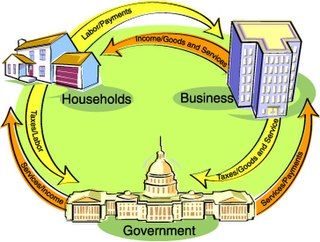

Macroeconomics is a branch of economics dealing with the performance, structure, behavior, and decision-making of an economy as a whole. For example, using interest rates, taxes and government spending to regulate an economy’s growth and stability. This includes regional, national, and global economies.

The IS–LM model, or Hicks–Hansen model, is a two-dimensional macroeconomic tool that shows the relationship between interest rates and assets market. The intersection of the "investment–saving" (IS) and "liquidity preference–money supply" (LM) curves models "general equilibrium" where supposed simultaneous equilibria occur in both the goods and the asset markets. Yet two equivalent interpretations are possible: first, the IS–LM model explains changes in national income when the price level is fixed in the short-run; second, the IS–LM model shows why an aggregate demand curve can shift. Hence, this tool is sometimes used not only to analyse economic fluctuations but also to suggest potential levels for appropriate stabilisation policies.

In economics, "rational expectations" are model-consistent expectations, in that agents inside the model are assumed to "know the model" and on average take the model's predictions as valid. Rational expectations ensure internal consistency in models involving uncertainty. To obtain consistency within a model, the predictions of future values of economically relevant variables from the model are assumed to be the same as that of the decision-makers in the model, given their information set, the nature of the random processes involved, and model structure. The rational expectations assumption is used especially in many contemporary macroeconomic models.

New Keynesian economics is a school of macroeconomics that strives to provide microeconomic foundations for Keynesian economics. It developed partly as a response to criticisms of Keynesian macroeconomics by adherents of new classical macroeconomics.

Robert Emerson Lucas Jr. is an American economist at the University of Chicago, where he is currently the John Dewey Distinguished Service Professor Emeritus in Economics and the College. Widely regarded as the central figure in the development of the new classical approach to macroeconomics, he received the Nobel Prize in Economics in 1995 "for having developed and applied the hypothesis of rational expectations, and thereby having transformed macroeconomic analysis and deepened our understanding of economic policy". He has been characterized by N. Gregory Mankiw as "the most influential macroeconomist of the last quarter of the 20th century." As of 2020, he ranks as the 11th most cited economist in the world.

The Phillips curve is a single-equation economic model, named after William Phillips, describing an inverse relationship between rates of unemployment and corresponding rates of rises in wages that result within an economy. Stated simply, decreased unemployment, in an economy will correlate with higher rates of wage rises. Phillips did not himself state there was any relationship between employment and inflation; this notion was a trivial deduction from his statistical findings. Paul Samuelson and Robert Solow made the connection explicit and subsequently Milton Friedman and Edmund Phelps put the theoretical structure in place. In so doing, Friedman was to successfully predict the imminent collapse of Phillips' a-theoretic correlation.

In macroeconomics, aggregate demand (AD) or domestic final demand (DFD) is the total demand for final goods and services in an economy at a given time. It is often called effective demand, though at other times this term is distinguished. This is the demand for the gross domestic product of a country. It specifies the amount of goods and services that will be purchased at all possible price levels. Consumer spending, investment, corporate and government expenditure, and net exports make up the aggregate demand.

A macroeconomic model is an analytical tool designed to describe the operation of the problems of economy of a country or a region. These models are usually designed to examine the comparative statics and dynamics of aggregate quantities such as the total amount of goods and services produced, total income earned, the level of employment of productive resources, and the level of prices.

Neutrality of money is the idea that a change in the stock of money affects only nominal variables in the economy such as prices, wages, and exchange rates, with no effect on real variables, like employment, real GDP, and real consumption. Neutrality of money is an important idea in classical economics and is related to the classical dichotomy. It implies that the central bank does not affect the real economy by creating money. Instead, any increase in the supply of money would be offset by a proportional rise in prices and wages. This assumption underlies some mainstream macroeconomic models. Others like monetarism view money as being neutral only in the long-run.

