Related Research Articles

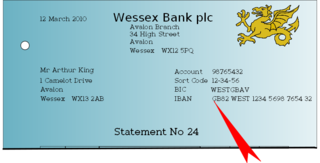

The International Bank Account Number (IBAN) is an internationally agreed system of identifying bank accounts across national borders to facilitate the communication and processing of cross border transactions with a reduced risk of transcription errors. An IBAN uniquely identifies the account of a customer at a financial institution. It was originally adopted by the European Committee for Banking Standards (ECBS) and since 1997 as the international standard ISO 13616 under the International Organization for Standardization (ISO). The current version is ISO 13616:2020, which indicates the Society for Worldwide Interbank Financial Telecommunication (SWIFT) as the formal registrar. Initially developed to facilitate payments within the European Union, it has been implemented by most European countries and numerous countries in other parts of the world, mainly in the Middle East and the Caribbean. As of May 2020, 77 countries were using the IBAN numbering system.

The Society for Worldwide Interbank Financial Telecommunication (Swift), legally S.W.I.F.T. SC, is a Belgian cooperative society providing services related to the execution of financial transactions and payments between certain banks worldwide. Its principal function is to serve as the main messaging network through which international payments are initiated. It also sells software and services to financial institutions, mostly for use on its proprietary "SWIFTNet", and assigns ISO 9362 Business Identifier Codes (BICs), popularly known as "Swift codes".

ISO 9362 is an international standard for Business Identifier Codes (BIC), a unique identifier for business institutions, approved by the International Organization for Standardization (ISO). BIC is also known as SWIFT-BIC, SWIFT ID, or SWIFT code, after the Society for Worldwide Interbank Financial Telecommunication (SWIFT), which is designated by ISO as the BIC registration authority. BIC was defined originally as Bank Identifier Code and is most often assigned to financial organizations; when it is assigned to non-financial organization, the code may also be known as Business Entity Identifier (BEI). These codes are used when transferring money between banks, particularly for international wire transfers, and also for the exchange of other messages between banks. The codes can sometimes be found on account statements.

In the United States, an ABA routing transit number is a nine-digit code printed on the bottom of checks to identify the financial institution on which it was drawn. The American Bankers Association (ABA) developed the system in 1910 to facilitate the sorting, bundling, and delivering of paper checks to the drawer's bank for debit to the drawer's account.

Delivery versus payment or DvP is a common form of settlement for securities. The process involves the simultaneous delivery of all documents necessary to give effect to a transfer of securities in exchange for the receipt of the stipulated payment amount. Alternatively, it may involve transfers of two securities in such a way as to ensure that delivery of one security occurs if and only if the corresponding delivery of the other security occurs.

Wire transfer, bank transfer, or credit transfer, is a method of electronic funds transfer from one person or entity to another. A wire transfer can be made from one bank account to another bank account, or through a transfer of cash at a cash office.

ISO 15022 is an ISO standard for securities messaging used in transactions between financial institutions. Participants in the financial industry need a common representation of the financial transactions they perform and this standard defines general message schema, which in turn are used by organizations to define messages in a complete and unambiguous way. This results in efficiency, lower costs, and the avoidance of errors. Prior to standardization in this area, there were overlapping standards, or ad hoc approaches where there was a functional gap and no standard.

The Australian financial system consists of the arrangements covering the borrowing and lending of funds and the transfer of ownership of financial claims in Australia, comprising:

A cheque, or check, is a document that orders a bank to pay a specific amount of money from a person's account to the person in whose name the cheque has been issued. The person writing the cheque, known as the drawer, has a transaction banking account where the money is held. The drawer writes various details including the monetary amount, date, and a payee on the cheque, and signs it, ordering their bank, known as the drawee, to pay the amount of money stated to the payee.

