Related Research Articles

Microeconomics is a branch of economics that studies the behavior of individuals and firms in making decisions regarding the allocation of scarce resources and the interactions among these individuals and firms.

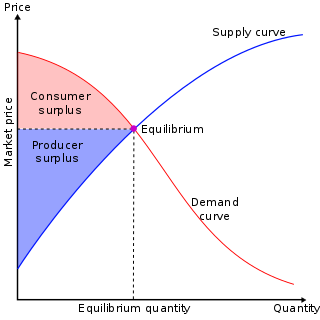

In microeconomics, supply and demand is an economic model of price determination in a market. It postulates that, holding all else equal, in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded will equal the quantity supplied, resulting in an economic equilibrium for price and quantity transacted. It forms the theoretical basis of modern economics.

In mainstream economics, economic surplus, also known as total welfare or Marshallian surplus, refers to two related quantities:

In economics, elasticity measures the percentage change of one economic variable in response to a change in another. If a good's price elasticity of demand is -2, a 10% increase in price causes the quantity demanded to fall 20%.

A good's price elasticity of demand is a measure of how sensitive the quantity demanded is to its price. When the price rises, quantity demanded falls for almost any good, but it falls more for some than for others. The price elasticity gives the percentage change in quantity demanded when there is a one percent increase in price, holding everything else constant. If the elasticity is -2, that means a one percent price rise leads to a two percent decline in quantity demanded. Other elasticities measure how the quantity demanded changes with other variables.

The theory of consumer choice is the branch of microeconomics that relates preferences to consumption expenditures and to consumer demand curves. It analyzes how consumers maximize the desirability of their consumption as measured by their preferences subject to limitations on their expenditures, by maximizing utility subject to a consumer budget constraint.

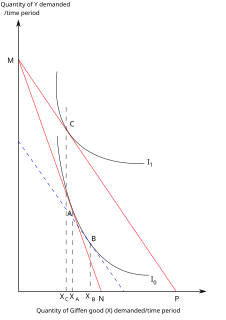

In economics and consumer theory, a Giffen good is a product that people consume more of as the price rises and vice versa—violating the basic law of demand in microeconomics. For any other sort of good, as the price of the good rises, the substitution effect makes consumers purchase less of it, and more of substitute goods; for most goods, the income effect reinforces this decline in demand for the good. But a Giffen good is so strongly an inferior good in the minds of consumers that this contrary income effect more than offsets the substitution effect, and the net effect of the good's price rise is to increase demand for it. Also known as Giffen paradox. A Giffen good is considered to be the opposite of an ordinary good.

In economics, an inferior good is a good whose demand decreases when consumer income rises, unlike normal goods, for which the opposite is observed. Normal goods are those goods for which the demand rises as consumer income rises.

In economics, a normal good is a type of a good which experiences an increase in demand due to an increase in income. When there is an increase in a person's income, for example due to a wage rise, a good for which the demand rises due to the wage increase, is referred as a normal good. Conversely, the demand for normal goods declines when the income decreases, for example due to a wage decrease or layoffs.

A Veblen good is a type of luxury good for which the demand for a good increases as the price increases, in apparent contradiction of the law of demand, resulting in an upward-sloping demand curve. The higher prices of Veblen goods may make them desirable as a status symbol in the practices of conspicuous consumption and conspicuous leisure. A product may be a Veblen good because it is a positional good, something few others can own.

In economics and particularly in consumer choice theory, the income-consumption curve is a curve in a graph in which the quantities of two goods are plotted on the two axes; the curve is the locus of points showing the consumption bundles chosen at each of various levels of income.

In microeconomics, the law of demand is a fundamental principle which states that there is an inverse relationship between price and quantity demanded. In other words, "conditional on all else being equal, as the price of a good increases (↑), quantity demanded will decrease (↓); conversely, as the price of a good decreases (↓), quantity demanded will increase (↑)". Alfred Marshall worded this as: "When then we say that a person's demand for anything increases, we mean that he will buy more of it than he would before at the same price, and that he will buy as much of it as before at a higher price". The law of demand, however, only makes a qualitative statement in the sense that it describes the direction of change in the amount of quantity demanded but not the magnitude of change.

In economics, a demand curve is a graph depicting the relationship between the price of a certain commodity and the quantity of that commodity that is demanded at that price. Demand curves can be used either for the price-quantity relationship for an individual consumer, or for all consumers in a particular market.

Utility maximization was first developed by utilitarian philosophers Jeremy Bentham and John Stewart Mill. In microeconomics, the utility maximization problem is the problem consumers face: "How should I spend my money in order to maximize my utility?" It is a type of optimal decision problem. It consists of choosing how much of each available good or service to consume, taking into account a constraint on total spending (income), the prices of the goods and their preferences.

The Slutsky equation in economics, named after Eugen Slutsky, relates changes in Marshallian (uncompensated) demand to changes in Hicksian (compensated) demand, which is known as such since it compensates to maintain a fixed level of utility.

In microeconomics, a consumer's Hicksian demand function or compensated demand function for a good is his quantity demanded as part of the solution to minimizing his expenditure on all goods while delivering a fixed level of utility. The function is named after John Hicks.

In economics, partial equilibrium is a condition of economic equilibrium which analyzes only a single market,Ceteris paribus (everything else remaining constant]] except for the one change at a time being analyzed. In general equilibrium analysis, on the other hand, the prices and quantities of all markets in the economy are considered simultaneously, including feedback effects from one to another, though the assumption of ceteris paribus is maintained with respect to such things as constancy of tastes and technology.

In economics, demand is the quantity of a good that consumers are willing and able to purchase at various prices during a given period of time. The relationship between price and quantity demanded is also called the demand curve. Demand for a specific item is a function of an item's perceived necessity, price, perceived quality, convenience, available alternatives, purchasers' disposable income and tastes, and many other factors.

An aggregate in economics is a summary measure. The aggregation problem is the difficult problem of finding a valid way to treat an empirical or theoretical aggregate as if it reacted like a less-aggregated measure, say, about behavior of an individual agent as described in general microeconomic theory. Examples of aggregates in micro- and macroeconomics relative to less aggregated counterparts are:

In economics, the income elasticity of demand is the responsivenesses of the quantity demanded for a good to a change in consumer income. It is measured as the ratio of the percentage change in quantity demanded to the percentage change in income. If a 10% increase in Mr. Ruskin Smith's income causes him to buy 20% more bacon, Smith's income elasticity of demand for bacon is 20%/10% = 2.

References

- Hal Varian, Intermediate Microeconomics: A Modern Approach, Sixth Edition, chapter 6

| | This article related to microeconomics is a stub. You can help Wikipedia by expanding it. |