Double taxation is the levying of tax by two or more jurisdictions on the same income, asset, or financial transaction.

Although the actual definitions vary between jurisdictions, in general, a direct tax or income tax is a tax imposed upon a person or property as distinct from a tax imposed upon a transaction, which is described as an indirect tax. There is a distinction between direct and indirect tax depending on whether the tax payer is the actual taxpayer or if the amount of tax is supported by a third party, usually a client. The term may be used in economic and political analyses, but does not itself have any legal implications. However, in the United States, the term has special constitutional significance because of a provision in the U.S. Constitution that any direct taxes imposed by the national government be apportioned among the states on the basis of population. In the European Union direct taxation remains the sole responsibility of member states.

Tax withholding, also known as tax retention, pay-as-you-earn tax or tax deduction at source, is income tax paid to the government by the payer of the income rather than by the recipient of the income. The tax is thus withheld or deducted from the income due to the recipient. In most jurisdictions, tax withholding applies to employment income. Many jurisdictions also require withholding taxes on payments of interest or dividends. In most jurisdictions, there are additional tax withholding obligations if the recipient of the income is resident in a different jurisdiction, and in those circumstances withholding tax sometimes applies to royalties, rent or even the sale of real estate. Governments use tax withholding as a means to combat tax evasion, and sometimes impose additional tax withholding requirements if the recipient has been delinquent in filing tax returns, or in industries where tax evasion is perceived to be common.

The Working Time Directive2003/88/EC is a European Union law Directive and a key part of European labour law. It gives EU workers the right to:

The European Union withholding tax is the common name for a withholding tax which is deducted from interest earned by European Union residents on their investments made in another member state, by the state in which the investment is held. The European Union itself has no taxation powers, so the name is strictly a misnomer. The aim of the tax is to ensure that citizens of one member state do not evade taxation by depositing funds outside the jurisdiction of residence and so distort the single market. The tax is withheld at source and passed on to the EU Country of residence. All but three member states disclose the recipient of the interest concerned. Most EU states already apply a withholding tax to savings and investment income earned by their nationals on deposits and investments in their own states. The Directive seeks to bring inter-state income into the same arrangement, under the Single Market policy.

Taxation in Greece is based on the direct and indirect systems. The total tax revenue in 2017 was €47.56 billion from which €20.62 billion came from direct taxes and €26.94 billion from indirect taxes. The total tax revenue represented 39.4% of GDP in 2017. Taxes in Greece are collected by the Independent Authority for Public Revenue.

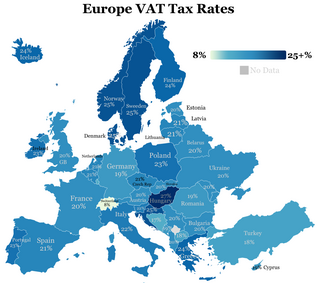

The European Union value-added tax is a value added tax on goods and services within the European Union (EU). The EU's institutions do not collect the tax, but EU member states are each required to adopt in national legislation a value added tax that complies with the EU VAT code. Different rates of VAT apply in different EU member states, ranging from 17% in Luxembourg to 27% in Hungary. The total VAT collected by member states is used as part of the calculation to determine what each state contributes to the EU's budget.

The Revised Payment Services Directive (PSD2, Directive (EU) 2015/2366, which replaced the Payment Services Directive (PSD), Directive 2007/64/EC) is an EU Directive, administered by the European Commission (Directorate General Internal Market) to regulate payment services and payment service providers throughout the European Union (EU) and European Economic Area (EEA). The PSD's purpose was to increase pan-European competition and participation in the payments industry also from non-banks, and to provide for a level playing field by harmonizing consumer protection and the rights and obligations of payment providers and users. The key objectives of the PSD2 directive are creating a more integrated European payments market, making payments more secure and protecting consumers.

