The Central Bank of Ireland in Dublin's IFSC. Then Governor Philip Lane chaired the Economic Statistics Review Group which published a report in 2016 recommending the creation of Modified Gross National Income.

Modified gross national income (also Modified GNI or GNI*) is a metric used by the Central Statistics Office (Ireland) to measure the Irish economy rather than GNI or GDP. GNI* is GNI minus the depreciation on Intellectual Property, depreciation on leased aircraft and the net factor income of redomiciled PLCs.

While "Inflated GDP-per-capita" due to BEPS tools is a feature of tax havens,[1][2] Ireland was the first to adjust its GDP metrics. Economists, including Eurostat,[3] noted Irish Modified GNI (GNI*) is still distorted by Irish BEPS tools and US multinational tax planning activities in Ireland (e.g. contract manufacturing); and that Irish BEPS tools distort aggregate EU-28 data,[4] and the EU-US trade deficit.[5]

In August 2018, the Central Statistics Office (Ireland) (CSO) restated table of Irish GDP versus Modified GNI (2009–2017) showed GDP was 162% of GNI* (EU-28 2017 GDP was 100% of GNI).[6] Ireland's public §2018 Debt metrics differ dramatically depending on whether Debt-to-GDP, Debt-to-GNI* or Debt-per-Capita is used.[7]

The distorted GNI to GDP ratio in some EU states indicates a profound disproportionality in corporate havens as Ireland and Luxembourg.

In February 1994, tax academic James R. Hines Jr., identified Ireland as one of seven major tax havens in his 1994 Hines-Rice paper,[10] still[as of?] the most cited paper in research on tax havens.[11] Hines noted that the profit shifting tools of US multinationals in corporate-focused tax havens distorted the national economic statistics of the haven as the scale of the profit shifting was disproportionate to haven's economy. An elevated GDP-per-capita became a "proxy indicator" of a tax haven.[2]

In November 2005, the Wall Street Journal reported that US technology and life sciences multinationals (e.g. Microsoft), were using an Irish base erosion and profit shifting ("BEPS") tool called the double Irish, to minimise their corporate taxes.[12][13] Designed by PwC (Ireland) tax partner, Feargal O'Rourke,[14][15] the double Irish would become the largest BEPS tool in history, and would enable US multinationals to accumulate over US$1 trillion in untaxed offshore profits.[16]

The accounting flows of BEPS tools can appear in national economic statistics, varying with each tool, but without contributing to the economy of the tax haven.[2]

Subsequent US Senate (2013), and EU Commission (2014–2016) investigations, into Apple's Irish tax structure, would show that starting in 2004, Apple's Irish subsidiary, Apple Sales International ("ASI"), would almost double the untaxed profits shifted through its double Irish BEPS tool every year, for a decade.[17]

Table 1: Estimate of profits shifted through Apple's Irish subsidiary, Apple Sales International ("ASI"), 2004–2014.[17]

Year

ASI profit shifted (USD m)

Average €/$ rate

ASI profit shifted (EUR m)

Irish corp. tax rate

Irish corp. tax avoided (EUR m)

2004

268

.805

216

12.5%

27

2005

725

.804

583

12.5%

73

2006

1,180

.797

940

12.5%

117

2007

1,844

.731

1,347

12.5%

168

2008

3,127

.683

2,136

12.5%

267

2009

4,003

.719

2,878

12.5%

360

2010

12,095

.755

9,128

12.5%

1,141

2011

21,855

.719

15,709

12.5%

1,964

2012

35,877

.778

27,915

12.5%

3,489

2013

32,099

.753

24,176

12.5%

3,022

2014

34,229

.754

25,793

12.5%

3,224

Total

147,304

110,821

13,853

From 2003 to 2007, research has shown that inflated Irish GDP from US multinational BEPS tools,[18] amplified the Irish Celtic Tiger period by stimulating Irish consumer optimism, who increased borrowing to OECD record levels; and global capital markets optimism about Ireland enabling Irish banks to borrow 180% of Irish deposits.[19]

