The United States of America has separate federal, state, and local governments with taxes imposed at each of these levels. Taxes are levied on income, payroll, property, sales, capital gains, dividends, imports, estates and gifts, as well as various fees. In 2020, taxes collected by federal, state, and local governments amounted to 25.5% of GDP, below the OECD average of 33.5% of GDP. The United States had the seventh-lowest tax revenue-to-GDP ratio among OECD countries in 2020, with a higher ratio than Mexico, Colombia, Chile, Ireland, Costa Rica, and Turkey.

A limited liability company is the United States-specific form of a private limited company. It is a business structure that can combine the pass-through taxation of a partnership or sole proprietorship with the limited liability of a corporation. An LLC is not a corporation under state law; it is a legal form of a company that provides limited liability to its owners in many jurisdictions. LLCs are well known for the flexibility that they provide to business owners; depending on the situation, an LLC may elect to use corporate tax rules instead of being treated as a partnership, and, under certain circumstances, LLCs may be organized as not-for-profit. In certain U.S. states, businesses that provide professional services requiring a state professional license, such as legal or medical services, may not be allowed to form an LLC but may be required to form a similar entity called a professional limited liability company (PLLC).

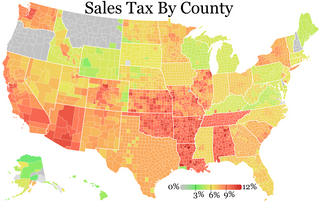

A sales tax is a tax paid to a governing body for the sales of certain goods and services. Usually laws allow the seller to collect funds for the tax from the consumer at the point of purchase.

A budget is a calculation plan, usually but not always financial, for a defined period, often one year or a month. A budget may include anticipated sales volumes and revenues, resource quantities including time, costs and expenses, environmental impacts such as greenhouse gas emissions, other impacts, assets, liabilities and cash flows. Companies, governments, families, and other organizations use budgets to express strategic plans of activities in measurable terms.

Fiona Ma is an American accountant and politician. She has been serving as the California state treasurer since January 7, 2019. She previously served as a member of the California Board of Equalization from 2015 to 2019, the California State Assembly (2006–2012), and the San Francisco Board of Supervisors (2002–2006).

A use tax is a type of tax levied in the United States by numerous state governments. It is essentially the same as a sales tax but is applied not where a product or service was sold but where a merchant bought a product or service and then converted it for its own use, without having paid tax when it was initially purchased. Use taxes are functionally equivalent to sales taxes. They are typically levied upon the use, storage, enjoyment, or other consumption in the state of tangible personal property that has not been subjected to a sales tax.

Mary Fallin is an American politician who served as the 27th governor of Oklahoma from 2011 to 2019. A member of the Republican Party, she was elected in 2010 and reelected in 2014. She is the first and so far only woman to be elected governor of Oklahoma. She was the first woman to represent Oklahoma in Congress since Alice Mary Robertson in 1920.

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. 45 states, the District of Columbia, the territories of Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

The Streamlined Sales Tax Project (SSTP), first organized in March 2000, is intended to simplify and modernize sales and use tax collection and administration in the United States. It arose in response to efforts by Congress to permanently prohibit states from collecting sales tax on online commerce. Because such a ban would have serious financial consequences for states, the SSTP began as an effort to try to minimize the many differences between the states' sales tax policies and practices. The SSTP was dissolved once the Streamlined Sales and Use Tax Agreement (SSUTA) became effective on October 1, 2005.

Tax-free shopping (TFS) is the buying of goods in another country or state and obtaining a refund of the sales tax which has been collected by the retailer on those goods. The sales tax may be variously described as a sales tax, goods and services tax (GST), value added tax (VAT), or consumption tax.

Internet tax is a tax on Internet-based services. A number of jurisdictions have introduced an Internet tax and others are considering doing so mainly as a result of successful tax avoidance by multinational corporations that operate within the digital economy. Internet taxes prominently target companies including Facebook, Google, Amazon, Airbnb, Uber.

A hotel tax or lodging tax is charged in most of the United States, to travelers when they rent accommodations in a hotel, inn, tourist home or house, motel, or other lodging, generally unless the stay is for a period of 30 days or more. In addition to sales tax, it is collected when payment is made for the accommodation, and it is then remitted by the lodging operator to the city or county. It can also be called hotel occupancy tax, in places like New York city and Texas. Despite its name, it generally applies to the same range of accommodations.

Proposition 218 is an adopted initiative constitutional amendment which revolutionized local and regional government finance and taxation in California. Named the "Right to Vote on Taxes Act," it was sponsored by the Howard Jarvis Taxpayers Association as a constitutional follow-up to the landmark property tax reduction initiative constitutional amendment, Proposition 13, approved in 1978. Proposition 218 was approved and adopted by California voters during the November 5, 1996, statewide general election.

Archon Information Systems, L.L.C. (“Archon”) is a Delaware corporation that provides technology and collection services to government clients.

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property times an assessment ratio times a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other taxes. The property tax typically produces the required revenue for municipalities' tax levies. A disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

Taxes in California are among the highest in the United States and are imposed by the state and by local governments.

Amazon's tax behaviours have been investigated in China, Germany, Poland, Sweden, South Korea, France, Japan, Ireland, Singapore, Luxembourg, Italy, Spain, United Kingdom, multiple states in the United States, and Portugal. According to a report released by Fair Tax Mark in 2019, Amazon is the best actor of tax avoidance, having paid a 12% effective tax rate between 2010-2018, in contrast with 35% corporate tax rate in the US during the same period. Amazon countered that it had an 24% effective tax rate during the same period.

California has an extensive system of local government that manages public functions throughout the state. Like most states, California is divided into counties, of which there are 58 covering the entire state. Most urbanized areas are incorporated as cities, though not all of California is within the boundaries of a city. School districts, which are independent of cities and counties, handle public education. Many other functions, especially in unincorporated areas, are handled by special districts, which include municipal utility districts, transit districts, health care districts, vector control districts, and geologic hazard abatement districts.

Apple’s EU tax dispute refers to an investigation by the European Commission into tax arrangements between Apple and Ireland, which allowed the company to pay close to zero corporate tax over 10 years.

California Proposition 19 (2020), also referred to as Assembly Constitutional Amendment No. 11, is an amendment of the Constitution of California that was narrowly approved by voters in the general election on November 3, 2020, with just over 51% of the vote. The legislation increases the property tax burden on owners of inherited property to provide expanded property tax benefits to homeowners ages 55 years and older, disabled homeowners, and victims of natural disasters and fund wildfire response. According to the California Legislative Analyst, Proposition 19 is a large net tax increase "of hundreds of millions of dollars per year."