In economics, a recession is a business cycle contraction that occurs when there is a general decline in economic activity. Recessions generally occur when there is a widespread drop in spending. This may be triggered by various events, such as a financial crisis, an external trade shock, an adverse supply shock, the bursting of an economic bubble, or a large-scale anthropogenic or natural disaster.

In economics, inflation is a general increase in the prices of goods and services in an economy. This is usually measured using the consumer price index (CPI). When the general price level rises, each unit of currency buys fewer goods and services; consequently, inflation corresponds to a reduction in the purchasing power of money. The opposite of CPI inflation is deflation, a decrease in the general price level of goods and services. The common measure of inflation is the inflation rate, the annualized percentage change in a general price index. As prices faced by households do not all increase at the same rate, the consumer price index (CPI) is often used for this purpose.

A stock market, equity market, or share market is the aggregation of buyers and sellers of stocks, which represent ownership claims on businesses; these may include securities listed on a public stock exchange as well as stock that is only traded privately, such as shares of private companies that are sold to investors through equity crowdfunding platforms. Investments are usually made with an investment strategy in mind.

An economic indicator is a statistic about an economic activity. Economic indicators allow analysis of economic performance and predictions of future performance. One application of economic indicators is the study of business cycles. Economic indicators include various indices, earnings reports, and economic summaries: for example, the unemployment rate, quits rate, housing starts, consumer price index, Inverted yield curve, consumer leverage ratio, industrial production, bankruptcies, gross domestic product, broadband internet penetration, retail sales, price index, and changes in credit conditions.

Business cycles are intervals of general expansion followed by recession in economic performance. The changes in economic activity that characterize business cycles have important implications for the welfare of the general population, government institutions, and private sector firms. There are numerous specific definitions of what constitutes a business cycle. The simplest and most naïve characterization comes from regarding recessions as 2 consecutive quarters of negative GDP growth. More satisfactory classifications are provided by, first including more economic indicators and second by looking for more informative data patterns than the ad hoc 2 quarter definition.

The causes of the Great Depression in the early 20th century in the United States have been extensively discussed by economists and remain a matter of active debate. They are part of the larger debate about economic crises and recessions. The specific economic events that took place during the Great Depression are well established.

In the United States, the federal funds rate is the interest rate at which depository institutions lend reserve balances to other depository institutions overnight on an uncollateralized basis. Reserve balances are amounts held at the Federal Reserve. Institutions with surplus balances in their accounts lend those balances to institutions in need of larger balances. The federal funds rate is an important benchmark in financial markets and central to the conduct of monetary policy in the United States as it influences a wide range of market interest rates.

The Austrian business cycle theory (ABCT) is an economic theory developed by the Austrian School of economics about how business cycles occur. The theory views business cycles as the consequence of excessive growth in bank credit due to artificially low interest rates set by a central bank or fractional reserve banks. The Austrian business cycle theory originated in the work of Austrian School economists Ludwig von Mises and Friedrich Hayek. Hayek won the Nobel Prize in Economics in 1974 in part for his work on this theory.

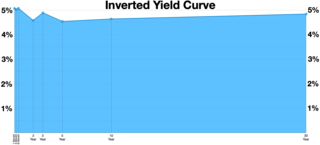

In finance, an inverted yield curve is a yield curve in which short-term debt instruments have a greater yield than longer term bonds. An inverted yield curve is an unusual phenomenon; bonds with shorter maturities generally provide lower yields than longer term bonds.

The Philadelphia Fed Report, formally known as the Business Outlook Survey and sometimes abbreviated as BOS, is a monthly survey produced by the Federal Reserve Bank of Philadelphia which questions manufacturers on general business conditions. The index covers the Third Federal Reserve District, namely covers eastern and central Pennsylvania, the nine southern counties of New Jersey, and Delaware. The report is sometimes also called the Philadelphia Fed Index because it includes reporting of some index values.

The Great Moderation is a period in the United States of America starting from the mid-1980s until at least 2007 characterized by the reduction in the volatility of business cycle fluctuations in developed nations compared with the decades before. It is believed to be caused by institutional and structural changes, particularly in central bank policies, in the second half of the twentieth century.

