The Eastern Caribbean dollar is the currency of all seven full members and one associate member of the Organisation of Eastern Caribbean States (OECS). The successor to the British West Indies dollar, it has existed since 1965, and it is normally abbreviated with the dollar sign $ or, alternatively, EC$ to distinguish it from other dollar-denominated currencies. The EC$ is subdivided into 100 cents. It has been pegged to the United States dollar since 7 July 1976, at the exchange rate of US$1 = EC$2.70.

The global financial system is the worldwide framework of legal agreements, institutions, and both formal and informal economic action that together facilitate international flows of financial capital for purposes of investment and trade financing. Since emerging in the late 19th century during the first modern wave of economic globalization, its evolution is marked by the establishment of central banks, multilateral treaties, and intergovernmental organizations aimed at improving the transparency, regulation, and effectiveness of international markets. In the late 1800s, world migration and communication technology facilitated unprecedented growth in international trade and investment. At the onset of World War I, trade contracted as foreign exchange markets became paralyzed by money market illiquidity. Countries sought to defend against external shocks with protectionist policies and trade virtually halted by 1933, worsening the effects of the global Great Depression until a series of reciprocal trade agreements slowly reduced tariffs worldwide. Efforts to revamp the international monetary system after World War II improved exchange rate stability, fostering record growth in global finance.

The Monetary Authority of Singapore or (MAS), is the central bank and financial regulatory authority of Singapore. It administers the various statutes pertaining to money, banking, insurance, securities and the financial sector in general, as well as currency issuance and manages the foreign-exchange reserves. It was established in 1971 to act as the banker to and as a financial agent of the Government of Singapore. The body is duly accountable to the Parliament of Singapore through the Minister-in-charge, who is also the Incumbent Chairman of the central bank.

Monetary policy is the policy adopted by the monetary authority of a nation to affect monetary and other financial conditions to accomplish broader objectives like high employment and price stability. Further purposes of a monetary policy may be to contribute to economic stability or to maintain predictable exchange rates with other currencies. Today most central banks in developed countries conduct their monetary policy within an inflation targeting framework, whereas the monetary policies of most developing countries' central banks target some kind of a fixed exchange rate system. A third monetary policy strategy, targeting the money supply, was widely followed during the 1980s, but has diminished in popularity since that, though it is still the official strategy in a number of emerging economies.

The Eastern Caribbean Central Bank (ECCB) is a supranational central bank that serves Anguilla, Antigua and Barbuda, Dominica, Grenada, Montserrat, Saint Kitts and Nevis, Saint Lucia, and Saint Vincent and the Grenadines, all members of the Organisation of Eastern Caribbean States (OECS) that use the ECCB-issued Eastern Caribbean Dollar as their currency. The ECCB was established in 1983, succeeding the British Caribbean Currency Board (1950–1965) and the Eastern Caribbean Currency Authority (1965–1983). It is also in charge of bank supervision within its geographical remit.

The Bretton Woods system of monetary management established the rules for commercial relations among the United States, Canada, Western European countries, and Australia as well as 44 other countries after the 1944 Bretton Woods Agreement. The Bretton Woods system was the first example of a fully negotiated monetary order intended to govern monetary relations among independent states. The Bretton Woods system required countries to guarantee convertibility of their currencies into U.S. dollars to within 1% of fixed parity rates, with the dollar convertible to gold bullion for foreign governments and central banks at US$35 per troy ounce of fine gold. It also envisioned greater cooperation among countries in order to prevent future competitive devaluations, and thus established the International Monetary Fund (IMF) to monitor exchange rates and lend reserve currencies to nations with balance of payments deficits.

In public finance, a currency board is a monetary authority which is required to maintain a fixed exchange rate with a foreign currency. This policy objective requires the conventional objectives of a central bank to be subordinated to the exchange rate target. In colonial administration, currency boards were popular because of the advantages of printing appropriate denominations for local conditions, and it also benefited the colony with the seigniorage revenue. However, after World War II many independent countries preferred to have central banks and independent currencies.

