Related Research Articles

In finance, a derivative is a contract that derives its value from the performance of an underlying entity. This underlying entity can be an asset, index, or interest rate, and is often simply called the "underlying". Derivatives can be used for a number of purposes, including insuring against price movements (hedging), increasing exposure to price movements for speculation, or getting access to otherwise hard-to-trade assets or markets. Some of the more common derivatives include forwards, futures, options, swaps, and variations of these such as synthetic collateralized debt obligations and credit default swaps. Most derivatives are traded over-the-counter (off-exchange) or on an exchange such as the Chicago Mercantile Exchange, while most insurance contracts have developed into a separate industry. In the United States, after the financial crisis of 2007–2009, there has been increased pressure to move derivatives to trade on exchanges.

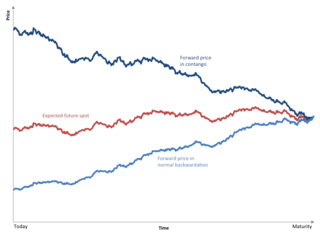

Contango is a situation where the futures price of a commodity is higher than the expected spot price of the contract at maturity. In a contango situation, arbitrageurs or speculators are "willing to pay more [now] for a commodity [to be received] at some point in the future than the actual expected price of the commodity [at that future point]. This may be due to people's desire to pay a premium to have the commodity in the future rather than paying the costs of storage and carry costs of buying the commodity today." On the other side of the trade, hedgers are happy to sell futures contracts and accept the higher-than-expected returns. A contango market is also known as a normal market, or carrying-cost market.

In finance, being short in an asset means investing in such a way that the investor will profit if the value of the asset falls. This is the opposite of a more conventional "long" position, where the investor will profit if the value of the asset rises.

An economic bubble is a situation in which asset prices are much higher than the underlying fundamentals can reasonably justify. Bubbles are sometimes caused by unlikely and overly optimistic projections about the future. It could also be described as prices which strongly exceed the asset's intrinsic value.

In finance, the capital asset pricing model (CAPM) is a model used to determine a theoretically appropriate required rate of return of an asset, to make decisions about adding assets to a well-diversified portfolio.

In finance, a put or put option is a financial market derivative instrument that gives the holder the right to sell an asset, at a specified price, by a specified date to the writer of the put. The purchase of a put option is interpreted as a negative sentiment about the future value of the underlying stock. The term "put" comes from the fact that the owner has the right to "put up for sale" the stock or index.

A credit default swap (CDS) is a financial swap agreement that the seller of the CDS will compensate the buyer in the event of a debt default or other credit event. That is, the seller of the CDS insures the buyer against some reference asset defaulting. The buyer of the CDS makes a series of payments to the seller and, in exchange, may expect to receive a payoff if the asset defaults.

In finance, valuation is the process of determining the present value (PV) of an asset. Valuations can be done on assets or on liabilities. Valuations are needed for many reasons such as investment analysis, capital budgeting, merger and acquisition transactions, financial reporting, taxable events to determine the proper tax liability.

In finance, a swap is an agreement between two counterparties to exchange financial instruments or cashflows or payments for a certain time. The instruments can be almost anything but most swaps involve cash based on a notional principal amount.

Rational pricing is the assumption in financial economics that asset prices - and hence asset pricing models - will reflect the arbitrage-free price of the asset as any deviation from this price will be "arbitraged away". This assumption is useful in pricing fixed income securities, particularly bonds, and is fundamental to the pricing of derivative instruments.

A collateralized debt obligation (CDO) is a type of structured asset-backed security (ABS). Originally developed as instruments for the corporate debt markets, after 2002 CDOs became vehicles for refinancing mortgage-backed securities (MBS). Like other private label securities backed by assets, a CDO can be thought of as a promise to pay investors in a prescribed sequence, based on the cash flow the CDO collects from the pool of bonds or other assets it owns. Distinctively, CDO credit risk is typically assessed based on a probability of default (PD) derived from ratings on those bonds or assets.

Business valuation is a process and a set of procedures used to estimate the economic value of an owner's interest in a business. Here various valuation techniques are used by financial market participants to determine the price they are willing to pay or receive to effect a sale of the business. In addition to estimating the selling price of a business, the same valuation tools are often used by business appraisers to resolve disputes related to estate and gift taxation, divorce litigation, allocate business purchase price among business assets, establish a formula for estimating the value of partners' ownership interest for buy-sell agreements, and many other business and legal purposes such as in shareholders deadlock, divorce litigation and estate contest.

Financial risk is any of various types of risk associated with financing, including financial transactions that include company loans in risk of default. Often it is understood to include only downside risk, meaning the potential for financial loss and uncertainty about its extent.

In finance, a price (premium) is paid or received for purchasing or selling options. This article discusses the calculation of this premium in general. For further detail, see: Mathematical finance § Derivatives pricing: the Q world for discussion of the mathematics; Financial engineering for the implementation; as well as Financial modeling § Quantitative finance generally.

In finance, a collar is an option strategy that limits the range of possible positive or negative returns on an underlying to a specific range. A collar strategy is used as one of the ways to hedge against possible losses and it represents long put options financed with short call options.

The following outline is provided as an overview of and topical guide to finance:

In finance, an option is a contract which conveys to its owner, the holder, the right, but not the obligation, to buy or sell an underlying asset or instrument at a specified strike price on or before a specified date, depending on the style of the option. Options are typically acquired by purchase, as a form of compensation, or as part of a complex financial transaction. Thus, they are also a form of asset and have a valuation that may depend on a complex relationship between underlying asset value, time until expiration, market volatility, and other factors. Options may be traded between private parties in over-the-counter (OTC) transactions, or they may be exchange-traded in live, orderly markets in the form of standardized contracts.

A synthetic CDO is a variation of a CDO that generally uses credit default swaps and other derivatives to obtain its investment goals. As such, it is a complex derivative financial security sometimes described as a bet on the performance of other mortgage products, rather than a real mortgage security. The value and payment stream of a synthetic CDO is derived not from cash assets, like mortgages or credit card payments – as in the case of a regular or "cash" CDO—but from premiums paying for credit default swap "insurance" on the possibility of default of some defined set of "reference" securities—based on cash assets. The insurance-buying "counterparties" may own the "reference" securities and be managing the risk of their default, or may be speculators who've calculated that the securities will default.

A toxic asset is a financial asset that has fallen in value significantly and for which there is no longer a functioning market. Such assets cannot be sold at a price satisfactory to the holder. Because assets are offset against liabilities and frequently leveraged, this decline in price may be quite dangerous to the holder. The term became common during the financial crisis of 2007–2008, in which they played a major role.

Factor investing is an investment approach that involves targeting quantifiable firm characteristics or “factors” that can explain differences in stock returns. Security characteristics that may be included in a factor-based approach include size, low-volatility, value, momentum, asset growth, profitability, leverage, term and carry.

References

- ↑ Carr, Wu (2009). "Variance Risk Premiums". The Review of Financial Studies. Retrieved 2014-03-30.

| | This economics-related article is a stub. You can help Wikipedia by expanding it. |