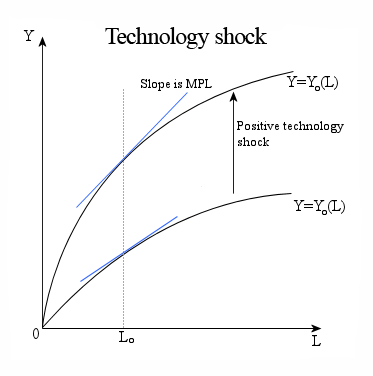

An example of the function, where Y=output, L=labor, MPL=marginal product of labor. The technology shock increases the output given the same level of, in this case, labor. The marginal product of labor is higher after the positive technology shock, this can be seen in the MPL (blue) line being steeper.

Technology shocks are sudden changes in technology that significantly affect economic, social, political or other outcomes.[1] In economics, the term technology shock usually refers to events in a macroeconomic model, that change the production function. Usually this is modeled with an aggregate production function that has a scaling factor.

Normally reference is made to positive (i.e., productivity enhancing) technological changes, though technology shocks can also be contractionary.[2] The term “shock” connotes the fact that technological progress is not always gradual – there can be large-scale discontinuous changes that significantly alter production methods and outputs in an industry, or in the economy as a whole. Such a technology shock can occur in many different ways.[3] For example, it may be the result of advances in science that enable new trajectories of innovation, or may result when an existing technological alternative improves to a point that it overtakes the dominant design, or is transplanted to a new domain. It can also occur as the result of a shock in another system, such as when a change in input prices dramatically changes the price/performance relationship for a technology,[4] or when a change in the regulatory environment significantly alters the technologies permitted (or demanded) in the market. Numerous studies have shown that technology shocks can have a significant effect on investment, economic growth, labor productivity, collaboration patterns, and innovation.[5]

Positive technology shock

The Industrial Revolution is an example of a positive technology shock. The Industrial Revolution occurred between the 18th and the 19th centuries where major changes in agriculture, manufacturing, mining, transport, and technology occurred.[6]

What this did to the economy at the time was notable. It increased wages steadily over the period of time and it also increased population because people had the wages for standard living. This is an example of a positive technology shock, where it increases national and disposable income, and also increases the labor force. The Industrial Revolution also provided a much more efficient way to produce goods which lead to less labor-intensive work.[6]

The rise of the internet, which coincided with rapid innovation in related networking equipment and software, also caused a major shock to the economy.[7][8] The internet was a “general-purpose technology” with the potential to transform information dissemination on a massive scale. The shock created both great opportunity and great uncertainty for firms, precipitating large increases in alliance activity and an increase in innovation across a wide range of sectors.[7]

Negative technology shock

The oil shocks that occurred in the late 1970s are examples of negative technology shocks. When the oil shocks occurred, the energy that was used to extract to oil became more expensive, the energy was the technology in this case.[clarification needed] The price of the capital and the labor both went up due to this shock,[9] and this is an example of a negative technology shock.

More examples

There are many examples of different types of technology shocks, but one of the biggest in the past couple of decades has been Web 2.0. Web 2.0 was a huge technological advancement in the e commerce business, it allowed for user interaction benefiting businesses in different ways.[10] It allowed for user feedback, ratings, comments, user content, etc. Web 2.0 revolutionized the online business as a whole, an example of a positive technology shock.

Real business cycle theory

Real business cycle theory (RBCT) is the theory where any type of shock has a ripple effect into many other shocks. To relate this to current times the upward price on oil is a RBCT because of the negative technology shock that happened due to the raise in price for the process of extracting of the oil. Now due to this increase in price for energy to extract the oil, fewer people could afford oil which drove economic activity down and at the same time lessens a countries national GDP. Typically, a RBCT starts with a negative type of shock, which is why the RBCT is becoming less and less relevant in today's economics. More and more economists are arguing against the RBCT because very rarely can you have a negative shock on technology with the amount of advancements we are going through now.[11]

↑ Schilling, M. A. (2015). "Technology Shocks, Technological Collaboration, and Innovation Outcomes". Organization Science. 26 (3): 668–686. doi:10.1287/orsc.2015.0970.

↑ Basu, S., Fernald, J.G., Kimball, M.S. (2006) "Are technology improvements contractionary?" American Economic Review 96:1418-1448.

↑ Schilling, M. A. (2015). "Technology Shocks, Technological Collaboration, and Innovation Outcomes". Organization Science 26 (3): 668–686. doi:10.1287/orsc.2015.0970.

↑ Ehrnberg, E. (1995) "On the definition and measurement of technological discontinuities." Technovation Volume 15, Issue 7, September 1995, pp. 437-452.