The Central Bank of Malaysia is the Malaysian central bank. Established on 26 January 1959 as the Central Bank of Malaya, its main purpose is to issue currency, act as the banker and advisor to the government of Malaysia, and to regulate the country's financial institutions, credit system and monetary policy. Its headquarters is located in Kuala Lumpur, the federal capital of Malaysia.

The British West Indies dollar (BWI$) was the currency of British Guiana and the Eastern Caribbean territories of the British West Indies from 1949 to 1965, when it was largely replaced by the East Caribbean dollar, and was one of the currencies used in Jamaica from 1954 to 1964. The monetary policy of the currency was overseen by the British Caribbean Currency Board (BCCB). It was the official currency used by the West Indies Federation. The British West Indies dollar was never used in British Honduras, the Cayman Islands, the Turks and Caicos Islands, the Bahamas, or Bermuda.

A managed float regime, also known as a dirty float, is a type of exchange rate regime where a currency's value is allowed to fluctuate in response to foreign-exchange market mechanisms, but the central bank or monetary authority of the country intervenes occasionally to stabilize or steer the currency's value in a particular direction. This is in contrast to a pure float where the value is entirely determined by market forces, and a fixed exchange rate where the value is pegged to another currency or a basket of currencies.

In macroeconomics and modern monetary policy, a devaluation is an official lowering of the value of a country's currency within a fixed exchange-rate system, in which a monetary authority formally sets a lower exchange rate of the national currency in relation to a foreign reference currency or currency basket. The opposite of devaluation, a change in the exchange rate making the domestic currency more expensive, is called a revaluation. A monetary authority maintains a fixed value of its currency by being ready to buy or sell foreign currency with the domestic currency at a stated rate; a devaluation is an indication that the monetary authority will buy and sell foreign currency at a lower rate.

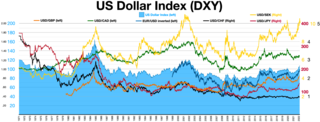

The foreign exchange market is a global decentralized or over-the-counter (OTC) market for the trading of currencies. This market determines foreign exchange rates for every currency. It includes all aspects of buying, selling and exchanging currencies at current or determined prices. In terms of trading volume, it is by far the largest market in the world, followed by the credit market.

The Bank of Korea is the central bank of the Republic of Korea and issuer of South Korean won. It was established on 12 June 1950 in Seoul, South Korea.

The Trinidad and Tobago dollar is the currency of Trinidad and Tobago. It is normally abbreviated with the dollar sign $, or alternatively TT$ to distinguish it from other dollar-denominated currencies. It is subdivided into 100 cents. Cents are abbreviated with the cent sign ¢, or TT¢ to distinguish from other currencies that use cents. Its predecessor currencies are the Trinidadian dollar and the Tobagonian dollar.

The Convertibility plan was a plan by the Argentine Currency Board that pegged the Argentine peso to the U.S. dollar between 1991 and 2002 in an attempt to eliminate hyperinflation and stimulate economic growth. While it initially met with considerable success, the board's actions ultimately failed. The peso was only pegged to the dollar until 2002.

The National Bank of Ethiopia is the central bank of Ethiopia. Its headquarters are in the capital city of Addis Ababa. Mamo Mihretu is the current governor of the bank.

The Reserve Bank of Fiji is the central bank of the Pacific island country of Fiji. Its responsibilities include the issue of currency, control of the money supply, currency exchange, monetary stability, promotion of sound finances, and fostering economic development.

The Central Bank of The Bahamas is the reserve bank of The Bahamas based in the capital Nassau.

The Nepal Rastra Bank was established April 26, 1956 A.D. under the Nepal Rastra Bank Act, 1955, to discharge the central banking responsibilities including guiding the development of the embryonic domestic financial sector. As of now, the NRB is functioning under the new Nepal Rastra Bank Act, 2002. The functions of NRB are to formulate required monetary and foreign exchange policies so as to maintain the stability in market prices, to issue currency notes, to regulate and supervise the banking and financial sector, to develop efficient payment and banking systems among others. The NRB is also the economic advisor to the government of Nepal. As the central bank of Nepal, it is the monetary, supervisory and regulatory body of all the commercial banks. development banks, finance companies and micro-finances institutions.

Monetary policy in the United States is associated with interest rates and availability of credit.