This unwound in the economic crisis as global capital markets, who had ignored Ireland's deteriorating credit metrics and distorted GDP data when Irish GDP was rising, withdrew and precipitated an Irish property and banking collapse in 2009–2012.[18][20]

The 2009–2012 Irish economic collapse led to a transfer of indebtedness from the Irish private sector balance sheet, the most leveraged in the OECD with household debt-to-income at 190%, to the Irish public sector balance sheet, which was almost unleveraged pre-crisis. This was done via Irish bank bailouts and public deficit spending.[21][22]

Dominance of US companies: Irish corporate Gross Operating Surplus (i.e. profits), by the controlling country of the company (note: a material part of the Irish figure is also from US tax inversions who are US-controlled). Eurostat (2015).

During the Irish financial crisis from 2009 to 2012, two catalysts would restart the distortion of Irish economic statistics:

Irish-based US technology firms such as Apple and Google entered a stronger phase of growth; for example, in 2007, Apple's Irish ASI subsidiary was profit shifting just under USD 2 billion of untaxed global income through its hybrid-double Irish BEPS tool, however by 2012, ASI was profit shifting just under USD 36 billion of untaxed global income through Ireland, although only a small amount of this BEPS tool appeared in Irish GDP.[17]

In 2010, Hines published a new list of 52 global tax havens, the Hines 2010 list, which ranked Ireland as the 3rd largest tax haven in the world.[26]

By 2011, Eurostat showed that Ireland's ratio of GNI to GDP, had fallen to 80% (i.e. Irish GDP was 125% of Irish GNI, or artificially inflated by 25%). Only Luxembourg, who ranked 1st on Hines' 2010 list of global tax havens,[26] was lower at 73% (i.e. Luxembourg GDP was 137% of Luxembourg GNI). Eurostat's GNI/GDP table (see graphic) showed EU GDP is equal to EU GNI for almost every EU country, and for the aggregate EU-27 average.[18][27]

In 2013–2015 several large US life sciences multinationals executed tax inversions to Ireland (e.g. Medtronic). Ireland became the largest recipient of US corporate tax inversions in history.[28] The Irish BEPS tool enabled US multinationals to avoid almost all Irish corporate taxes, however, unlike other Irish BEPS tools, it registers fully in Irish economic statistics.[29] In April 2016, the Obama Administration blocked the proposed US$160 billion proposed Pfizer-Allergan Irish inversion.[30]

A 2015 EU Commission report into Ireland's economic statistics, showed that from 2010 to 2015, almost 23% of Ireland's GDP was now represented by untaxed multinational net royalty payments, thus implying that Irish GDP was now circa 130% of Irish GNI.[31] This analysis, however, did not capture the full effect of the BEPS tool as it uses capital allowances, rather than royalty payments, to execute the BEPS movement. The Irish media were also confused as to Ireland's state of indebtedness as Irish Debt-per-Capita diverged sharply from Irish Debt-to GDP.[32][33][34]

By 2012–14, Apple's Irish subsidiary, ASI, was profit shifting circa US$35 billion per annum through Ireland, equivalent to 20% of Irish GDP, via its hybrid-double Irish BEPS tool.[17] However, this particular BEPS tool had a modest impact on Irish GDP data. In late 2014, to limit further exposure to fines from the EU Commission's investigation into Apple's Irish tax schemes, Apple closed its hybrid-double Irish BEPS tool,[35] and decided to swap into the BEPS tool.[36][37] In Q1 2015, Apple Ireland purchased circa US$300 billion of virtual IP assets owned by Apple Jersey, executing the largest BEPS action in history.[17][38]

Ireland: Apple's Q1 2015 IP distortion of Ireland's balance of payments. Brad Setser & Cole Frank (Council on Foreign Relations)

The BEPS tool is recorded like a tax inversion in the Irish national accounts.[38] Because Apple's IP was now on-shored in Ireland, all of ASI's circa US$40 billion in profit shifting for 2015, appeared in 2015 Irish GDP and GNP, despite the fact that new BEPS tool would limit Apple's exposure to Irish corporation tax.

