External links

| This tax-related article is a stub. You can help Wikipedia by expanding it. |

A tax-allocation district (TAD), also known as tax increment financing, is a defined area where real estate property tax monies gathered above a certain threshold for a certain period of time (typically 25 years) to be used a specified improvement. The funds raised from a TAD are placed in a tax-free bond (finance) where the money can continue to grow. These improvements are typically for revitalization and especially to complete redevelopment efforts.

Tax-increment financing has attracted much criticism as merely a subsidy to connected developers. California, where the practice began, has discontinued their use though it will be paying off debt on previous formed districts for years to come.

Enactment of a TAD typically requires approval of all local governments who will be giving-up taxes, thus a project within a municipality will also require approval of the county's commission (or its local equivalent), and the board of the school district, in addition to the city council and possibly township board of supervisors (if applicable).

This differs from an improvement district, which the property owners agree to pay extra for improvements. That is only an option for an area which is already in good economic health.

| This tax-related article is a stub. You can help Wikipedia by expanding it. |

A municipal bond, commonly known as a muni bond, is a bond issued by a local government or territory, or one of their agencies. It is generally used to finance public projects such as roads, schools, airports and seaports, and infrastructure-related repairs. The term municipal bond is commonly used in the United States, which has the largest market of such trade-able securities in the world. As of 2011, the municipal bond market was valued at $3.7 trillion. Potential issuers of municipal bonds include states, cities, counties, redevelopment agencies, special-purpose districts, school districts, public utility districts, publicly owned airports and seaports, and other governmental entities at or below the state level having more than a de minimis amount of one of the three sovereign powers: the power of taxation, the power of eminent domain or the police power.

In the United States, a homeowner association is a private association often formed by a real estate developer for the purpose of marketing, managing, and selling homes and lots in a residential subdivision. Typically the developer will transfer control of the association to the homeowners after selling a predetermined number of lots. Generally any person who wants to buy a residence within the area of a homeowners association must become a member, and therefore must obey the governing documents including Articles of Incorporation, CC&Rs and By-Laws, which may limit the owner's choices. Homeowner associations are especially active in urban planning, zoning and land use, decisions that affect the pace of growth, the quality of life, the level of taxation and the value of land in the community. Most homeowner associations are incorporated, and are subject to state statutes that govern non-profit corporations and homeowner associations. State oversight of homeowner associations is minimal, and it varies from state to state. Some states, such as Florida and California, have a large body of HOA law. Other states, such as Massachusetts, have virtually no HOA law. Homeowners associations are commonly found in residential developments since the passage of the Davis–Stirling Common Interest Development Act in 1985.

Proposition 13 is an amendment of the Constitution of California enacted during 1978, by means of the initiative process. The initiative was approved by California voters on June 6, 1978. It was upheld as constitutional by the United States Supreme Court in the case of Nordlinger v. Hahn, 505 U.S. 1 (1992). Proposition 13 is embodied in Article XIII A of the Constitution of the State of California.

The Low-Income Housing Tax Credit is a dollar-for-dollar tax credit in the United States for affordable housing investments. It was created under the Tax Reform Act of 1986 (TRA86) and gives incentives for the utilization of private equity in the development of affordable housing aimed at low-income Americans. LIHTC accounts for the majority of all affordable rental housing created in the United States today. As the maximum rent that can be charged is based upon the Area Median Income ("AMI"), LIHTC housing remains unaffordable to many low-income renters. The credits are also commonly called Section 42 credits in reference to the applicable section of the Internal Revenue Code. The tax credits are more attractive than tax deductions as the credits provide a dollar-for-dollar reduction in a taxpayer's federal income tax, whereas a tax deduction only provides a reduction in taxable income. The "passive loss rules" and similar tax changes made by TRA86 greatly reduced the value of tax credits and deductions to individual taxpayers. Less than 10% of current credit expenditures are claimed by individual investors.

Tax increment financing (TIF) is a public financing method that is used as a subsidy for redevelopment, infrastructure, and other community-improvement projects in many countries, including the United States. The original intent of a TIF program is to stimulate private investment with a blighted area that has been designated to be in need of economic revitalization. Similar or related value capture strategies are used around the world.

Massachusetts shares with the five other New England states a governmental structure known as the New England town. Only the southeastern third of the state has functioning county governments; in western, central, and northeastern Massachusetts, traditional county-level government was eliminated in the late 1990s. Generally speaking, there are four kinds of public school districts in Massachusetts: local schools, regional schools, vocational/technical schools, and charter schools.

Sales taxes in the United States are taxes placed on the sale or lease of goods and services in the United States. Sales tax is governed at the state level and no national general sales tax exists. Forty-five states, the District of Columbia, the territories of the Puerto Rico, and Guam impose general sales taxes that apply to the sale or lease of most goods and some services, and states also may levy selective sales taxes on the sale or lease of particular goods or services. States may grant local governments the authority to impose additional general or selective sales taxes.

Proposition 218 is an adopted initiative constitutional amendment which revolutionized local and regional government finance in California. Called the "Right to Vote on Taxes Act," it was sponsored by the Howard Jarvis Taxpayers Association as a constitutional follow-up to the landmark property tax reduction initiative constitutional amendment, Proposition 13, approved in 1978. Proposition 218 was approved by California voters during the November 5, 1996, statewide general election.

