North Rhine-Westphalia or North-Rhine/Westphalia, commonly shortened to NRW, is a state (Land) in Western Germany. With more than 18 million inhabitants, it is the most populous state in Germany. Apart from the city-states, it is also the most densely populated state in Germany. Covering an area of 34,084 km2 (13,160 sq mi), it is the fourth-largest German state by size.

Debt is an obligation that requires one party, the debtor, to pay money borrowed or otherwise withheld from another party, the creditor. Debt may be owed by sovereign state or country, local government, company, or an individual. Commercial debt is generally subject to contractual terms regarding the amount and timing of repayments of principal and interest. Loans, bonds, notes, and mortgages are all types of debt. In financial accounting, debt is a type of financial transaction, as distinct from equity.

In finance, a loan is the transfer of money by one party to another with an agreement to pay it back. The recipient, or borrower, incurs a debt and is usually required to pay interest for the use of the money.

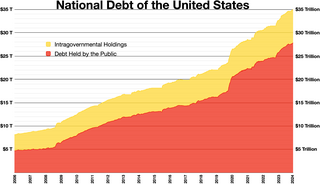

The national debt of the United States is the total national debt owed by the federal government of the United States to Treasury security holders. The national debt at any point in time is the face value of the then-outstanding Treasury securities that have been issued by the Treasury and other federal agencies. The terms "national deficit" and "national surplus" usually refer to the federal government budget balance from year to year, not the cumulative amount of debt. In a deficit year the national debt increases as the government needs to borrow funds to finance the deficit, while in a surplus year the debt decreases as more money is received than spent, enabling the government to reduce the debt by buying back some Treasury securities. In general, government debt increases as a result of government spending and decreases from tax or other receipts, both of which fluctuate during the course of a fiscal year. There are two components of gross national debt:

A taxpayer is a person or organization subject to pay a tax. Modern taxpayers may have an identification number, a reference number issued by a government to citizens or firms.

A capital gains tax (CGT) is the tax on profits realized on the sale of a non-inventory asset. The most common capital gains are realized from the sale of stocks, bonds, precious metals, real estate, and property.

A country's gross government debt is the financial liabilities of the government sector. Changes in government debt over time reflect primarily borrowing due to past government deficits. A deficit occurs when a government's expenditures exceed revenues. Government debt may be owed to domestic residents, as well as to foreign residents. If owed to foreign residents, that quantity is included in the country's external debt.

Georg Milbradt is a German politician of the Christian Democratic Union (CDU) who served as Minister-President of Saxony from 2002 to 2008.

Global debt refers to the total amount of money owed by all sectors, including governments, businesses, and households worldwide.

Taxpayers in the United States may have tax consequences when debt is cancelled. This is commonly known as cancellation-of-debt (COD) income. According to the Internal Revenue Code, the discharge of indebtedness must be included in a taxpayer's gross income. There are exceptions to this rule, however, so a careful examination of one's COD income is important to determine any potential tax consequences.

In United States income tax law, an installment sale is generally a "disposition of property where at least 1 loan payment is to be received after the close of the taxable year in which the disposition occurs." The term "installment sale" does not include, however, a "dealer disposition" or, generally, a sale of inventory. The installment method of accounting provides an exception to the general principles of income recognition by allowing a taxpayer to defer the inclusion of income of amounts that are to be received from the disposition of certain types of property until payment in cash or cash equivalents is received. The installment method defers the recognition of income when compared with both the cash and accrual methods of accounting. Under the cash method, the taxpayer would recognize the income when it is received, including the entire sum paid in the form of a negotiable note. The deferral advantages of the installment method are the most pronounced when comparing to the accrual method, under which a taxpayer must recognize income as soon as he or she has a right to the income.

The Mortgage Forgiveness Debt Relief Act of 2007 was introduced in the United States Congress on September 25, 2007, and signed into law by President George W. Bush on December 20, 2007. This act offers relief to homeowners who would have owed taxes on forgiven mortgage debt after facing foreclosure. The act extends such relief for three years, applying to debts discharged in calendar years 2007 through 2009. With the Emergency Economic Stabilization Act of 2008, this tax relief was extended another three years, covering debts discharged through calendar year 2012. The relief was further extended until January 1, 2014, at Section 202 of the American Taxpayer Relief Act of 2012.

Christian Wolfgang Lindner is a German politician of the Free Democratic Party (FDP) who has been serving as the Federal Minister of Finance since 8 December 2021. He has been the party leader of the FDP since 2013 and a Member of the Bundestag (MdB) for North Rhine-Westphalia since 2017, previously holding a seat from 2009 until 2012.

The National Debt Clock is a billboard-sized running total display that shows the United States gross national debt and each American family's share of the debt. As of 2017, it is installed on the western side of the Bank of America Tower, west of Sixth Avenue between 42nd and 43rd Streets in Manhattan, New York City. It was the first debt clock installed anywhere.

The financial position of the United States includes assets of at least $269 trillion and debts of $145.8 trillion to produce a net worth of at least $123.8 trillion. GDP in Q1 decline was due to foreclosures and increased rates of household saving. There were significant declines in debt to GDP in each sector except the government, which ran large deficits to offset deleveraging or debt reduction in other sectors.

The National Asset Management Agency is a body created by the government of Ireland in late 2009 in response to the Irish financial crisis and the deflation of the Irish property bubble.

Canadian public debt, or general government debt, is the liabilities of the government sector. Government gross debt consists of liabilities that are a financial claim that requires payment of interest and/or principal in future. They consist mainly of Treasury bonds, but also include public service employee pension liabilities. Changes in debt arise primarily from new borrowing, due to government expenditures exceeding revenues.

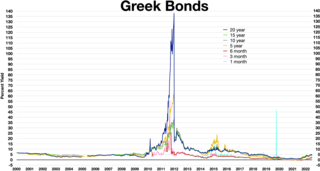

The European debt crisis, often also referred to as the eurozone crisis or the European sovereign debt crisis, was a multi-year debt crisis that took place in the European Union (EU) from 2009 until the mid to late 2010s. Several eurozone member states were unable to repay or refinance their government debt or to bail out over-indebted banks under their national supervision without the assistance of third parties like other eurozone countries, the European Central Bank (ECB), or the International Monetary Fund (IMF).

Greece faced a sovereign debt crisis in the aftermath of the 2007–2008 financial crisis. Widely known in the country as The Crisis, it reached the populace as a series of sudden reforms and austerity measures that led to impoverishment and loss of income and property, as well as a humanitarian crisis. In all, the Greek economy suffered the longest recession of any advanced mixed economy to date and became the first developed country whose stock market was downgraded to that of an emerging market in 2013. As a result, the Greek political system was upended, social exclusion increased, and hundreds of thousands of well-educated Greeks left the country.

The proposed long-term solutions for the Eurozone crisis address ways to deal with the European debt crisis that took place in the European Union from 2009 till the late 2010s, including risks to Eurozone country governments and the Euro.