ISO 20022 is an ISO standard for electronic data interchange between financial institutions. It describes a metadata repository containing descriptions of messages and business processes, and a maintenance process for the repository content. The standard covers financial information transferred between financial institutions that includes payment transactions, securities trading and settlement information, credit and debit card transactions and other financial information.

In banking and finance, clearing denotes all activities from the time a commitment is made for a transaction until it is settled. This process turns the promise of payment into the actual movement of money from one account to another. Clearing houses were formed to facilitate such transactions among banks.

A Bank State Branch is the name used in Australia for a bank code, which is a branch identifier. The BSB is normally used in association with the account number system used by each financial institution. The structure of the BSB + account number does not permit for account numbers to be transferable between financial institutions. While similar in structure, the New Zealand and Australian systems are only used in domestic transactions and are incompatible with each other. For international transfers, a SWIFT code is used in addition to the BSB and account number.

ISO 8583 is an international standard for financial transaction card originated interchange messaging. It is the International Organization for Standardization standard for systems that exchange electronic transactions initiated by cardholders using payment cards.

Sort codes are the domestic bank codes used to route money transfers between financial institutions in the United Kingdom, and in the Republic of Ireland. They are six-digit hierarchical numerical addresses that specify clearing banks, clearing systems, regions, large financial institutions, groups of financial institutions and ultimately resolve to individual branches. In the UK they continue to be used to route transactions domestically within clearance organisations and to identify accounts, while in the Republic of Ireland they have been deprecated and replaced by the SEPA systems and infrastructure.

Payment cards are part of a payment system issued by financial institutions, such as a bank, to a customer that enables its owner to access the funds in the customer's designated bank accounts, or through a credit account and make payments by electronic transfer with a payment terminal and access automated teller machines (ATMs). Such cards are known by a variety of names including bank cards, ATM cards, client cards, key cards or cash cards.

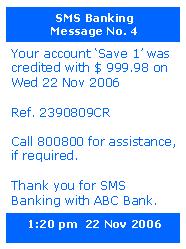

SMS banking' is a form of mobile banking. It is a facility used by some banks or other financial institutions to send messages to customers' mobile phones using SMS messaging, or a service provided by them which enables customers to perform some financial transactions using SMS.

MT103 is a specific SWIFT message types/format used on the Society for Worldwide Interbank Financial Telecommunication (SWIFT) payment system to send for cross border/international wire transfer messages between financial institutions for customer cash transfers.

Mobile payments is a mode of payment using mobile phones. Instead of using methods like cash, cheque, and credit card, a customer can use a mobile phone to transfer money or to pay for goods and services. A customer can transfer money or pay for goods and services by sending an SMS, using a Java application over GPRS, a WAP service, over IVR or other mobile communication technologies. In India, this service is bank-led. Customers wishing to avail themselves of this service will have to register with banks which provide this service. Currently, this service is being offered by several major banks and is expected to grow further. Mobile Payment Forum of India (MPFI) is the umbrella organisation which is responsible for deploying mobile payments in India.

The Cross-Border Interbank Payment System (CIPS) is a Chinese payment system that offers clearing and settlement services for its participants in cross-border renminbi (RMB) payments and trade. Backed by the People's Bank of China (PBOC), China launched the CIPS in 2015 to internationalize RMB use. CIPS also counts several foreign banks as shareholders, including HSBC, Standard Chartered, the Bank of East Asia, DBS Bank, Citi, Australia and New Zealand Banking Group, and BNP Paribas.

MT202 COV is a specific SWIFT message type used on the SWIFT network for financial institution (FI) funds transfer between financial institutions.

References

- ↑ McGill, R.; Patel, N. (2008). Global Custody and Clearing Services. Basingstoke, Hampshire: Springer. p. 27. ISBN 9781349282883.

- ↑ swift.com

- ↑ "List of all SWIFT Messages Types". Paiementor. Retrieved 2020-01-07.

- ↑ "List of all SWIFT Messages Types". Paiementor. Retrieved 2020-01-07.