In July 2016, the Irish Central Statistice Office announced 2015 Irish economic growth rates of 26.3% (GDP) and 18.7% (GNP), as a result of Apple's restructuring.[39] The announcement led to ridicule,[40][41][42][43][44][45][46] and was labelled by Nobel Prize economist Paul Krugman as "leprechaun economics".[47]

Finance Minister Michael Noonan who removed the "cap" on the Irish "capital allowances for intangibles" BEPS tool in 2015, to remove any potential Irish corporate tax liability from Apple's Q1 2015 restructuring

From July 2016 to July 2018, the Central Statistics Office refused to identify the source of leprechaun economics, and suppressed the release of other economic data to protect Apple's identity under the 1993 Central Statistics Act,[48][49] in the manner of a "captured state", further damaging confidence in Ireland.[50]

By early 2017, research in the Sloan School of Management in the Massachusetts Institute of Technology, using the limited data released by the Irish CSO, could conclude: While corporate inversions and aircraft leasing firms were credited for increasing Irish [2015] GDP, the impact may have been exaggerated.[51] The same research noted that capital markets did not consider Irish macro economic statistics to be credible or meaningful, as evidenced by the lack of any reaction by the capital markets to Ireland's 26.3% GDP growth (both on the day of release, and in the subsequent days).[51]

Where as the Obama Administration blocked the proposed US$160 billion Pfizer-Allergan Irish inversion in 2016, Apple's larger US$300 billion Irish inversion was ignored. It is not clear if this was due to the confusion caused by the Central Statistics Office (Ireland) in protecting Apple's identity for 2 years, or other reasons.

2017 GNI* response

Nobel Prize-winning US economist Paul Krugman whose tweet on the 12 July 2016 christened the Irish "Leprechaun economics" affair and precipitated the creation of "Modified gross national income", or GNI*

In September 2016, as a direct result of the "leprechaun economics" affair, the Governor of the Central Bank of Ireland ("CBI"), Philip R. Lane, chaired a special cross-economic steering group, the Economic Statistics Review Group ("ESRG"), of stakeholders (incl. CBI, IFAC, ESRI, NTMA, leading academics and the Department of Finance), to recommend new economic statistics that would better represent the true position of the Irish economy.[52]

In February 2017, a new metric, "Modified Gross National Income" (or GNI* for short) was announced. The difference between GNI* and GNI is due to having to deal with two problems (a) The retained earnings of re-domiciled firms in Ireland (where the earnings ultimately accrue to foreign investors), and (b) depreciation on foreign-owned capital assets located in Ireland, such as intellectual property (which inflate the size of Irish GDP, but again the benefits accrue to foreign investors).[53][54]

Irish GNI less the effects of the profits of re-domiciled companies and the depreciation of intellectual property products and aircraft leasing companies.[55]

In February 2017, the CSO stated they would continue to calculate and release Irish GDP and Irish GNP to meet their EU and other International statistical reporting commitments.[56] In July 2017, the CSO estimated that 2016 Irish GNI* (€190bn) was 30% below Irish GDP (€275bn), or that Irish GDP is 143% above Irish GNI*. The CSO also confirmed that Irish Net Public Debt-to-GNI* was 106% (Irish Net Public Debt-to-GDP, post leprechaun economics, was 73%).[57][58]

In December 2017, Eurostat noted that while GNI* was helpful, it was still being artificially inflated by BEPS flows, and the BEPS activities of certain types of contract manufacturing in particular;[3] a view shared by several others.[18][59][60][61][62][63] There have been several material revisions to Irish 2015 GDP in particular (as per §Irish GDP versus Modified GNI (2009–2017).[64] Modified GNI, or GNI*, was adopted by the IMF and OECD in their 2017 Ireland Country Reports.[65][66]

Economists noted in May 2018 that distorted Irish economic data was calling into question the credibility of Eurostat's aggregate EU-28 economic data.[4]

In June 2018, tax academic Gabriel Zucman, using 2015 economic data, claimed Irish BEPS tools had made Ireland the world's largest tax haven (Zucman-Tørsløv-Wier 2018 list).[67][68] Zucman also showed that Irish BEPS flows were becoming so large, that they were artificially exaggerating the scale of the EU-US trade deficit.[5]

