The Federal Reserve System is the central banking system of the United States. It was created on December 23, 1913, with the enactment of the Federal Reserve Act, after a series of financial panics led to the desire for central control of the monetary system in order to alleviate financial crises. Over the years, events such as the Great Depression in the 1930s and the Great Recession during the 2000s have led to the expansion of the roles and responsibilities of the Federal Reserve System.

The Federal Reserve Act was passed by the 63rd United States Congress and signed into law by President Woodrow Wilson on December 23, 1913. The law created the Federal Reserve System, the central banking system of the United States.

An interest rate is the amount of interest due per period, as a proportion of the amount lent, deposited, or borrowed. The total interest on an amount lent or borrowed depends on the principal sum, the interest rate, the compounding frequency, and the length of time over which it is lent, deposited, or borrowed.

The monetary policy of the United States is the set of policies which the Federal Reserve follows to achieve its twin objectives of high employment and stable inflation.

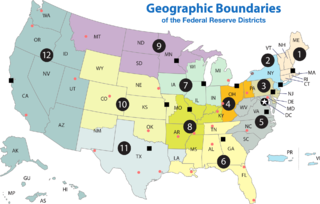

A Federal Reserve Bank is a regional bank of the Federal Reserve System, the central banking system of the United States. There are twelve in total, one for each of the twelve Federal Reserve Districts that were created by the Federal Reserve Act of 1913. The banks are jointly responsible for implementing the monetary policy set forth by the Federal Open Market Committee, and are divided as follows:

In public finance, a lender of last resort (LOLR) is the institution in a financial system that acts as the provider of liquidity to a financial institution which finds itself unable to obtain sufficient liquidity in the interbank lending market when other facilities or such sources have been exhausted. It is, in effect, a government guarantee to provide liquidity to financial institutions. Since the beginning of the 20th century, most central banks have been providers of lender of last resort facilities, and their functions usually also include ensuring liquidity in the financial market in general.

In the United States, federal funds are overnight borrowings between banks and other entities to maintain their bank reserves at the Federal Reserve. Banks keep reserves at Federal Reserve Banks to meet their reserve requirements and to clear financial transactions. Transactions in the federal funds market enable depository institutions with reserve balances in excess of reserve requirements to lend reserves to institutions with reserve deficiencies. These loans are usually made for one day only, that is, "overnight". The interest rate at which these transactions occur is called the federal funds rate. Federal funds are not collateralized; like eurodollars, they are an unsecured interbank loan.

The discount window is an instrument of monetary policy that allows eligible institutions to borrow money from the central bank, usually on a short-term basis, to meet temporary shortages of liquidity caused by internal or external disruptions.

The Federal Reserve Bank of St. Louis is one of 12 regional Reserve Banks that, along with the Board of Governors in Washington, D.C., make up the United States' central bank. Missouri is the only state to have two main Federal Reserve Banks.

The Federal Reserve Bank of Atlanta,, is the sixth district of the 12 Federal Reserve Banks of the United States and is headquartered in midtown Atlanta, Georgia.

Bank rate, also known as discount rate in American English, and (familiarly) the base rate in British English, is the rate of interest which a central bank charges on its loans and advances to a commercial bank. The bank rate is known by a number of different terms depending on the country, and has changed over time in some countries as the mechanisms used to manage the rate have changed.

The American subprime mortgage crisis was a multinational financial crisis that occurred between 2007 and 2010 that contributed to the 2007–2008 global financial crisis. The crisis led to a severe economic recession, with millions losing their jobs and many businesses going bankrupt. The U.S. government intervened with a series of measures to stabilize the financial system, including the Troubled Asset Relief Program (TARP) and the American Recovery and Reinvestment Act (ARRA).

The United States Federal Reserve System is the central banking system of the United States. It was created on December 23, 1913.

The U.S. central banking system, the Federal Reserve, in partnership with central banks around the world, took several steps to address the subprime mortgage crisis. Federal Reserve Chairman Ben Bernanke stated in early 2008: "Broadly, the Federal Reserve’s response has followed two tracks: efforts to support market liquidity and functioning and the pursuit of our macroeconomic objectives through monetary policy." A 2011 study by the Government Accountability Office found that "on numerous occasions in 2008 and 2009, the Federal Reserve Board invoked emergency authority under the Federal Reserve Act of 1913 to authorize new broad-based programs and financial assistance to individual institutions to stabilize financial markets. Loans outstanding for the emergency programs peaked at more than $1 trillion in late 2008."

The Emergency Economic Stabilization Act of 2008, also known as the "bank bailout of 2008" or the "Wall Street bailout", was a United States federal law enacted during the Great Recession, which created federal programs to "bail out" failing financial institutions and banks. The bill was proposed by Treasury Secretary Henry Paulson, passed by the 110th United States Congress, and was signed into law by President George W. Bush. It became law as part of Public Law 110-343 on October 3, 2008. It created the $700 billion Troubled Asset Relief Program (TARP), which utilized congressionally appropriated taxpayer funds to purchase toxic assets from failing banks. The funds were mostly redirected to inject capital into banks and other financial institutions while the Treasury continued to examine the usefulness of targeted asset purchases.

The interbank lending market is a market in which banks lend funds to one another for a specified term. Most interbank loans are for maturities of one week or less, the majority being overnight. Such loans are made at the interbank rate. A sharp decline in transaction volume in this market was a major contributing factor to the collapse of several financial institutions during the financial crisis of 2007–2008.

The Term Asset-Backed Securities Loan Facility (TALF) is a program created by the U.S. Federal Reserve to spur consumer credit lending. The program was announced on November 25, 2008, and was to support the issuance of asset-backed securities (ABS) collateralized by student loans, auto loans, credit card loans, and loans guaranteed by the Small Business Administration (SBA). Under TALF, the Federal Reserve Bank of New York authorized up to $200 billion of loans on a non-recourse basis to holders of certain AAA-rated ABS backed by newly and recently originated consumer and small business loans. As TALF money did not originate from the U.S. Treasury, the program did not require congressional approval to disburse funds, but an act of Congress forced the Fed to reveal how it lent the money. The TALF began operation in March 2009 and was closed on June 30, 2010. TALF 2 was initiated in 2020 during the COVID-19 pandemic.

United States policy responses to the late-2000s recession explores legislation, banking industry and market volatility within retirement plans.

Bloomberg L.P. v. Board of Governors of the Federal Reserve System, 1:08-cv-09595, was a lawsuit by Bloomberg L.P. against the Board of Governors of the Federal Reserve System for disclosure of information about banks and other financial institutions that had borrowed from the Federal Reserve discount window during the United States housing bubble and ensuing financial crisis.

The real bills doctrine says that as long as bankers lend to businessmen only against the security (collateral) of short-term 30-, 60-, or 90-day commercial paper representing claims to real goods in the process of production, the loans will be just sufficient to finance the production of goods. The doctrine seeks to have real output determine its own means of purchase without affecting prices. Under the real bills doctrine, there is only one policy role for the central bank: lending commercial banks the necessary reserves against real customer bills, which the banks offer as collateral. The term "real bills doctrine" was coined by Lloyd Mints in his 1945 book, A History of Banking Theory. The doctrine was previously known as "the commercial loan theory of banking".