The Depression of 1920–1921 was a sharp deflationary recession in the United States, United Kingdom and other countries, beginning 14 months after the end of World War I. It lasted from January 1920 to July 1921. The extent of the deflation was not only large, but large relative to the accompanying decline in real product.

The Supervisory Capital Assessment Program, publicly described as the bank stress tests, was an assessment of capital conducted by the Federal Reserve System and thrift supervisors to determine if the largest U.S. financial organizations had sufficient capital buffers to withstand the recession and the financial market turmoil. The test used two macroeconomic scenarios, one based on baseline conditions and the other with more pessimistic expectations, to plot a 'What If?' exploration into the banking situation in the rest of 2009 and into 2010. The capital levels at 19 institutions were assessed based on their Tier 1 common capital, although it was originally thought that regulators would use tangible common equity as the yardstick. The results of the tests were released on May 7, 2009, at 5pm EST.

The Brookings Papers on Economic Activity (BPEA) is a journal of macroeconomics published twice a year by the Brookings Institution Press.[1] Each issue of the journal comprises the proceedings of a conference held biannually by the Economic Studies program at the Brookings Institution in Washington D.C. The conference and journal both "emphasize innovative analysis that has an empirical orientation, take real-world institutions seriously, and is relevant to economic policy."[2]

The Economic Cycle Research Institute (ECRI) based in New York City, is an independent institute formed in 1996 by Geoffrey H. Moore, Anirvan Banerji, and Lakshman Achuthan. It provides economic modeling, financial databases, economic forecasting, and market cycles services to investment managers, business executives, and government policymakers.

Real business-cycle theory is a class of new classical macroeconomics models in which business-cycle fluctuations are accounted for by real shocks. Unlike other leading theories of the business cycle, RBC theory sees business cycle fluctuations as the efficient response to exogenous changes in the real economic environment. That is, the level of national output necessarily maximizes expected utility, and governments should therefore concentrate on long-run structural policy changes and not intervene through discretionary fiscal or monetary policy designed to actively smooth out economic short-term fluctuations.

Francis X. Diebold is an American economist known for his work in predictive econometric modeling, financial econometrics, and macroeconometrics. He earned both his B.S. and Ph.D. degrees at the University of Pennsylvania, where his doctoral committee included Marc Nerlove, Lawrence Klein, and Peter Pauly. He has spent most of his career at Penn, where he has mentored approximately 75 Ph.D. students. Presently he is Paul F. and Warren S. Miller Professor of Social Sciences and Professor of Economics at Penn’s School of Arts and Sciences, and Professor of Finance and Professor of Statistics at Penn’s Wharton School. He is also a Faculty Research Associate at the National Bureau of Economic Research in Cambridge, Massachusetts, and author of the No Hesitations blog.

The 1994 bond market crisis, or Great Bond Massacre, was a sudden drop in bond market prices across the developed world. It began in Japan and the United States (US), and spread through the rest of the world. After the recession of the early 1990s, historically low interest rates in many industrialized nations preceded an unexpectedly volatile year for bond investors, including those that held on to mortgage debts. Over 1994, a rise in rates, along with the relatively quick spread of bond market volatility across international borders, resulted in a mass sell-off of bonds and debt funds as yields rose beyond expectations. This was especially the case for instruments with comparatively longer maturities attached. Some financial observers argued that the plummet in bond prices was triggered by the Federal Reserve's decision to raise rates by 25 basis points in February, in a move to counter inflation. At about $1.5 trillion in lost market value across the globe, the crash has been described as the worst financial event for bond investors since 1927.

The Aruoba-Diebold-Scotti Business Conditions Index is a coincident business cycle indicator used in macroeconomics in the United States. The index measures business activity, which may be correlated with periods of expansion and contraction in the economy. The primary and novel function of the ADS index stems from its use of high-frequency economic data and subsequent high-frequency updating, opposed to the traditionally highly-lagged and infrequently-published macroeconomic data such as GDP.