Another study published in June 2018 by the IMF called into question the economic data of all leading tax havens, and the artificial effect of their BEPS tools.[1][69]

Irish public debt-to-GDP and public debt-to-GNI* from 2000 to 2017

The issues post leprechaun economics, and "modified GNI", are captured on page 34 of the OECD 2018 Ireland survey:[66]

On a gross public debt-to-GDP basis, Ireland's 2015 figure at 78.8% is not of concern;

On a gross public debt-to-GNI* basis, Ireland's 2015 figure at 116.5% is more serious, but not alarming;

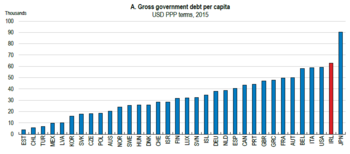

On a gross public debt-per-capita basis, Ireland's 2015 figure at over $62,686 per capita, is the second highest in the OECD, after Japan.[71]

There is concern Ireland repeats the mistakes of the "Celtic Tiger" era, and over-leverages again, against distorted Irish economic data.[59] Given the transfer of Irish private sector debt to the Irish public balance sheet from the Irish 2009–2012 financial crisis, it will not be possible to bail out the Irish banking system again.

OECD Public Debt-per-Capita table for 2015

In June 2017, the Irish Fiscal Advisory Council benchmarked Irish public debt against Irish tax revenues (similar to the debt-to-EBITDA ratio used in capital markets). Ireland's 2016 gross public debt-to-tax revenues was 282.9%, the 4th highest in the EU-28 (after Greece, Portugal, and Cyprus).[72][73][74]

In November 2017, the Central Bank of Ireland benchmarked Irish private debt against Irish disposable income. Ireland's 2016 private debt as a% of Irish disposable income was 141.6%, the 4th highest in the EU-28 (after Netherlands, Denmark and Sweden).[75][76]

These two initiatives show Ireland's high public debt levels, and Ireland's high private sector debt levels, imply that on a "total debt" basis (i.e. Irish public debt plus Irish private debt), Ireland is likely one of the most indebted of the EU-27 countries when benchmarked on a GNI*-type basis; hence the importance of a GNI* metric.[citation needed]

Irish GDP versus Modified GNI (2009–2018)

Irish National Income and Expenditure 2017 (measured in 2018 euros) 2009–2017[6][77][78][79]

Corporate haven, corporate tax haven, or multinational tax haven is used to describe a jurisdiction that multinational corporations find attractive for establishing subsidiaries or incorporation of regional or main company headquarters, mostly due to favourable tax regimes, and/or favourable secrecy laws, and/or favourable regulatory regimes.

The Central Bank of Ireland is the Irish member of the Eurosystem and had been the monetary authority for Ireland from 1943 to 1998, issuing the Irish pound. It is also the country's main financial regulatory authority, and since 2014 has been Ireland's national competent authority within European Banking Supervision.

IDA Ireland is the agency responsible for the attraction and retention of inward foreign direct investment (FDI) into Ireland. The agency was founded in 1949 as the Industrial Development Authority and placed on a statutory footing a year later. In 1969 it became a non-commercial autonomous state-sponsored body. Today it is a semi-state body that plays an important role in Ireland's relationship with foreign investors, with multinationals accounting for 10.2% of employment and 66% of Irish exports. The agency partners with investors to help them to begin or expand their operations in the Irish market. It provides funding support to research and development projects, and has a number of direct support mechanisms, including employment and training grants.

Margrethe Vestager is a Danish politician currently serving as Executive Vice President of the European Commission for A Europe Fit for the Digital Age since December 2019 and European Commissioner for Competition since 2014. Vestager is a member of the Danish Social Liberal Party, and of the Alliance of Liberals and Democrats for Europe Party (ALDE) on the European level.