Netherlands benefits from a strategic geographic location, a world-class economy, a stable political climate, and a skilled workforce. The Netherlands has a large network of tax treaties, a low corporate income tax rate and a full participation exemption for capital gains and profits. These characteristics, in addition to a favorable tax environment, make Netherlands one of the most open economies in the world for multinational corporations (MNCs).

The tax system of Andorra has evolved according to the country's economic activity and structure, and the tax bases have been expanded to optimally distribute the weight of the tax burden, going from an almost exclusively indirect tax system to a system with direct taxation that can be approved at the international level. Despite its taxes, Andorra ceased to be a tax haven for its neighboring countries years ago, and for the European Union and OECD recently.

European organisational law is a part of European Union law, which concerns the formation, operation and insolvency of public bodies, partnerships, corporations and foundations in the entire European Union. There is no substantive European company law as such, although a host of minimum standards are applicable to companies throughout the European Union. All member states continue to operate separate companies acts, which are amended from time to time to comply with EU Directives and Regulations. There is, however, also the option of businesses to incorporate as a Societas Europaea (SE), which allows a company to operate across all member states.

Taxation in Estonia consists of state and local taxes. A relatively high proportion of government revenue comes from consumption taxes whilst revenue from capital taxes is one of the lowest in the European Union.

In Slovakia, taxes are levied by the state and local governments. Tax revenue stood at 19.3% of the country's gross domestic product in 2021. The tax-to-GDP ratio in Slovakia deviates from OECD average of 34.0% by 0.8 percent and in 2022 was 34.8% which ranks Slovakia 19th in the tax-to-GDP ratio comparison among the OECD countries. The most important revenue sources for the state government are income tax, social security, value-added tax and corporate tax.

European company law is the part of European Union law which concerns the formation, operation and insolvency of companies in the European Union. The EU creates minimum standards for companies throughout the EU, and has its own corporate forms. All member states continue to operate separate companies acts, which are amended from time to time to comply with EU Directives and Regulations. There is, however, also the option of businesses to incorporate as a Societas Europaea (SE), which allows a company to operate across all member states.

The Tax Attractiveness Index (T.A.X.) indicates the attractiveness of a country's tax environment and the possibilities of tax planning for companies. The T.A.X. is constructed for 100 countries worldwide starting from 2005 on. The index covers 20 equally weighted components of real-world tax systems which are relevant for corporate location decisions. The index ranges between zero and one. The more the index values approaches one, the more attractive is the tax environment of a certain country from a corporate perspective. The 100 countries include 41 European countries, 19 American countries, 6 Caribbean countries, 18 countries that are located in Africa & Middle East, and 16 countries that fall into the Asia-Pacific region.

The Energy Efficiency Directive 2012/27/EU is a European Union directive which mandates energy efficiency improvements within the European Union. It was approved on 25 October 2012 and entered into force on 4 December 2012. The directive introduces legally binding measures to encourage efforts to use energy more efficiently in all stages and sectors of the supply chain. It establishes a common framework for the promotion of energy efficiency within the EU in order to meet its energy efficiency headline target of 20% by 2020. It also paves the way for further improvements thereafter.

The European Union tax haven blacklist, officially the EU list of non-cooperative tax jurisdictions, is a tool of the European Union (EU) that lists tax havens. It is used by the Member States to tackle external risks of tax abuse and unfair tax competition. It was adopted for the first time in 2017 as a response to tax avoidance in the EU, screening 92 countries. It is managed by the Code of Conduct Group for Business Taxation and monitored by the European Commission (EC). The most recent revision was released on 6 October 2020. The list is updated twice a year.

The Energy Taxation Directive or ETD (2003/96/EC) is a European directive, which establishes the framework conditions of the European Union for the taxation of electricity, motor and aviation fuels and most heating fuels. The directive is part of European Union energy law; its core component is the setting of minimum tax rates for all Member States.

The Central Electronic System of Payments (CESOP) regime is an automatic exchange of information regime being introduced in the European Union from 1 January 2024. The rules were introduced by Council Directive 2020/284, amending the EU's Value-added tax Directive.