Community Facilities Districts (CFDs), more commonly known as Mello-Roos, are special districts established by local governments in California as a means of obtaining additional public funding. Counties, cities, special districts, joint powers authority, and schools districts in California use these financing districts to pay for public works and some public services.

The 2007 Texas Constitutional Amendment Election took place 6 November 2007.

Taxes in Indiana are almost entirely authorized at the state level, although the revenue is used to fund both local and state level government. The state of Indiana's income comes from four primary tax areas. Most state level income is from a sales tax of 7% and a flat state income tax of 3.23%. The state also collects an additional income tax for some counties. Local governments are funded by a property tax that is the sum of rates set by local boards, but the total rate must be approved by the Indiana General Assembly before it can be imposed. Residential property tax rates are capped at maximum of 1% of property value. Excise tax is the fourth form of taxation and is charged on motor vehicles, alcohol, tobacco, gasoline, and certain other forms of movable property; most of the proceeds are used to fund state and local roads and health programs. The Indiana Department of Revenue collects all taxes and pays them out to the appropriate agencies and municipalities. The Indiana Tax Court deals with all tax disputes issues, but decisions can be appealed to the Indiana Supreme Court.

The Tax Relief and Health Care Act of 2006, includes a package of tax extenders, provisions affecting health savings accounts and other provisions in the United States.

A tax increment reinvestment zone (TIRZ) is a political subdivision of a municipality or county in the state of Texas created to implement tax increment financing. They may be initiated by the city or county or by petition of owners whose total holdings in the zone consist of a majority of the appraised property value. To get funding for a TIRZ area applicants have to follow three steps.

PACE financing is a means of financing energy efficiency upgrades, disaster resiliency improvements, water conservation measures, or renewable energy installations of residential, commercial, and industrial property owners. Depending on state legislation, PACE financing can be used to finance building envelope energy efficiency improvements such as insulation and air sealing, cool roofs, water efficiency products, seismic retrofits, and hurricane preparedness measures. In some states, commercial PACE financing can also fund a portion of new construction projects, as long as the building owner agrees to build the new structure to exceed the local energy code.

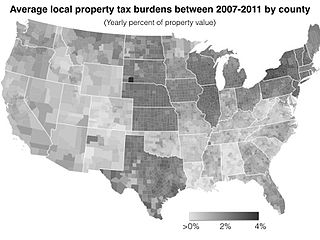

Most local governments in the United States impose a property tax, also known as a millage rate, as a principal source of revenue. This tax may be imposed on real estate or personal property. The tax is nearly always computed as the fair market value of the property times an assessment ratio times a tax rate, and is generally an obligation of the owner of the property. Values are determined by local officials, and may be disputed by property owners. For the taxing authority, one advantage of the property tax over the sales tax or income tax is that the revenue always equals the tax levy, unlike the other taxes. The property tax typically produces the required revenue for municipalities' tax levies. A disadvantage to the taxpayer is that the tax liability is fixed, while the taxpayer's income is not.

Sales and use taxes in California are among the highest in the United States and are imposed by the state and by local governments. From a tax terminology perspective, sales taxes are a proportional tax; though because of the fact that lower income earners may pay a greater percentage of their earnings to sales taxes than higher income earners, a sales tax is also described as a regressive tax.

Tourism Improvement Districts (TIDs) are a type of business improvement district in the USA. The aim of TIDs is increasing the number of overnight visitors using business and services in that area. TIDs are formed through a public-private partnership between the local government and the businesses in a district. TID funds are usually managed by a nonprofit corporation, generally a Convention and Visitors' Bureau, hotel association, or similar destination marketing organization. Typical TID services include marketing programs to raise awareness of the destination, sponsorship of special events that attract overnight visitors, and sales programs to bring in large-group business. Synonymous terms for TIDs include: tourism marketing district, hotel improvement district, and tourism business improvement district.

A parcel tax is a form of real estate tax that, unlike most real estate taxes or a land value tax, is not directly based on property value. The parcel tax is used in California to fund K–12 public education and to fund community facilities districts usually known as "Mello-Roos" districts. The parcel tax in its typical form as a flat tax is regressive: While most parcel taxes are a fixed amount per parcel, some are based on the size of the parcel or its improvements.

Business improvement districts (BIDs), also known as local improvement districts (LIDs), are special districts within a city that are overseen by a nonprofit entity. In the United States, BIDs are typically funded by an additional tax assessment, with the tax increase going toward improvements of the area. BIDs have been used in nearly 1,000 major cities and small towns throughout the United States, including most major U.S. cities that have multiple BIDs. New York City alone has 76 BIDs.

A transportation improvement district or transportation development district (TDD) is a special-purpose district created in some U.S. states for the purpose of coordinating and financing transportation infrastructure improvement programs, particularly road construction projects, among local governments in a specific area. Depending on the state, they may have the authority to levy sales or property taxes or issue municipal bonds. TIDs or TDDs are authorized in Missouri, New Jersey, Ohio, and Virginia.