Ireland's Corporate Tax System is a central component of Ireland's economy. In 2016–17, foreign firms paid 80% of Irish corporate tax, employed 25% of the Irish labour force, and created 57% of Irish OECD non-farm value-add. As of 2017, 25 of the top 50 Irish firms were U.S.–controlled businesses, representing 70% of the revenue of the top 50 Irish firms. By 2018, Ireland had received the most U.S. § Corporate tax inversions in history, and Apple was over one–fifth of Irish GDP. Academics rank Ireland as the largest tax haven; larger than the Caribbean tax haven system.

A tax haven is a term, often used pejoratively, to describe a place with very low tax rates for non-domiciled investors, even if the official rates may be higher.

The economy of the Republic of Ireland is a highly developed knowledge economy, focused on services in high-tech, life sciences, financial services and agribusiness, including agrifood. Ireland is an open economy, and ranks first for high-value foreign direct investment (FDI) flows. In the global GDP per capita tables, Ireland ranks 2nd of 192 in the IMF table and 4th of 187 in the World Bank ranking. Among OECD nations, Ireland has a highly efficient and strong social security system; social expenditure stood at roughly 13.4% of GDP.

A tax inversion or corporate tax inversion is a form of tax avoidance where a corporation restructures so that the current parent is replaced by a foreign parent, and the original parent company becomes a subsidiary of the foreign parent, thus moving its tax residence to the foreign country. Executives and operational headquarters can stay in the original country. The US definition requires that the original shareholders remain a majority control of the post-inverted company. In US federal legislation a company which has been restructured in this manner is referred to as an "inverted domestic corporation", and the term "corporate expatriate" is also used.

An offshore financial centre (OFC) is defined as a "country or jurisdiction that provides financial services to nonresidents on a scale that is incommensurate with the size and the financing of its domestic economy."

The Double Irish arrangement was a base erosion and profit shifting (BEPS) corporate tax avoidance tool used mainly by United States multinationals since the late 1980s to avoid corporate taxation on non-U.S. profits. It was the largest tax avoidance tool in history. By 2010, it was shielding US$100 billion annually in US multinational foreign profits from taxation, and was the main tool by which US multinationals built up untaxed offshore reserves of US$1 trillion from 2004 to 2018. Traditionally, it was also used with the Dutch Sandwich BEPS tool; however, 2010 changes to tax laws in Ireland dispensed with this requirement.

The Financial Secrecy Index (FSI) is a report published by the advocacy organization Tax Justice Network (TJN) which ranks countries by financial secrecy indicators, weighted by the economic flows of each country.

Base erosion and profit shifting (BEPS) refers to corporate tax planning strategies used by multinationals to "shift" profits from higher-tax jurisdictions to lower-tax jurisdictions or no-tax locations where there is little or no economic activity, thus "eroding" the "tax-base" of the higher-tax jurisdictions using deductible payments such as interest or royalties. For the government, the tax base is a company's income or profit. Tax is levied as a percentage on this income/profit. When that income / profit is transferred to a tax haven, the tax base is eroded and the company does not pay taxes to the country that is generating the income. As a result, tax revenues are reduced and the country is disadvantaged. The Organisation for Economic Co-operation and Development (OECD) define BEPS strategies as "exploiting gaps and mismatches in tax rules". While some of the tactics are illegal, the majority are not. Because businesses that operate across borders can utilize BEPS to obtain a competitive edge over domestic businesses, it affects the righteousness and integrity of tax systems. Furthermore, it lessens deliberate compliance, when taxpayers notice multinationals legally avoiding corporate income taxes. Because developing nations rely more heavily on corporate income tax, they are disproportionately affected by BEPS.

Dutch Sandwich is a base erosion and profit shifting (BEPS) corporate tax tool, used mostly by U.S. multinationals to avoid incurring European Union withholding taxes on untaxed profits as they were being moved to non-EU tax havens. These untaxed profits could have originated from within the EU, or from outside the EU, but in most cases were routed to major EU corporate-focused tax havens, such as Ireland and Luxembourg, by the use of other BEPS tools. The Dutch Sandwich was often used with Irish BEPS tools such as the Double Irish, the Single Malt and the Capital Allowances for Intangible Assets ("CAIA") tools. In 2010, Ireland changed its tax-code to enable Irish BEPS tools to avoid such withholding taxes without needing a Dutch Sandwich.