↑ Alexopoulos, M. (2011) "What Happens Following a Technology Shock?" American Economic Review, 101 (4): 1144-79. DOI: 10.1257/aer.101.4.1144; Christiano, L.J. Eichenbaum, M. and Vigfusson, R.J. (2003) What Happens after a Technology Shock? NBER Working Paper No. w9819. Available at SSRN: https://ssrn.com/abstract=421780; Galí, J. (1999) "Technology, Employment, and the Business Cycle: Do Technology Shocks Explain Aggregate Fluctuations?" American Economic Review 89 (1): 249-271; Schilling, M. A. (2015). "Technology Shocks, Technological Collaboration, and Innovation Outcomes". Organization Science 26 (3): 668–686. doi:10.1287/orsc.2015.0970.

1 2 Landes, David S. (1969). The Unbound Prometheus: Technological Change and Industrial Development in Western Europe from 1750 to the Present. Cambridge, New York: Press Syndicate of the University of Cambridge. ISBN0-521-09418-6.

1 2 Schilling, M. A. (2015). "Technology Shocks, Technological Collaboration, and Innovation Outcomes". Organization Science. 26 (3): 668–686. doi:10.1287/orsc.2015.0970. S2CID207244744.

Macroeconomics is a branch of economics that deals with the performance, structure, behavior, and decision-making of an economy as a whole. This includes national, regional, and global economies. Macroeconomists study topics such as output/GDP and national income, unemployment, price indices and inflation, consumption, saving, investment, energy, international trade, and international finance.

In economics, inflation is a general increase in the prices of goods and services in an economy. This is usually measured using the consumer price index (CPI). When the general price level rises, each unit of currency buys fewer goods and services; consequently, inflation corresponds to a reduction in the purchasing power of money. The opposite of CPI inflation is deflation, a decrease in the general price level of goods and services. The common measure of inflation is the inflation rate, the annualized percentage change in a general price index. As prices faced by households do not all increase at the same rate, the consumer price index (CPI) is often used for this purpose.

Organizational learning is the process of creating, retaining, and transferring knowledge within an organization. An organization improves over time as it gains experience. From this experience, it is able to create knowledge. This knowledge is broad, covering any topic that could better an organization. Examples may include ways to increase production efficiency or to develop beneficial investor relations. Knowledge is created at four different units: individual, group, organizational, and inter organizational.

One of the major subfields of urban economics, economies of agglomeration, explains, in broad terms, how urban agglomeration occurs in locations where cost savings can naturally arise. This term is most often discussed in terms of economic firm productivity. However, agglomeration effects also explain some social phenomena, such as large proportions of the population being clustered in cities and major urban centers. Similar to economies of scale, the costs and benefits of agglomerating increase the larger the agglomerated urban cluster becomes. Several prominent examples of where agglomeration has brought together firms of a specific industry are: Silicon Valley and Los Angeles being hubs of technology and entertainment, respectively, in California, United States; and London, United Kingdom, being a hub of finance.

In economics, a shock is an unexpected or unpredictable event that affects an economy, either positively or negatively. Technically, it is an unpredictable change in exogenous factors—that is, factors unexplained by an economic model—which may influence endogenous economic variables.

Induced innovation is a microeconomic hypothesis first proposed in 1932 by John Hicks in his work The Theory of Wages. He proposed that "a change in the relative prices of the factors of production is itself a spur to invention, and to invention of a particular kind—directed to economizing the use of a factor which has become relatively expensive."

A supply shock is an event that suddenly increases or decreases the supply of a commodity or service, or of commodities and services in general. This sudden change affects the equilibrium price of the good or service or the economy's general price level.

Deindustrialization is a process of social and economic change caused by the removal or reduction of industrial capacity or activity in a country or region, especially of heavy industry or manufacturing industry.

The Gerschenkron effect, developed by Alexander Gerschenkron, claims that changing the base year for an index determines the growth rate of the index. This effect is applicable only to aggregation method using reference price structure or reference volume structure. However, if production is measured by "real" tearms, this effect does not exist.

In economics, deskilling is the process by which skilled labor within an industry or economy is eliminated by the introduction of technologies operated by semi- or unskilled workers. This results in cost savings due to lower investment in human capital, and reduces barriers to entry, weakening the bargaining power of the human capital. Deskilling is the decline in working positions through the machinery or technology introduced to separate workers from the production process.

Hydrocarbon economy is a term referencing the global hydrocarbon industry and its relationship to world markets. Energy used mostly comes from three hydrocarbons: petroleum, coal, and natural gas. Hydrocarbon economy is often used when talking about possible alternatives like the hydrogen economy.

