finance, clearing denotes all activities from the time a commitment is made for a transaction until it is settled. This process turns the promise of payment into the actual movement of money from one account to another. Clearing houses were formed to facilitate such transactions among banks.

Bacs Payment Schemes Limited (Bacs), previously known as Bankers' Automated Clearing System, is responsible for the clearing and settlement of UK automated direct debit and Bacs Direct Credit and the provision of third-party services. Bacs became a subsidiary of Pay.UK on 1 May 2018, and responsibility for direct debit, Bacs Direct Credit, the Current Account Switch Service, Cash ISA Transfer Service and the Industry Sort Code Directory was given to Pay.UK.

A direct debit or direct withdrawal is a financial transaction in which one person withdraws funds from another person's bank account. Formally, the person who directly draws the funds instructs their bank to collect an amount directly from another's bank account designated by the payer and pay those funds into a bank account designated by the payee. Before the payer's banker will allow the transaction to take place, the payer must have advised the bank that they have authorized the payee to directly draw the funds. It is also called pre-authorized debit (PAD) or pre-authorized payment (PAP). After the authorities are set up, the direct debit transactions are usually processed electronically.

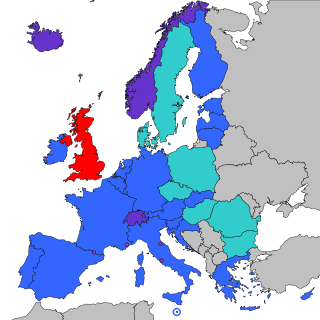

The Single Euro Payments Area (SEPA) is a payment-integration initiative of the European Union for simplification of bank transfers denominated in euro. As of 2020, there were 36 members in SEPA, consisting of the 27 member states of the European Union, the four member states of the European Free Trade Association, and the United Kingdom. Some microstates participate in the technical schemes: Andorra, Monaco, San Marino, and Vatican City.

A standing order is an instruction a bank account holder gives to their bank to pay a set amount at regular intervals to another's account. The instruction is sometimes known as a banker's order.

LINK is a British interbank network. It is the largest interbank network in United Kingdom.

The Faster Payments Service (FPS) is a United Kingdom banking initiative to reduce payment times between different banks' customer accounts to typically a few seconds, from the three working days that transfers usually take using the long-established BACS system. CHAPS, which was introduced in 1984, provides a limited faster-than-BACS service for "high value" transactions, while FPS is focused on the much larger number of smaller payments, subject to limits set by the individual banks, with some allowing Faster Payments of up to £1million. Transfer time, while expected to be short, is not guaranteed, nor is it guaranteed that the receiving institution will immediately credit the payee's account.

The BancNet (BN) Point-Of-Sale System is a local PIN-based electronic funds transfer (EFTPOS) payments solution operated by BancNet on behalf of the member banks and China UnionPay (CUP). The BN point of sale (POS) System allows merchants to accept the automated teller machine (ATM) cards of any active BancNet member bank as payment for goods or services and obliges BN to settle the transaction as early as the following banking day through a direct deposit to a settlement account with any member bank. Acceptance of CUP cards is limited to SM Prime Holdings, Inc.'s Department Store, Supermarket, Hypermarket, Super Sale, Watson's, Sports Central, SM Appliance, Toy Kingdom, and select Surplus Stores.

Payment and Settlement Systems in India are used for financial transactions. They are covered by the Payment and Settlement Systems Act of 2007, legislated in December 2007 and regulated by the Reserve Bank of India and the Board for Regulation and Supervision of Payment and Settlement Systems.

National Westminster Bank, commonly known as NatWest, is a major retail and commercial bank in the United Kingdom based in London, England. It was established in 1968 by the merger of National Provincial Bank and Westminster Bank. In 2000, it became part of The Royal Bank of Scotland Group, which was re-named NatWest Group in 2020. Following ringfencing of the group's core domestic business, the bank became a direct subsidiary of NatWest Holdings; NatWest Markets comprises the non-ringfenced investment banking arm. The British government currently owns around 48.1%, previously 54.7% of NatWest Group after spending 45 billion pounds bailing out the lender in 2008.

Direct Corporate Access (DCA) is part of the Faster Payments Service which provides a same day clearing payment service to UK member banks. Direct Corporate Access (DCA) will provide Banks' business customers with direct access to the Faster Payments Service (FPS) clearing service in a very similar way that Bacstel-IP provides access to BACS.

Debit Mastercard is a brand of debit cards provided by Mastercard. They use the same systems as standard Mastercard credit cards but they do not use a line of credit to the customer, instead relying on funds that the customer has in their bank account.

The Soneri Bank Limited is a Pakistani bank based in Karachi, Sindh, Pakistan. Its head office is located in the PNSC Building. It is a mid-sized bank having about over 360 branches country-wide. Soneri Bank started its operation in the year 1992.

JPMorgan Chase is an American multinational banking corporation with a large presence in the United Kingdom. The corporation’s European subsidiaries J.P. Morgan Europe Limited, J.P. Morgan International Bank Limited and J.P. Morgan Securities plc are headquartered in London.

Vocalink is a payment systems company headquartered in the United Kingdom, created in 2007 from the merger between Voca and LINK. It designs, builds and operates the UK payments infrastructure, which underpins the provision of the Bacs payment system and the UK ATM LINK switching platform covering 65,000 ATMs and the UK Faster Payments systems.

An automated clearing house (ACH) is a computer-based electronic network for processing transactions, usually domestic low value payments, between participating financial institutions. It may support both credit transfers and direct debits. The ACH system is designed to process batches of payments containing numerous transactions, and it charges fees low enough to encourage its use for low value payments.

References

- ↑ "Direct Debit Glossary". BACS Payment Schemes Limited. 2005. Archived from the original on 2007-02-24. Retrieved 2007-03-20.

- ↑ "About Voca – History". Voca Limited. Archived from the original on 2007-01-04. Retrieved 2007-03-20.

- ↑ "S-plugins" . Retrieved 27 September 2018.

- ↑ "Review of Banking Services in the UK". HM Treasury. Retrieved 2007-03-20.