Leprechaun economics was a term coined by economist Paul Krugman to describe the 26.3 per cent rise in Irish 2015 GDP, later revised to 34.4 per cent, in a 12 July 2016 publication by the Irish Central Statistics Office (CSO), restating 2015 Irish national accounts. At that point, the distortion of Irish economic data by tax-driven accounting flows reached a climax. In 2020, Krugman said the term was a feature of all tax havens.

Conduit OFC and sink OFC is an empirical quantitative method of classifying corporate tax havens, offshore financial centres (OFCs) and tax havens.

Apple's EU tax dispute refers to an investigation by the European Commission into tax arrangements between Apple and Ireland, which allowed the company to pay close to zero corporate tax over 10 years.

Ireland has been labelled as a tax haven or corporate tax haven in multiple financial reports, an allegation which the state has rejected in response. Ireland is on all academic "tax haven lists", including the § Leaders in tax haven research, and tax NGOs. Ireland does not meet the 1998 OECD definition of a tax haven, but no OECD member, including Switzerland, ever met this definition; only Trinidad & Tobago met it in 2017. Similarly, no EU–28 country is amongst the 64 listed in the 2017 EU tax haven blacklist and greylist. In September 2016, Brazil became the first G20 country to "blacklist" Ireland as a tax haven.

Qualifying Investor Alternative Investment Fund or QIAIF is a Central Bank of Ireland regulatory classification established in 2013 for Ireland's five tax-free legal structures for holding assets. The Irish Collective Asset-management Vehicle or ICAV is the most popular of the five Irish QIAIF structures, it is the main tax-free structure for foreign investors holding Irish assets. A QIAIF constitutes an alternative investment fund (AIF) under the Alternative Investment Fund Managers Directive (AIFMD) and is required to appoint an alternative investment fund manager (AIFM). The AIFM may be either an EU manager or a non-EU manager.

James R. Hines Jr. is an American economist and a founder of academic research into corporate-focused tax havens, and the effect of U.S. corporate tax policy on the behaviors of U.S. multinationals. His papers were some of the first to analyse profit shifting, and to establish quantitative features of tax havens. Hines showed that being a tax haven could be a prosperous strategy for a jurisdiction, and controversially, that tax havens can promote economic growth. Hines showed that use of tax havens by U.S. multinationals had maximized long-term U.S. exchequer tax receipts, at the expense of other jurisdictions. Hines is the most cited author on the research of tax havens, and his work on tax havens was relied upon by the CEA when drafting the Tax Cuts and Jobs Act of 2017.

References

1 2 JANNICK DAMGAARD; THOMAS ELKJAER; NIELS JOHANNESEN (June 2018). "Piercing the Veil of Tax Havens". International Monetary Fund: Finance & Development Quarterly. 55 (2). Archived from the original on 12 June 2018. Retrieved 12 June 2018. The eight major pass-through economies—the Netherlands, Luxembourg, Hong Kong SAR, the British Virgin Islands, Bermuda, the Cayman Islands, Ireland, and Singapore—host more than 85 percent of the world's investment in special purpose entities, which are often set up for tax reasons.

1 2 3 SILKE STAPEL-WEBER; JOHN VERRINDER (December 2017). "Globalisation at work in statistics — Questions arising from the 'Irish case'"(PDF). EuroStat. p.31. Archived(PDF) from the original on 28 April 2018. Retrieved 22 August 2018. Nevertheless the rise in [Irish] GNI* is still very substantial because the additional income flows of the companies (interest and dividends) concerned are considerably smaller than the value added of their activities

1 2 Brad Setser (11 May 2018). "Ireland Exports its Leprechaun". Council on Foreign Relations. Archived from the original on 14 May 2018. Retrieved 13 May 2018. Ireland has, more or less, stopped using GDP to measure its own economy. And on current trends [because Irish GDP is distorting EU-28 aggregate data], the eurozone taken as a whole may need to consider something similar.