In economics, a spillover is a positive or a negative, but more often negative, impact experienced in one region or across the world due to an independent event occurring from an unrelated environment.

In economics, a demand shock is a sudden event that increases or decreases demand for goods or services temporarily.

Innovation management is a combination of the management of innovation processes, and change management. It refers to product, business process, marketing and organizational innovation. Innovation management is the subject of ISO 56000 series standards being developed by ISO TC 279.

Real business-cycle theory is a class of new classical macroeconomics models in which business-cycle fluctuations are accounted for by real shocks. Unlike other leading theories of the business cycle, RBC theory sees business cycle fluctuations as the efficient response to exogenous changes in the real economic environment. That is, the level of national output necessarily maximizes expected utility, and governments should therefore concentrate on long-run structural policy changes and not intervene through discretionary fiscal or monetary policy designed to actively smooth out economic short-term fluctuations.

Technological unemployment is the loss of jobs caused by technological change. It is a key type of structural unemployment. Technological change typically includes the introduction of labour-saving "mechanical-muscle" machines or more efficient "mechanical-mind" processes (automation), and humans' role in these processes are minimized. Just as horses were gradually made obsolete as transport by the automobile and as labourer by the tractor, humans' jobs have also been affected throughout modern history. Historical examples include artisan weavers reduced to poverty after the introduction of mechanized looms. During World War II, Alan Turing's bombe machine compressed and decoded thousands of man-years worth of encrypted data in a matter of hours. A contemporary example of technological unemployment is the displacement of retail cashiers by self-service tills and cashierless stores.

Open collaboration refers to any "system of innovation or production that relies on goal-oriented yet loosely coordinated participants who cooperate voluntarily to create a product of economic value, which is made freely available to contributors and noncontributors alike." It is prominently observed in open source software, and has been initially described in Richard Stallman's GNU Manifesto, as well as Eric S. Raymond's 1997 essay, The Cathedral and the Bazaar. Beyond open source software, open collaboration is also applied to the development of other types of mind or creative works, such as information provision in Internet forums, or the production of encyclopedic content in Wikipedia.

The economics of digitization is the field of economics that studies how digitization, digitalisation and digital transformation affects markets and how digital data can be used to study economics. Digitization is the process by which technology lowers the costs of storing, sharing, and analyzing data. This has changed how consumers behave, how industrial activity is organized, and how governments operate. The economics of digitization exists as a distinct field of economics for two reasons. First, new economic models are needed because many traditional assumptions about information no longer hold in a digitized world. Second, the new types of data generated by digitization require new methods for their analysis.

Green industrial policy (GIP) is strategic government policy that attempts to accelerate the development and growth of green industries to transition towards a low-carbon economy. Green industrial policy is necessary because green industries such as renewable energy and low-carbon public transportation infrastructure face high costs and many risks in terms of the market economy. Therefore, they need support from the public sector in the form of industrial policy until they become commercially viable. Natural scientists warn that immediate action must occur to lower greenhouse gas emissions and mitigate the effects of climate change. Social scientists argue that the mitigation of climate change requires state intervention and governance reform. Thus, governments use GIP to address the economic, political, and environmental issues of climate change. GIP is conducive to sustainable economic, institutional, and technological transformation. It goes beyond the free market economic structure to address market failures and commitment problems that hinder sustainable investment. Effective GIP builds political support for carbon regulation, which is necessary to transition towards a low-carbon economy. Several governments use different types of GIP that lead to various outcomes. The Green Industry plays a pivotal role in creating a sustainable and environmentally responsible future; By prioritizing resource efficiency, renewable energy, and eco-friendly practices, this industry significantly benefits society and the planet at large.

Melissa A. Schilling is an American innovation scholar and professor. She holds the John Herzog Family chair in management and organizations at NYU Stern, and she is also the Innovation Director for Stern's Fubon Center for Technology, Business and Innovation. She is world known as an expert in innovation, is the author of the leading innovation strategy text, Strategic Management of Technological Innovation, and is a coauthor of Strategic Management: Theory and Cases. She is also the author of Quirky: The remarkable story of the traits, foibles, and genius of breakthrough innovators who changed the world. She and her work have been featured in NPR's Marketplace, The Wall Street Journal, Bloomberg BusinessWeek, Entrepreneur, Inc., Financial Times, Harvard Business Review, Huffington Post, CNBC, Scientific American, and USA Today, among others. She also speaks regularly at national and international conferences as well as at corporations on strategy and innovation.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.