The policy-ineffectiveness proposition (PIP) is a new classical theory proposed in 1975 by Thomas J. Sargent and Neil Wallace based upon the theory of rational expectations, which posits that monetary policy cannot systematically manage the levels of output and employment in the economy.

In macroeconomics, the classical dichotomy is the idea, attributed to classical and pre-Keynesian economics, that real and nominal variables can be analyzed separately. To be precise, an economy exhibits the classical dichotomy if real variables such as output and real interest rates can be completely analyzed without considering what is happening to their nominal counterparts, the money value of output and the interest rate. In particular, this means that real GDP and other real variables can be determined without knowing the level of the nominal money supply or the rate of inflation. An economy exhibits the classical dichotomy if money is neutral, affecting only the price level, not real variables. As such, if the classical dichotomy holds, money only affects absolute rather than the relative prices between goods.

The Lucas islands model is an economic model of the link between money supply and price and output changes in a simplified economy using rational expectations. It delivered a new classical explanation of the Phillips curve relationship between unemployment and inflation. The model was formulated by Robert Lucas, Jr. in a series of papers in the 1970s.

In monetary economics, the demand for money is the desired holding of financial assets in the form of money: that is, cash or bank deposits rather than investments. It can refer to the demand for money narrowly defined as M1, or for money in the broader sense of M2 or M3.

Dynamic stochastic general equilibrium modeling is a macroeconomic method which is often employed by monetary and fiscal authorities for policy analysis, explaining historical time-series data, as well as future forecasting purposes. DSGE econometric modeling applies general equilibrium theory and microeconomic principles in a tractable manner to postulate economic phenomena, such as economic growth and business cycles, as well as policy effects and market shocks.

New classical macroeconomics, sometimes simply called new classical economics, is a school of thought in macroeconomics that builds its analysis entirely on a neoclassical framework. Specifically, it emphasizes the importance of rigorous foundations based on microeconomics, especially rational expectations.

The AD–AS or aggregate demand–aggregate supply model is a macroeconomic model that explains price level and output through the relationship of aggregate demand and aggregate supply.

The Keynesian cross diagram is a formulation of the central ideas in Keynes' General Theory. It first appeared as a central component of macroeconomic theory as it was taught by Paul Samuelson in his textbook, Economics: An Introductory Analysis. The Keynesian Cross plots aggregate income and planned total spending or aggregate expenditure.

Macroeconomic theory has its origins in the study of business cycles and monetary theory. In general, early theorists believed monetary factors could not affect real factors such as real output. John Maynard Keynes attacked some of these "classical" theories and produced a general theory that described the whole economy in terms of aggregates rather than individual, microeconomic parts. Attempting to explain unemployment and recessions, he noticed the tendency for people and businesses to hoard cash and avoid investment during a recession. He argued that this invalidated the assumptions of classical economists who thought that markets always clear, leaving no surplus of goods and no willing labor left idle.

The new neoclassical synthesis (NNS) or new synthesis is the fusion of the major, modern macroeconomic schools of thought, new classical and New-Keynesianism, into a consensus on the best way to explain short-run fluctuations in the economy. This new synthesis is analogous to the neoclassical synthesis that combined neoclassical economics with Keynesian macroeconomics. The new synthesis provides the theoretical foundation for much of contemporary mainstream economics. It is an important part of the theoretical foundation for the work done by the Federal Reserve and many other central banks.

The Taylor contract or staggered contract was first formulated by John B. Taylor in his two articles, in 1979 "Staggered wage setting in a macro model'. and in 1980 "Aggregate Dynamics and Staggered Contracts". In its simplest form, one can think of two equal sized unions who set wages in an industry. Each period, one of the unions sets the nominal wage for two periods. This means that in any one period, only one of the unions can reset its wage and react to events that have just happened. When the union sets its wage, it sets it for a known and fixed period of time. Whilst it will know what is happening in the first period when it sets the new wage, it will have to form expectations about the factors in the second period that determine the optimal wage to set. Although the model was first used to model wage setting, in new Keynesian models that followed it was also used to model price-setting by firms.