1 2 Gabriel Zucman; Thomas Tørsløv; Ludvig Wier (8 June 2018). "The Missing Profits of Nations∗"(PDF). National Bureau of Economic Research, Working Papers. p.25. Archived(PDF) from the original on 2 August 2018. Retrieved 23 August 2018. Profit shifting also has a significant effect on trade balances. For instance, after accounting for profit shifting, Japan, the U.K., France, and Greece turn out to have trade surpluses in 2015, in contrast to the published data that record trade deficits. According to our estimates, the true trade deficit of the United States was 2.1% of GDP in 2015, instead of 2.8% in the official statistics—that is, a quarter of the recorded trade deficit of the United States is an illusion of multinational corporate tax avoidance.

↑ James R. Hines Jr.; Eric M. Rice (February 1994). "FISCAL PARADISE: FOREIGN TAX HAVENS AND AMERICAN BUSINESS"(PDF). Quarterly Journal of Economics (Harvard/MIT). 9 (1). Archived from the original(PDF) on 25 August 2017. Retrieved 22 August 2018. We identify 41 countries and regions as tax havens for the purposes of U.S. businesses. Together the seven tax havens with populations greater than one million (Hong Kong, Ireland, Liberia, Lebanon, Panama, Singapore, and Switzerland) account for 80 percent of total tax haven population and 89 percent of tax haven GDP.

↑ "Irish Subsidiary Lets Microsoft Slash Taxes in U.S. and Europe". Wall Street Journal. 7 November 2005. Archived from the original on 16 June 2018. Retrieved 23 August 2018. Round Island's legal address is in the headquarters of a Dublin law firm, Matheson Ormsby Prentice, that advertises its expertise in helping multinational companies use Ireland to shelter income from taxes.

↑ Seamus Coffey, Irish Fiscal Advisory Council (18 June 2018). "Who shifts profits to Ireland". Economic Incentives, University College Cork. Archived from the original on 20 November 2018. Retrieved 20 November 2018. Eurostat's structural business statistics give a range of measures of the business economy broken down by the controlling country of the enterprises. Here is the Gross Operating Surplus generated in Ireland in 2015 for the countries with figures reported by Eurostat.

↑ Daly, Frank; Arnold, Tom; Burke, Julie; Collins, Micheál; Convery, Frank J.; Donohue, Tom; Fahy, Eoin; Hunt, Colin; Leech, Sinead; Lucey, Con; McCoy, Danny; O'Rourke, Feargal; O'Sullivan, Mary; Redmond, Mark; Soffe, Willie; Walsh, Mary; Taxation, Ireland Commission on (September 2009). "Commission on Taxation report 2009". UCD Archives. Archived from the original on 13 June 2018. Retrieved 22 August 2018.

↑ Rochelle Toplensky (7 March 2018). "Europe points finger at Ireland over tax avoidance". Irish Times. Archived from the original on 7 March 2018. Retrieved 7 April 2018. Multinational companies have made such extensive use of Ireland to funnel royalties — a common way to shift profits and avoid tax — that these payments averaged 23 per cent of the country's annual gross domestic product between 2010 and 2015, according to a European Commission report seen by the Financial Times. The scale of the net royalty payments channelled through Ireland contrasts sharply with the average in the EU as a whole, where such payments are a fraction of one per cent of the bloc's annual GDP.

↑ "Leprechaun Economics". Paul Krugman (Twitter). 12 July 2016. Archived from the original on 16 June 2018. Retrieved 7 April 2018.

↑ "CSO Press Release"(PDF). Central Statistics Office (Ireland). 12 July 2016. Archived(PDF) from the original on 22 November 2017. Retrieved 28 April 2018.

↑ Max de Haldevang (11 June 2018). "How tax havens turn economic statistics into nonsense". Quartz (publication). Archived from the original on 12 June 2018. Retrieved 12 June 2018. A recent IMF article reveals a perfect example: "A stunning $12 trillion—almost 40% of all foreign direct investment positions globally—is completely artificial," write economists Jannick Damgaard, Thomas Elkjaer, and Niels Johannesen

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.